The impact of inflation on real interest rates significantly erodes the true value of your savings returns, a critical concept every investor must grasp. Understanding this dynamic is not merely academic; it directly influences your purchasing power and long-term financial health. When prices rise, the money you hold or save loses some of its ability to buy goods and services. Therefore, discerning the difference between nominal and real returns becomes paramount for effective wealth preservation and growth.

For many, inflation feels like a nebulous economic force. However, its effects are tangible, especially on fixed-income investments and cash held in traditional savings accounts. Investors frequently overlook how seemingly positive nominal returns can, in reality, represent a loss of wealth after accounting for the increase in living costs. Consequently, a deep dive into this topic provides crucial insights for making informed financial decisions.

Understanding Inflation: A Silent Erosion of Purchasing Power

Inflation, in essence, describes the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. This economic phenomenon impacts everyone, from individual consumers to multinational corporations. Notably, moderate inflation is often considered a sign of a healthy, growing economy. However, uncontrolled or high inflation can wreak havoc on financial stability.

What is Inflation?

Fundamentally, inflation means your money buys less today than it did yesterday. Consider a simple example: if a loaf of bread costs $2 this year and $2.10 next year, that represents a 5% inflation rate for bread. This trend, when widespread across an economy, reflects a decline in the value of each unit of currency. Therefore, people need more money to acquire the same amount of goods and services over time. This erosion is particularly insidious because it often occurs gradually, making its long-term effects easy to underestimate.

Measuring Inflation: The CPI

Economists primarily measure inflation using price indexes. The most commonly cited measure in many countries, including the United States, is the Consumer Price Index (CPI). The Bureau of Labor Statistics (BLS) calculates the CPI by taking a basket of consumer goods and services, such as food, housing, transportation, and medical care. They then track the average change in prices paid by urban consumers for this basket over time. Consequently, if the CPI rises by 3%, it indicates that, on average, consumer prices have increased by 3% over a specified period. This metric provides a crucial benchmark for assessing the true cost of living and the effectiveness of economic policies.

Furthermore, other measures like the Producer Price Index (PPI) track price changes at the wholesale level. The Personal Consumption Expenditures (PCE) price index, preferred by the Federal Reserve, offers another perspective, focusing on what consumers actually spend. Each of these indexes offers valuable insights into different facets of inflationary pressures across the economy.

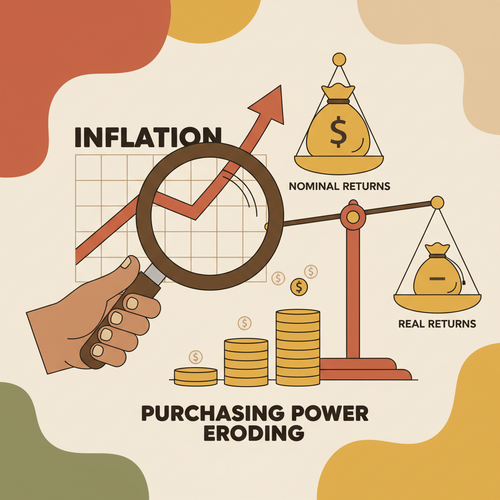

Nominal vs. Real Interest Rates: The Crucial Distinction

To truly understand how inflation affects your money, distinguishing between nominal and real interest rates is absolutely essential. Many investors only focus on the headline number they see advertised by banks, which represents the nominal rate. However, the real rate tells the actual story of your investment’s growth.

Defining Nominal Interest Rates

A nominal interest rate is the stated interest rate on a loan or investment without taking inflation into account. For instance, if your savings account advertises a 2% annual interest rate, that 2% is the nominal rate. This is the rate banks quote for loans, mortgages, and savings accounts. It represents the absolute monetary increase you receive on your principal. However, this figure alone does not reflect the actual purchasing power gain or loss, particularly in an inflationary environment. Understanding this fundamental concept is the first step towards savvy financial planning.

The True Story: Real Interest Rates

The real interest rate, by contrast, is the nominal interest rate minus the rate of inflation. This figure reveals the true return on your investment or the true cost of borrowing after accounting for changes in purchasing power. For example, if your savings account offers a 2% nominal interest rate, but inflation is running at 3%, your real interest rate is -1%. This means your money is actually losing purchasing power, even though your account balance is numerically increasing. Consequently, the real interest rate provides a much more accurate picture of your financial well-being over time.

The Fisher Equation: Connecting the Dots

Economist Irving Fisher formalized the relationship between nominal interest rates, real interest rates, and inflation through what is known as the Fisher Equation. The equation states: Nominal Interest Rate ≈ Real Interest Rate + Inflation Rate. More precisely, for higher rates, the formula is: (1 + Nominal Rate) = (1 + Real Rate) * (1 + Inflation Rate). However, for practical purposes with low to moderate rates, the approximation works well.

Therefore, to calculate the real interest rate, you can rearrange the approximate equation: Real Interest Rate ≈ Nominal Interest Rate – Inflation Rate. This simple yet powerful formula highlights why a high nominal rate can still lead to a negative real return if inflation outpaces it. Savvy investors always consider this equation when evaluating potential returns. Moreover, central banks often monitor real interest rates closely when setting monetary policy, understanding their profound impact on economic activity.

How Inflation Erodes Your Savings Returns

The insidious nature of inflation becomes most apparent when examining its direct impact on your hard-earned savings. Many traditional savings vehicles are particularly vulnerable, causing a gradual, often unnoticed, depletion of wealth. Therefore, recognizing these vulnerabilities is key to protecting your financial future.

The Diminishing Value of Cash and Low-Yield Accounts

Holding significant amounts of cash in a traditional savings account or even under your mattress during periods of inflation is financially detrimental. Banks typically offer very low nominal interest rates on these accounts, often barely above zero. When inflation is higher than this nominal rate, your money steadily loses purchasing power. For instance, if inflation is 4% and your savings account yields 0.5%, your real return is -3.5%. This means for every $100 you have, its buying power effectively shrinks to $96.50 over the year. Consequently, you are effectively paying a fee to keep your money in such accounts, eroding your wealth silently.

This effect is particularly pronounced over longer periods. What seems like a small annual loss can accumulate into a significant reduction in wealth over a decade or two. Astute investors understand that idle cash, especially in inflationary environments, is not truly idle; it is actively depreciating in value. Therefore, exploring alternative options for your emergency fund or short-term savings becomes a strategic necessity.

Fixed-Income Investments Under Pressure

Fixed-income investments, such as bonds and certificates of deposit (CDs), offer a predetermined stream of payments or a fixed interest rate. While these can provide stability, they are highly susceptible to the negative effects of inflation, especially if held until maturity. When you invest in a bond with a 3% coupon rate and inflation subsequently rises to 5%, the real return on your bond becomes -2%. This means the income generated by your bond, though fixed in nominal terms, can buy less and less over time.

Furthermore, new bonds issued after an inflation surge will likely offer higher nominal yields to compensate investors for the increased cost of living. This drives down the market value of your existing, lower-yielding bonds if you need to sell them before maturity. Investopedia provides comprehensive details on the intricacies of fixed-income investing. Consequently, actively managing your fixed-income portfolio and considering inflation-protected alternatives becomes crucial during inflationary periods.

The Illusion of High Nominal Returns

Sometimes, investments may show seemingly impressive nominal returns. However, without considering inflation, these figures can be highly misleading. Imagine an investment that returns 10% in a year, which on the surface looks fantastic. If, however, the inflation rate for that same year was 8%, your real return is only 2%. While still positive, it is significantly less impactful than the nominal figure suggests. This highlights the importance of always calculating real returns to assess the actual growth of your purchasing power.

Investors who chase high nominal returns without factoring in inflation risk making poor long-term decisions. They might believe they are growing their wealth substantially, only to find that their increased monetary holdings buy them relatively the same, or even less, in real terms. Therefore, focusing on real returns is a hallmark of sophisticated investment strategies, ensuring that your wealth truly appreciates beyond mere numerical increases.

Strategies to Safeguard Your Savings Against Inflation

Given inflation’s persistent threat, proactive strategies are essential for protecting and growing your wealth. Astute investors employ various tactics to mitigate the erosion of purchasing power, ensuring their money works harder for them. Consequently, understanding these approaches empowers you to build a resilient financial portfolio.

Inflation-Indexed Securities (TIPS)

One of the most direct ways to protect against inflation is by investing in inflation-indexed securities. In the United States, Treasury Inflation-Protected Securities (TIPS) are a prime example. These government bonds adjust their principal value in response to changes in the Consumer Price Index (CPI). When inflation rises, the principal value of your TIPS increases, and vice versa. The interest payments you receive are then paid on this adjusted principal, providing a real return regardless of inflation. Therefore, TIPS offer a strong hedge against unexpected surges in inflation, making them a cornerstone for inflation-aware portfolios.

Furthermore, upon maturity, you receive either the original or the adjusted principal, whichever is greater. This feature adds another layer of protection. For investors seeking certainty in their real returns, TIPS often represent a highly appealing option. Consult the TreasuryDirect website for official information on how to purchase and manage TIPS.

Equities: A Historical Hedge

Historically, equities (stocks) have served as a powerful hedge against inflation over the long term. Companies often have the ability to pass on increased costs to consumers through higher prices for their goods and services. This can translate into increased revenues and earnings, which in turn can support higher stock prices. Furthermore, many companies own real assets, like property and equipment, whose values tend to appreciate with inflation. Consequently, investing in a diversified portfolio of stocks or equity-based mutual funds and ETFs can offer a robust defense against inflation’s corrosive effects.

However, it is important to note that equities can be volatile in the short term, and their performance is not guaranteed. Choosing companies with strong pricing power and stable business models can enhance their effectiveness as an inflation hedge. Therefore, a long-term perspective and diversification across different sectors are crucial when relying on equities.

Real Estate and Commodities

Real estate is another asset class often considered an inflation hedge. Property values and rental income tend to rise with inflation over time. As construction costs and demand for housing increase, so too does the value of existing properties. Furthermore, rental income can often be adjusted to reflect higher living costs, providing a growing stream of income. Thus, direct real estate ownership or investments in Real Estate Investment Trusts (REITs) can offer a tangible asset-based protection against inflation.

Commodities, such as gold, oil, and agricultural products, also frequently perform well during inflationary periods. Since these are the raw materials that fuel economic activity, their prices naturally rise when the cost of production and demand increase. Gold, in particular, has long been viewed as a safe-haven asset and a store of value during times of economic uncertainty and rising inflation. Consequently, strategic allocations to commodities can provide additional diversification and a direct link to rising global prices.

Diversification as a Shield

Ultimately, the most effective strategy to safeguard your savings against inflation involves a well-diversified investment portfolio. Spreading your investments across various asset classes—including stocks, bonds, real estate, and commodities—can help mitigate risks and capture opportunities regardless of the economic climate. No single asset class is immune to inflation, nor does any one perform optimally in every scenario. Therefore, a diversified approach smooths out returns and provides multiple layers of protection. This holistic strategy acknowledges that different assets react differently to inflationary pressures, ensuring that your overall portfolio maintains its purchasing power.

Moreover, diversification extends beyond asset classes to include geographical diversification and investing across different industries. This comprehensive approach ensures that your portfolio is robust enough to withstand localized economic downturns or sector-specific inflationary impacts. Prudent investors always prioritize a broad and balanced portfolio to navigate economic uncertainties effectively.

The Central Bank’s Role and Monetary Policy

Central banks, like the Federal Reserve in the United States or the European Central Bank, play a pivotal role in managing inflation and, by extension, influencing real interest rates. Their monetary policy decisions directly impact the cost of borrowing and the returns on savings, therefore making them crucial actors in the financial landscape.

Interest Rate Adjustments and Inflation Control

Central banks primarily combat inflation by adjusting benchmark interest rates, such as the federal funds rate in the US. When inflation is high, they typically raise interest rates. Higher interest rates make borrowing more expensive for businesses and consumers, which in turn dampens demand and slows economic activity. This reduction in demand helps to cool down price increases, thereby bringing inflation back under control. Consequently, a rise in nominal interest rates by the central bank aims to increase real interest rates, encouraging savings and discouraging excessive spending.

Conversely, during periods of low inflation or economic slowdowns, central banks may lower interest rates to stimulate borrowing and spending. This action aims to boost economic growth. However, if these rates fall below the inflation rate, real interest rates become negative, potentially discouraging savings and making investments in interest-bearing accounts less attractive. Therefore, the central bank’s ongoing balancing act is critical for maintaining economic stability and protecting purchasing power.

Navigating Economic Cycles

The impact of inflation on real interest rates and savings is deeply intertwined with broader economic cycles. Central banks constantly monitor a vast array of economic indicators—including employment data, GDP growth, and consumer spending—to inform their policy decisions. Their goal is to achieve a delicate balance: fostering economic growth while keeping inflation at a stable and manageable level, often around 2%. The Federal Reserve regularly publishes updates on its monetary policy decisions and economic outlook. Hence, understanding the central bank’s stance offers valuable insights into the potential future direction of interest rates and inflation.

Investors must remain attuned to these macroeconomic signals and the pronouncements from central bank officials. Such awareness allows for timely adjustments to investment strategies, helping to mitigate the negative impacts of inflation and capitalize on opportunities presented by changing interest rate environments. Ultimately, a proactive approach based on a clear understanding of monetary policy is indispensable for long-term financial success.

Conclusion

The impact of inflation on real interest rates and your savings returns is a fundamental concept that can no longer be ignored by any serious investor. Nominal returns alone paint an incomplete and often misleading picture; understanding real returns is paramount for preserving and growing your purchasing power. Inflation acts as a silent tax, steadily eroding the value of cash and fixed-income investments, making proactive financial planning essential. Therefore, an informed approach is the most potent defense against this pervasive economic force.

By comprehending the Fisher Equation, recognizing the vulnerabilities of traditional savings, and strategically allocating assets, you can build a more resilient portfolio. Employing strategies such as investing in inflation-indexed securities, diversified equities, real estate, and commodities can significantly mitigate inflation’s corrosive effects. Ultimately, staying informed about monetary policy and economic cycles empowers you to make intelligent decisions. Take control of your financial future by prioritizing real returns over nominal illusions, ensuring your wealth continues to work hard for you, even in an inflationary environment.