Introduction

Juggling multiple debt payments can feel like a stressful, unpaid part-time job. You have a credit card bill due on the 5th and a personal loan payment on the 15th. Another store card payment is due on the 23rd. The mental energy spent just keeping track of it all is exhausting. This constant financial juggling act can lead to significant stress and a feeling of being perpetually behind. Furthermore, the high interest rates on credit card debt can be especially frustrating. They can make you feel like you’re on a treadmill, running hard with your payments but barely making a dent in what you actually owe.

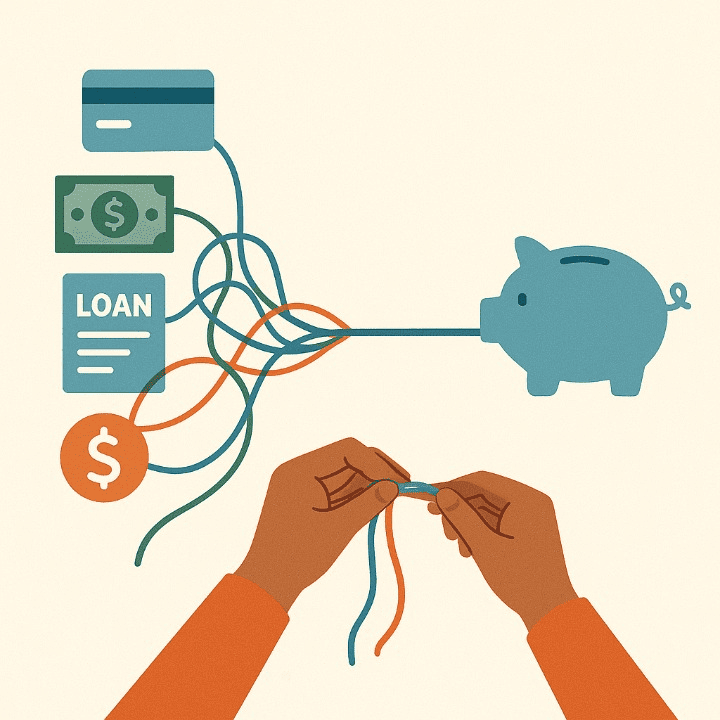

In this situation, many people explore a strategy called debt consolidation. It is a popular financial tool. It is designed to simplify this chaos into a single monthly payment. This new payment often has a lower interest rate, which is a key advantage. But is it the right move for your unique circumstances? This guide will provide an unbiased and detailed look at how debt consolidation works, its different forms, its pros and cons, and help you understand if this strategy is the right tool for your financial situation.

What is Debt Consolidation, and How Does It Work?

At its core, debt consolidation is a straightforward process. You take out a single, new form of financing. Then, you use that money to pay off multiple existing debts. Instead of managing several different payments, you are left with just one monthly payment to a single lender.

The two primary goals of debt consolidation are:

- Simplicity: This strategy streamlines your finances from many monthly payments into one. This greatly reduces the mental load. It also makes it easier to manage your budget and avoid the risk of accidentally missing payments.

- Savings: The most crucial goal is to secure a new, lower average interest rate on your total debt. By reducing your interest rate, more of your payment goes toward the principal you owe. This saves you a significant amount of money and helps you get out of debt faster.

It’s important to remember that consolidation does not eliminate your debt. It is a tool that reorganizes your debt, hopefully into a much more manageable structure.

The Key Requirement: Your Credit Score

To achieve the main goal of saving money, you need to qualify for a new loan that has a lower interest rate than your current debts. Your ability to do this depends heavily on your credit score. A higher credit score signals to lenders that you are a reliable borrower, which means they are more likely to offer you a lower interest rate. If your credit score is low, you may not be approved, or the interest rate you are offered might be too high to provide any real savings. Therefore, knowing your credit score is the first step before exploring consolidation options.

Common Methods for Debt Consolidation

There are several financial products that people commonly use to consolidate their debts. Each has its own features and risks.

Personal Loan

This is one of the most common and straightforward methods. You apply for an unsecured personal loan from a bank, credit union, or online lender. If approved, you use the lump sum of cash to pay off your high-interest debts. You are then left with a single loan to repay, typically with a fixed interest rate and a set repayment term (e.g., three to five years). This provides a clear, predictable path out of debt.

Balance Transfer Credit Card

These cards can be a powerful tool, often attracting customers with a 0% introductory interest rate for a period like 12 to 18 months. You can transfer balances from your high-interest credit cards to this new card. During this promotional period, your entire payment goes toward the principal balance, as no new interest charges are accruing. However, you must be disciplined. It is crucial to pay off the entire balance before the high standard interest rate kicks in. Also, be aware of balance transfer fees, which are typically 3-5% of the amount you transfer.

Home Equity Loan or Line of Credit (HELOC)

For homeowners, it can be tempting to use their home’s equity to secure a loan with a very low interest rate. While this can be effective, it comes with a significant and serious risk. You are securing the new financing with your house. This means if you fail to make the payments for any reason, the lender could begin foreclosure proceedings, and you could lose your home. This option should be considered with extreme caution.

The Pros and Cons: A Balanced View

Debt consolidation can be a great tool, but it’s not a magic solution. It’s essential to weigh the advantages and disadvantages carefully.

The Potential Pros:

- Simplicity: Managing one payment is far less stressful than juggling many.

- Lower Interest Rate: The opportunity to secure a lower interest rate is the biggest benefit. It can potentially save you hundreds or thousands of dollars in interest charges.

- Fixed Payoff Date: With a consolidation loan, you have a clear timeline. You know exactly when you will be debt-free, which can be highly motivating.

- Potential Credit Score Boost: When you pay off your credit cards with an installment loan, your credit utilization ratio drops significantly. Since this ratio is a major factor in your credit score, this can lead to an improvement over time.

The Potential Cons:

- It’s Not a Cure for Bad Habits: Consolidation is like reorganizing the clutter in a messy room into one neat box. The room looks better, but if you don’t stop bringing in more clutter, you’ll just have a neat box in a messy room again. You must address the spending habits that led to the debt.

- Temptation to Spend More: After you pay off your credit cards, you suddenly have thousands of dollars in open lines of credit again. This can be a dangerous temptation. Without discipline, you could easily run up new balances, leaving you in a worse position than before.

- Upfront Fees: Some personal loans have origination fees. Balance transfer cards almost always charge a transfer fee. You must factor these costs into your calculation to see if you are truly saving money.

- Longer Repayment Term: A consolidation loan might lower your monthly payment by extending the repayment period. If the new interest rate isn’t much lower, you could end up paying more in total interest over this longer term.

A Practical Scenario: How Sarah Simplified Her Finances

Sarah had accumulated debt across three different high-interest store credit cards, with balances totaling $8,000. Each card had an interest rate over 20%. She felt like her monthly payments were mostly going toward interest charges, making it impossible to get ahead.

Her credit score was still in a decent range, so she shopped around for a personal loan. She was approved for a three-year, $8,000 loan—a new financing option—with a fixed interest rate of 11%.

She used the loan funds to pay off all three credit cards in full. Then, to avoid temptation, she closed two of the store card accounts and kept only one for emergencies. Now, Sarah has just one predictable monthly payment for her loan. Because her new interest rate is nearly half of what she was paying before, a much larger portion of her payment reduces her principal balance each month. She saves money on interest and has a clear plan to be debt-free in three years.

Conclusion

Debt consolidation is not a magic wand. However, for the right person in the right situation, it can be a powerful and effective strategic tool to regain control of their finances. By simplifying your payments and lowering your overall interest rate, it can provide the clarity and structure needed to get out of debt for good. The success of this strategy, however, rests entirely on your commitment to responsible financial habits moving forward. It is a “reset button,” not a free pass.

Before choosing this path, it is essential to honestly assess the behaviors that led to the debt. You must also create a budget that ensures you can live within your means. When you use it as part of a larger plan for financial change, consolidation can be the first, most powerful step on a clear path to becoming debt-free.