Introduction

Interest rates are among the most influential yet least understood drivers of the global economy. They shape everything from mortgage payments to stock market trends, influencing both individual households and multinational corporations. A slight adjustment by a central bank can ripple through every aspect of financial life, affecting borrowing, saving, and investing.

In today’s rapidly shifting economic climate—characterized by inflationary pressures, global debt challenges, and technological disruption—understanding interest rates has become a critical skill. Far from being just a technical term for economists, they hold direct consequences for personal wealth, business growth, and government stability.

This article explores the mechanics of interest rates, their impact on daily financial decisions, the global forces that drive them, and practical strategies for using this knowledge to protect and grow wealth.

What Are Interest Rates and Why Do They Matter?

At their simplest, interest rates represent the cost of borrowing money or the reward for saving it. For borrowers, they determine how much extra must be repaid beyond the original loan amount. For savers and investors, they determine the yield or return on deposited funds.

But their influence extends far beyond simple lending. Interest rates function as the heartbeat of the global economy. When rates rise, borrowing slows, spending decreases, and inflation is often tamed. When rates fall, borrowing accelerates, investment increases, and economic activity is stimulated.

This balancing act makes interest rates one of the most powerful tools used by central banks such as the U.S. Federal Reserve or the European Central Bank to maintain economic stability.

The Mechanics of Interest Rate Changes

Understanding how interest rates shift requires examining the interplay of key economic forces:

-

Inflation: High inflation typically prompts central banks to raise rates to cool spending.

-

Economic Growth: During periods of expansion, rates may rise to prevent overheating.

-

Unemployment: High unemployment often leads to rate cuts to encourage business investment.

-

Global Events: Geopolitical tensions, pandemics, and crises often drive sudden rate adjustments.

For example, when the Federal Reserve raises its benchmark interest rate, commercial banks quickly pass those higher borrowing costs onto consumers through mortgages, car loans, and credit cards. Simultaneously, savings accounts and bonds may yield better returns, incentivizing people to save instead of spend.

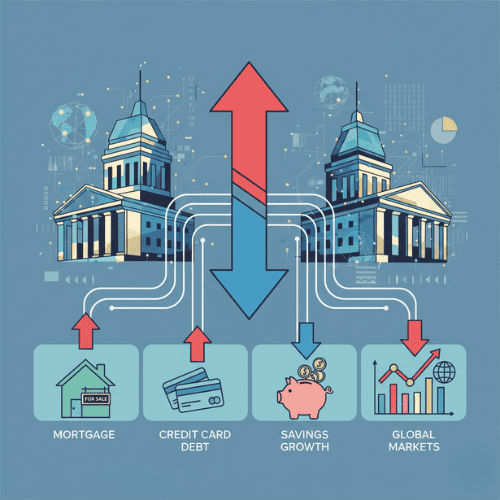

How Interest Rates Affect Personal Finances

The impact of interest rates is deeply personal. Even small changes can significantly influence financial outcomes:

-

Mortgages and Homeownership

Mortgage rates are directly tied to broader interest rate environments. A 1% increase in rates can translate into thousands of dollars in additional payments over the lifetime of a home loan. -

Credit Cards and Personal Loans

Credit card debt becomes more expensive when rates climb. For individuals carrying balances, this can create a heavy financial burden. -

Savings and Investments

Rising rates often improve returns on savings accounts, CDs, and bonds. However, they may also lead to volatility in stock markets as investors shift toward safer fixed-income products. -

Retirement Planning

Interest rates influence annuities, pension yields, and investment portfolios. Low-rate environments may push retirees toward riskier assets to secure sufficient income.

The Global Perspective on Interest Rates

Interest rates do not operate in isolation. They are deeply connected to global capital flows and trade. For instance:

-

United States: As the world’s largest economy, U.S. rate decisions often dictate global trends. A strong U.S. dollar typically follows rate hikes, impacting exports and emerging markets.

-

European Union: The ECB’s monetary policy heavily affects not just Europe but also surrounding economies.

-

Emerging Markets: Countries like Brazil or India often struggle with balancing inflation control against economic growth, leading to higher and more volatile interest rates.

-

Japan: Known for its ultra-low or even negative interest rate policies, Japan demonstrates the extreme measures sometimes taken to stimulate stagnant economies.

Interest Rates and Business Strategy

For businesses, interest rates shape critical strategic decisions:

-

Capital Expansion: Higher borrowing costs can delay or cancel major projects.

-

Cash Flow Management: Fluctuating loan rates directly affect operational costs.

-

Investor Behavior: Low rates often push investors toward equities, boosting stock markets.

-

Debt Refinancing: Companies with high leverage pay close attention to rate cycles, refinancing during low-rate periods to lock in better terms.

Thus, understanding interest rate trends is essential not only for CFOs but also for small business owners aiming to grow sustainably.

Strategies to Protect and Grow Wealth Amid Interest Rate Fluctuations

Navigating interest rate cycles requires proactive financial management. Here are strategies individuals and businesses can adopt:

-

Diversify Investments

Balancing equities, bonds, and alternative assets ensures that portfolios are not overly exposed to rate swings. -

Lock In Fixed Rates

Refinancing mortgages or loans during low-rate environments secures long-term savings. -

Build Emergency Funds

High-rate environments often tighten access to cheap credit. A robust emergency fund reduces dependence on expensive loans. -

Explore Inflation-Protected Securities

Treasury Inflation-Protected Securities (TIPS) and similar instruments safeguard against erosion of purchasing power. -

Be Strategic with Debt

Prioritize paying down high-interest debt (like credit cards) first, especially in rising rate environments. -

Stay Informed

Monitoring central bank policies and global economic indicators helps individuals anticipate shifts before they fully impact personal finances.

Psychological and Behavioral Impacts of Interest Rates

Beyond the numbers, interest rates also affect human behavior. When borrowing costs rise, consumer confidence often declines, leading to reduced spending. Conversely, low interest rates may foster a “cheap credit” culture, encouraging risky financial behavior and over-leveraging.

Understanding these psychological dynamics is crucial for both individuals and policymakers. Decisions driven by fear or overconfidence often create long-term financial vulnerabilities.

The Future of Interest Rates

The future of interest rates is likely to be shaped by a combination of:

-

Artificial Intelligence in Monetary Policy: AI may soon help central banks make more precise interest rate decisions.

-

Climate Change Economics: Green investments and sustainability projects may influence rate-setting strategies.

-

Global Debt Crisis: With global debt at record highs, central banks face pressure to balance growth with repayment feasibility.

-

Digital Currencies: The rise of central bank digital currencies (CBDCs) could redefine how interest rates are transmitted across economies.

The next decade may bring unprecedented volatility as global economies navigate technological disruption, demographic shifts, and climate-related challenges.

Conclusion

Interest rates are more than a technical financial mechanism—they are the silent architects of economic life. Whether you are a homeowner, investor, entrepreneur, or policymaker, understanding how they work and anticipating their shifts is crucial to financial success.

By diversifying investments, managing debt wisely, and keeping a long-term perspective, individuals can not only shield themselves from the negative effects of rising rates but also seize opportunities created by rate cycles.

In a world where uncertainty is the only constant, mastering the dynamics of interest rates offers a pathway to stability, resilience, and wealth creation.