Introduction

If you follow financial news, you’ve likely heard the terms “inflation” and “interest rate” mentioned constantly. These two economic forces are locked in a perpetual dance, a delicate push-and-pull that shapes national economies and, more importantly, has a direct impact on your personal finances. Understanding this relationship is key to making sense of why your savings account might suddenly offer a better return, or why the cost of a new car loan has gone up. For anyone looking to secure financing or manage their debt, this knowledge is not just academic—it’s essential. This guide will break down the crucial connection between inflation and the interest rate, explaining how they influence each other and what it all means for your budget, your credit card, and your overall financial planning.

What is Inflation? A Quick Refresher

Before we can understand the dance, we need to know the dancers. In simple terms, inflation is the rate at which the general level of prices for goods and services rises, which in turn causes the purchasing power of a currency to fall. It’s the reason that a cup of coffee that cost $3 a few years ago might cost $3.50 today. Your dollar just doesn’t stretch as far as it used to.

A moderate level of inflation is generally considered normal and is a sign of a healthy, growing economy where demand is strong. However, when inflation becomes too high, it can be damaging. It erodes the value of your savings and can strain household budgets as the cost of everyday necessities like food, gas, and housing increases faster than wages.

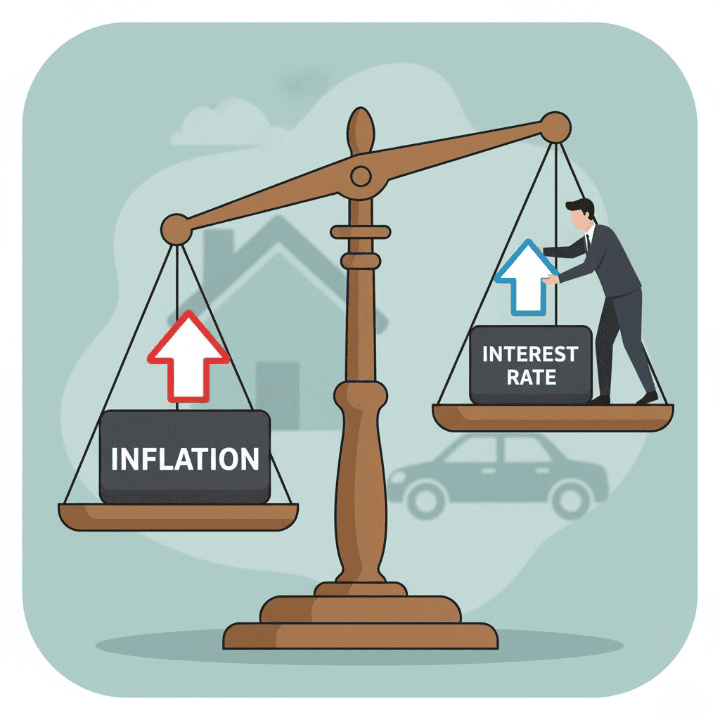

The Central Bank’s Role: The Main Tool is the Interest Rate

This is where a country’s central bank (like the U.S. Federal Reserve or the Banco Central do Brasil) steps in. One of the primary jobs of a central bank is to maintain price stability, which means keeping inflation under control. Their most powerful tool for accomplishing this is the ability to adjust the national benchmark interest rate.

Think of this benchmark rate as the foundation upon which all other rates are built. It’s the rate at which commercial banks borrow from each other and from the central bank. The central bank’s actions create a ripple effect throughout the entire economy.

- When Inflation is High: The central bank will raise the benchmark interest rate. This makes borrowing money more expensive for everyone. The goal is to cool down the economy by discouraging spending and borrowing. When people and businesses spend less, demand for goods and services decreases, which helps to bring prices down and curb inflation.

- When Inflation is Low or the Economy is Weak: The central bank will lower the benchmark interest rate. This makes borrowing cheaper, which incentivizes people and businesses to take out loans for financing major purchases and investments. This increased spending stimulates economic growth.

How This “Push and Pull” Affects You Directly

These macroeconomic policies might seem distant, but they have a very real and direct impact on your wallet. Here’s how that push-and-pull between inflation and the interest rate affects your personal finances.

Your Financing Costs

When the central bank raises the interest rate to fight inflation, the cost of all new financing rises as well. If you are looking to get a mortgage for a new home, an auto loan for a car, or a personal loan, the rate you are offered will be higher than it was when rates were low. This means your monthly payments will be larger, and you will pay more in total interest over the life of the loan.

Your Credit Card Debt

This is where the impact is often felt most immediately. The vast majority of credit card accounts have a variable interest rate. This rate is typically calculated as a benchmark rate (like the Prime Rate, which moves in lockstep with the central bank’s rate) plus a margin. When the central bank raises its rate by 0.50%, your credit card’s APR will likely increase by that same 0.50% within a billing cycle or two. This makes carrying a credit card balance significantly more expensive during periods of high inflation.

Your Savings Account

There is a silver lining, though it often appears slowly. When the benchmark interest rate rises, banks also begin to offer higher rates on their savings products, especially high-yield savings accounts. This allows your savings to earn more. However, the goal for any saver is to find an account where the interest rate is higher than the rate of inflation. Earning a 3% interest rate is great, but if inflation is at 4%, your money is still losing purchasing power over time.

The Impact on Your Broader Financial Health and Credit

The combination of high inflation and rising interest rates can create a “double whammy” for household budgets. On one side, the cost of everyday life is going up. On the other, the cost of any debt you hold is also increasing. This squeeze can make it much more difficult to make ends meet each month.

This financial pressure can put your credit score at risk. When budgets are tight, the likelihood of missing a payment on a loan or credit card increases. A single missed payment can have a significant negative impact on your credit. Furthermore, the economic uncertainty and stress of navigating this environment can take a toll on your mental and physical health, creating anxiety about your financial future.

What About Insurance Premiums?

The insurance industry is also affected by these economic forces. Inflation increases the cost of everything that insurance policies cover. The cost of auto parts and labor for car repairs goes up. The cost of lumber and materials to rebuild a home increases. Medical procedure costs rise. To cover these higher potential claim payouts, insurance companies often need to raise their premiums. This can be another expense that gets added to a household’s already strained budget during inflationary times.

Conclusion

The relationship between inflation and the interest rate is the primary mechanism that central banks use to steer the economy. While you cannot control these large-scale forces, understanding them is incredibly empowering. This knowledge helps you understand why the terms on your financing are changing and why your credit card debt might be getting more expensive. It reinforces the importance of timeless financial principles: building an emergency fund, aggressively managing high-interest debt, and protecting your credit. By understanding the bigger picture, you can navigate any economic climate with greater confidence and make smarter decisions for your financial life.