Introduction

In the vast world of personal finance, few concepts are as powerful or as influential as the interest rate. It operates silently in the background of nearly every financial decision we make. Think of it as a financial current; sometimes it flows in your favor, helping your savings grow, and other times it flows against you, increasing the cost of your debts. Understanding this force is essential for anyone looking to build a stable financial future. The interest rate dictates the cost of your car financing, the earnings on your savings account, and the penalty for carrying a credit card balance. This guide is designed to demystify the concept of the interest rate. We will explore what it is, how it is determined, and how it directly impacts your credit and your ability to secure affordable financing.

What Exactly Is an Interest Rate?

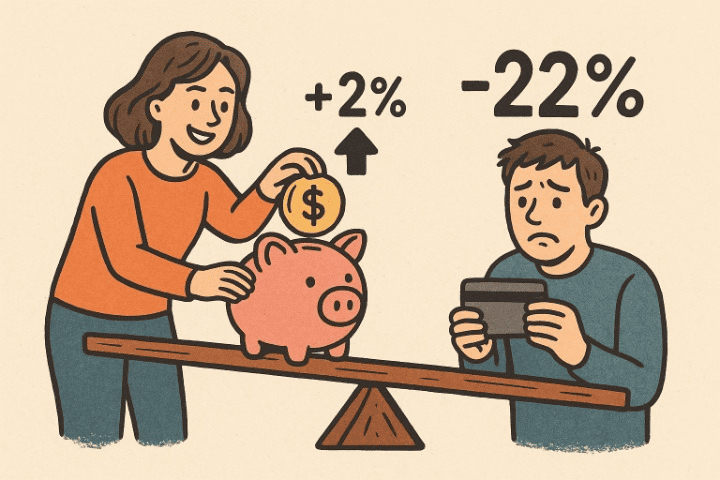

At its core, an interest rate is the cost of borrowing money. It is expressed as a percentage of the principal amount (the amount borrowed). However, it’s a two-sided coin. When you are the borrower, you pay interest. When you are the lender or saver, you earn interest.

Let’s break down both sides:

- As a Cost: When you take out a loan for financing a car or use your credit card to make a purchase you don’t pay off right away, you are borrowing money. The lender charges you an interest rate for the convenience of using their money. This is their profit and your cost.

- As a Reward: When you deposit money into a savings account, you are essentially lending your money to the bank. The bank then pays you an interest rate as a reward for letting them use your funds. The bank, in turn, lends that money out to other customers at a higher interest rate.

This number is typically shown as an Annual Percentage Rate (APR). The APR represents the yearly cost of a loan, including interest and certain fees. Understanding the APR is crucial because it allows you to make an apples-to-apples comparison between different financial products.

The Powerful Link Between Interest Rate and Your Credit

Your credit score and the interest rate you are offered on a loan have a direct and critical relationship. Lenders are in the business of managing risk. Before they approve you for financing, they need to predict how likely you are to pay the money back on time. Your credit score is the primary tool they use to make this assessment.

A high credit score signals to lenders that you are a reliable, low-risk borrower. To compete for your business, they will offer you their best terms, which includes a low interest rate. A low credit score, on the other hand, signals higher risk. It suggests you may have had trouble managing debt in the past. To compensate for this increased risk, lenders will charge you a much higher interest rate.

Imagine two friends, Alex and Ben, both want to get financing for a $20,000 car over five years.

- Alex has excellent credit and qualifies for a 5% interest rate. His monthly payment would be around $377, and he would pay about $2,645 in total interest.

- Ben has poor credit and is offered a 15% interest rate. His monthly payment would be around $476, and he would pay about $8,550 in total interest.

Over the life of the loan, the higher interest rate costs Ben nearly $6,000 more for the exact same car. This powerful example shows that building good credit is one of the most effective ways to save money on all future financing needs.

Interest Rates in Action: From Savings to Credit Card Debt

You encounter interest rates in many different areas of your financial life. Here are a few common examples:

- Savings Accounts: These offer a variable interest rate on your deposits. While typically low, they provide a safe way to earn a small return on your money.

- Mortgages: When you get financing for a home, even a small difference in the interest rate can save you tens of thousands of dollars over the 30-year term. Home loans can have a fixed interest rate, which stays the same, or a variable one, which can change over time.

- Auto Loans: Similar to mortgages, the interest rate on car financing is a key factor in the total cost. A lower rate can significantly reduce your monthly payment.

- Credit Card Balances: A credit card often has one of the highest interest rates of any financial product. Because the debt is unsecured (not backed by an asset like a car or house), the risk for the lender is higher. This is why carrying a credit card balance can become very expensive, very quickly due to the effects of compound interest.

The Broader Economic Picture: Who Sets Interest Rates?

The interest rates you see offered by banks are heavily influenced by the decisions of a country’s central bank (like the Federal Reserve in the United States). The central bank sets a baseline interest rate that determines how cheaply commercial banks can borrow money. This, in turn, influences the rates those banks offer to consumers like you.

Central banks adjust this baseline rate for two main reasons:

- To Stimulate the Economy: If the economy is slow, the central bank may lower interest rates. This makes borrowing cheaper, which encourages businesses and individuals to take out loans, spend money, and invest.

- To Fight Inflation: If prices are rising too quickly (inflation), the central bank may raise interest rates. This makes borrowing more expensive, which tends to slow down spending and help bring prices under control.

When you hear on the news that the central bank has raised rates, you can expect that the interest rate on new savings accounts, mortgages, and your credit card will likely rise as well.

The Indirect Connection to Insurance and Financial Health

At first glance, insurance and interest rates might not seem related. However, they are connected through the concept of risk management and overall financial health. The purpose of insurance (health, auto, home) is to provide a financial safety net against unexpected, large expenses.

If you don’t have adequate insurance, a major medical emergency or a car accident could force you to seek emergency financing to cover the costs. This debt will almost certainly come with a high interest rate, especially during a stressful time, potentially creating a long-term financial burden. In this way, having the right insurance protects you from having to take on high-interest debt. Maintaining good financial health involves a holistic approach. It means working to build good credit, seeking a low interest rate on any necessary financing, and protecting yourself with proper insurance to avoid financial shocks.

Conclusion

The interest rate is a fundamental force in the world of personal finance. It is the price you pay for financing and the reward you earn for saving. It is deeply connected to your credit, acting as a reflection of your financial reliability. While the economic factors that influence rates may be complex, the principle for your own life is simple: strive to minimize the interest you pay and maximize the interest you earn. By paying close attention to this crucial number on every financial product you consider—from a simple savings account to a complex mortgage—you empower yourself to make smarter decisions, save money, and build a more secure financial future.