Introduction

Managing your health and your finances are two of the most important responsibilities in adult life, and they are deeply interconnected. While most of us understand the critical role of health insurance, there is another powerful financial tool designed to work alongside it that many people overlook: the Health Savings Account, or HSA. Too often, people think of an HSA as just another savings account for doctor’s visits. In reality, it is one of the most unique and advantageous accounts in the entire financial world. An HSA is a financial superpower in disguise, offering a combination of tax benefits that no other account can match. It can help you manage your current medical costs, grow an investment portfolio, and even build a nest egg for retirement. This guide will illuminate what an HSA is and how you can use it to take control of both your healthcare costs and your long-term financial future.

What is a Health Savings Account (HSA)?

An HSA is a tax-advantaged savings account that you can use to pay for qualified medical expenses. Think of it as a personal savings account, but specifically designated for your health needs. However, there is one crucial requirement for opening and contributing to an HSA: you must be enrolled in a qualified High-Deductible Health Plan (HDHP).

An HDHP is a type of health insurance plan with a higher deductible than traditional plans, but in exchange, it typically has a lower monthly premium. The idea is that you pay less for your monthly insurance coverage and can use the savings to contribute to your own HSA, giving you more control over your healthcare spending. This direct link between the HSA and a specific type of insurance plan is fundamental to how the account is designed to work.

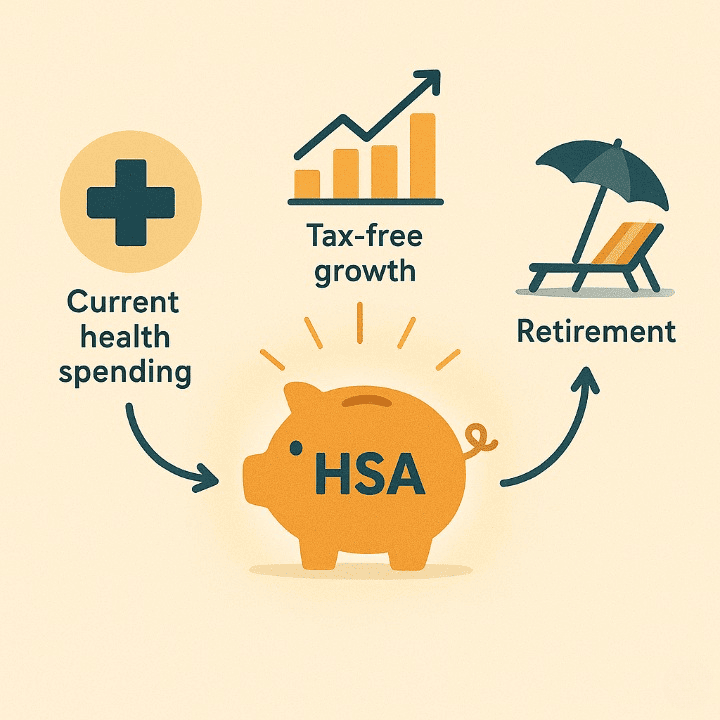

The “Triple-Tax Advantage”: The HSA’s Superpower

The reason financial experts are so enthusiastic about HSAs is because of their unique “triple-tax advantage.” This is what makes the account more powerful than even a 401(k) or an IRA.

- Tax-Deductible Contributions: The money you contribute to an HSA is tax-deductible (or pre-tax if done through an employer). This means your contributions for the year are subtracted from your gross income, which lowers your overall taxable income. You get a tax break just for saving.

- Tax-Free Growth: The money in your HSA can grow over time, either by earning interest or through investments. Unlike a standard investment account, all of this growth is completely tax-free. You will never pay taxes on the earnings your account generates.

- Tax-Free Withdrawals: You can withdraw money from your HSA at any time to pay for qualified medical expenses, and these withdrawals are also completely tax-free.

This combination—tax-free in, tax-free growth, and tax-free out for medical costs—is unparalleled. It is the only account that offers this powerful trifecta of tax benefits.

Beyond a Savings Account: Using Your HSA for Spending and Investing

An HSA is a dynamic tool that can be used for both short-term needs and long-term growth.

For Short-Term Spending

You can use your HSA funds to pay for a vast range of qualified medical, dental, and vision expenses that your insurance may not fully cover. This includes doctor visit copays, prescription medications, dental work, new glasses or contact lenses, and much more. Most HSAs come with a dedicated debit card, making it simple and convenient to pay for these expenses directly from your account.

For Long-Term Investing

This is the feature that transforms an HSA from a simple savings account into a powerful wealth-building tool. Once your account balance reaches a certain minimum threshold (which varies by provider), you have the option to invest a portion of your funds in a portfolio of mutual funds, ETFs, or other assets, similar to a 401(k). By investing your HSA funds, you give them the potential to grow significantly over decades, far beyond what they would earn in a standard savings account.

The Long-Term Vision: Your HSA as a Secret Retirement Tool

One of the best features of an HSA is that the funds are yours to keep, forever. Unlike a Flexible Spending Account (FSA), HSA balances are not “use-it-or-lose-it.” The money rolls over year after year, allowing you to build a substantial nest egg.

This is where the HSA reveals its final superpower: as a retirement account. While you can always use the funds tax-free for medical expenses at any age, something special happens when you turn 65. At that point, you can withdraw money from your HSA for any reason—a vacation, home repairs, or just daily living expenses—without penalty. For these non-medical withdrawals, you will simply pay regular income tax on the amount, just as you would with a traditional 401(k) or IRA. This flexibility makes the HSA an incredible supplemental retirement account, with the added bonus that any money you do use for health care in retirement remains completely tax-free.

A Practical Scenario: How Amelia Uses Her HSA

Let’s look at how an HSA can function over a lifetime.

- Amelia, age 30, enrolls in her company’s HDHP and opens an HSA. She sets up an automatic contribution from each paycheck. For the first few years, she uses her HSA debit card to pay for dental cleanings and prescription copays, appreciating the immediate tax savings.

- By age 40, her HSA balance has grown. She has more than the minimum required to invest, so she allocates a portion of her funds to a diversified portfolio of low-cost index funds. She continues to contribute regularly, allowing her investments to grow tax-free.

- At age 65, Amelia retires. Thanks to years of contributions and tax-free market growth, her HSA has grown into a substantial fund. She can now use this money completely tax-free to pay for her Medicare premiums and other health-related costs in retirement. If she needs extra cash for a trip, she can also withdraw from the account for non-medical reasons, simply paying income tax on that portion.

Amelia’s story shows how the HSA evolved with her, serving as a spending account in her early years, an investment vehicle in her middle years, and a powerful retirement and health fund in her later years.

Conclusion

A Health Savings Account is one of the most powerful and versatile financial tools available, yet it remains widely underutilized. It offers a direct way to manage your current health costs, provides a unique and powerful triple-tax advantage, and serves as a flexible, long-term vehicle for both investing and retirement planning. If your health insurance plan makes you eligible for an HSA, taking the time to understand and utilize it is a critical step in taking full control of your financial well-being. It’s an investment in both a healthier and a wealthier future.