Introduction

You have likely seen the headlines. First, news reports talk about rising prices and a high “inflation” rate. Then, shortly after, you hear that the central bank is “raising the interest rate.” Have you ever wondered why these two events are so closely linked? It’s not a coincidence. The relationship between inflation and interest rates is one of the most powerful forces in our economy, and it has a direct impact on your personal finances—from the return on your savings account to the cost of financing a new car. Understanding this connection can feel like trying to solve a complex economic puzzle. However, at its core, it’s a straightforward concept that, once understood, can help you make smarter financial decisions. This guide will demystify this crucial relationship and explain what it means for your wallet.

What is Inflation? The Shrinking Power of Your Money

Before we can connect it to interest rates, let’s first understand inflation. In simple terms, inflation is the rate at which the general level of prices for goods and services is rising, and as a result, the purchasing power of your money is falling.

Imagine a simple example: the cup of coffee you buy every morning.

- Last year, that cup of coffee cost you $3.00.

- This year, due to inflation, that same cup of coffee now costs $3.20.

The coffee itself hasn’t changed, but the value of your money has. The same dollar bill now buys you less than it did a year ago. When this happens across the entire economy for everything from groceries to gasoline, we have inflation. A small amount of inflation is considered normal for a growing economy, but when it gets too high, it becomes a problem.

The Central Bank’s Role: The Fight Against Inflation

Every country has a central bank (like the Federal Reserve in the United States) whose job is to act as the manager of the economy. One of its most important goals is to maintain price stability, which means keeping inflation low and predictable. When inflation starts to rise too quickly, it erodes the savings of citizens and creates economic uncertainty. To combat this, the central bank’s primary and most powerful tool is its ability to adjust the benchmark interest rate. When inflation is high, the standard response is to raise this key interest rate.

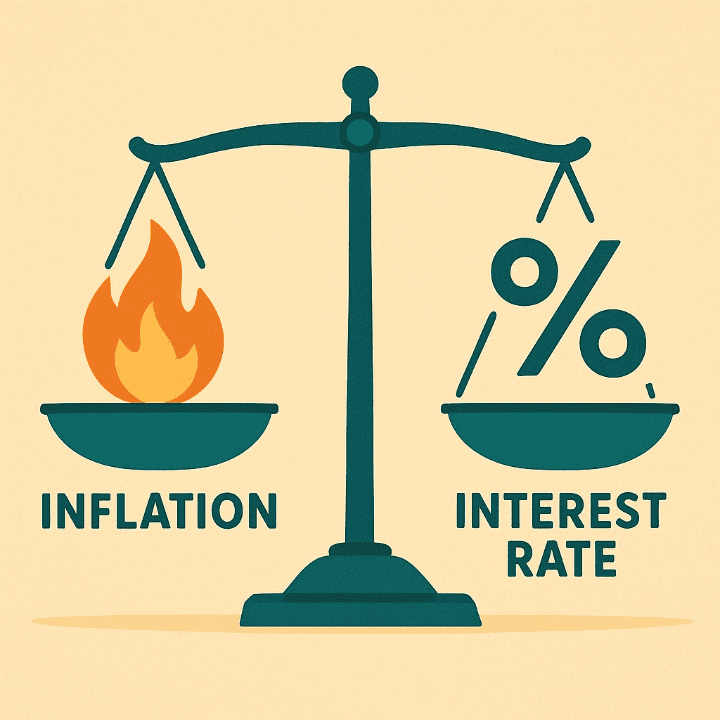

The Core Connection: Why Raising Interest Rates Fights Inflation

So, why does raising the cost of borrowing money help to control rising prices? It all comes down to the simple economic principle of supply and demand. Raising the interest rate is like gently tapping the brakes on a “hot” or overheating economy.

Here’s how it works:

- Borrowing Becomes More Expensive: The central bank’s rate influences the rates that commercial banks offer to their customers. When the benchmark rate goes up, it becomes more expensive for you to get financing for a new home or car. The interest rate on your credit card debt will also likely increase.

- Spending Cools Down: Because it’s more expensive to borrow, people and businesses tend to cut back on spending. A family might postpone buying a new house. A business might delay a major expansion that required a loan. This reduces the overall demand for goods and services in the economy.

- Saving Becomes More Attractive: The flip side is that higher interest rates make it more rewarding to save money. The interest rate (APY) you earn on a high-yield savings account will rise, giving you more incentive to save rather than spend.

When people and businesses spend less and save more, the total demand in the economy decreases. This reduction in demand helps to alleviate pressure on prices, causing inflation to slow down.

What This Means for Your Wallet: The Real-World Impact

This macroeconomic dance has a very real impact on your personal finances, creating both challenges and opportunities.

- For Borrowers: A high-interest-rate environment is generally bad news. If you are looking to take on new financing, you will face higher monthly payments and pay more in total interest over the life of the loan. Variable-rate debts, like most credit card balances, will become more expensive as their rates adjust upward.

- For Savers: This is where the news is good. A period of rising interest rates means your savings will work harder for you. The returns on high-yield savings accounts, certificates of deposit (CDs), and other savings vehicles will increase, helping your money grow faster and better combat the effects of inflation.

It’s a double-edged sword: the same force that makes your mortgage more expensive also boosts your savings account.

A Practical Scenario: The Car Buyer’s Dilemma

Let’s look at two cousins, Chloe and Leo, who are both planning to buy the exact same car.

- Chloe bought her car last year when inflation was low and the economy was stable. She was able to secure an auto loan with a fixed interest rate of 4%. Her monthly payments are manageable and predictable.

- Leo decides to wait a year to buy his car. During that year, inflation rises sharply. In response, the central bank raises its benchmark interest rate several times. When Leo goes to get financing, the economic climate has changed. The best interest rate he can qualify for is now 7%.

Even though they are buying the same car, Leo’s monthly payment is significantly higher than Chloe’s simply because of the change in the interest rate environment. Over the five-year term of the loan, he will end up paying thousands of dollars more in total interest than his cousin did. This perfectly illustrates the direct link between the wider economy and the cost of personal financing.

Conclusion

Inflation and interest rates are locked in a delicate dance, carefully orchestrated by central banks to keep the economy in balance. When the cost of living rises too quickly, the cost of borrowing is intentionally increased to cool things down. For you, this has a clear and direct impact. It means the cost of your future financing—from a small personal loan to a large mortgage—is heavily influenced by the rate of inflation today. At the same time, it dictates the returns you can expect on your savings. Understanding this fundamental relationship doesn’t require a degree in economics, but it does provide you with the crucial context to navigate the ever-changing financial world and make more informed decisions for your money.