Introduction: The Battle of Budgeting Strategies

Managing your money effectively is crucial for building lasting wealth. For many, the journey to financial prosperity begins with a solid budget. Budgeting helps you understand where your money goes. Consequently, this allows you to make intentional choices about spending and saving. However, with various budgeting philosophies available, choosing the right method can feel overwhelming. Currently, the debate often centers on Zero-Based Budgeting vs 50/30/20 Rule. These are two of the most popular and highly effective approaches available today.

Each method offers a distinct framework for handling your income and expenses. Yet, investors often ask: which one truly accelerates wealth accumulation? This article will delve deeply into both strategies. We will explore their mechanics, benefits, and drawbacks. Ultimately, we aim to help you determine which approach aligns best with your financial goals. By analyzing Zero-Based Budgeting vs 50/30/20 Rule, we will guide you toward the path that builds wealth faster for your specific situation.

Understanding Zero-Based Budgeting

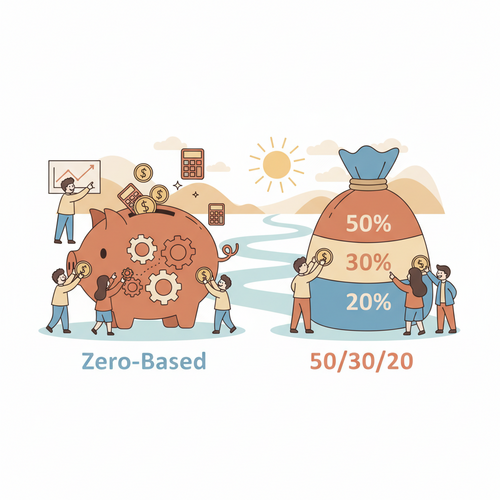

To fully grasp the comparison of Zero-Based Budgeting vs 50/30/20 Rule, we must first dissect the zero-based approach. Zero-Based Budgeting is a method where every single dollar of your income receives a specific job. Think of it this way: at the start of each month, you allocate every dollar you expect to earn. Specifically, you assign it to an expense, a saving goal, or debt repayment. Therefore, your income minus your expenses should equal zero.

This approach demands a high level of intentionality. You are not merely tracking spending. Instead, you are actively deciding the fate of every dollar before you spend it. No money remains unaccounted for. On the contrary, each penny serves a purpose that you define explicitly.

How Zero-Based Budgeting Works

Implementing a zero-based budget involves a few disciplined steps. Consistency is key here.

- Calculate Your Income: First, determine your total expected income for the month. This includes salaries, side hustles, or any other regular cash flow.

- List All Expenses: Next, itemize all your fixed and variable expenses. Fixed expenses might include rent or mortgage payments. Variable expenses cover groceries and entertainment.

- Assign Every Dollar: This is the core of the method. Allocate your income to these categories until the total allocated equals your total income. Ensure that “income – expenses = 0.”

- Track and Adjust: Throughout the month, diligently track your spending. Life happens, so be prepared to adjust. If you overspend in one area, you must reduce spending in another immediately.

This method fosters a deep understanding of your financial inflows. Ideally, it empowers you to take complete control. You become the master of your finances, rather than a passive observer.

Pros and Cons of Zero-Based Budgeting

Zero-based budgeting offers significant advantages. However, it also presents challenges.

Pros: You have precise control over where every dollar goes. This eliminates mindless spending. Furthermore, it promotes conscious financial decisions. By scrutinizing every expense, you easily spot unnecessary waste. Consequently, you can reallocate funds towards savings. It is exceptionally powerful for achieving specific goals like debt elimination.

Cons: Setting up this budget requires time. It needs regular review. Success hinges on strict discipline. Unfortunately, a lack of consistency can quickly derail the budget. Additionally, some individuals find the detailed allocation too restrictive.

Deciphering the 50/30/20 Rule

Now, let us examine the second contender in the Zero-Based Budgeting vs 50/30/20 Rule comparison. The 50/30/20 Rule is a straightforward guideline. Ideally, it allocates your after-tax income into three broad categories: Needs, Wants, and Savings. Popularized by Senator Elizabeth Warren, this method offers a simpler alternative to granular tracking.

It provides a flexible framework. Primarily, it helps you prioritize essential spending. Simultaneously, it allows room for discretionary purchases. The rule simplifies budgeting by focusing on percentages rather than individual dollar amounts.

How the 50/30/20 Rule Works

The application of the 50/30/20 Rule is relatively simple and user-friendly.

- 50% for Needs: This category covers essential expenses. You cannot live without them. Examples include housing, utilities, groceries, and insurance. These are the non-negotiables.

- 30% for Wants: Wants are discretionary expenses. They improve your quality of life but are not strictly necessary. This includes dining out, subscriptions, and vacations. This category provides flexibility.

- 20% for Savings and Debt: This crucial portion builds your financial future. It includes retirement contributions and debt repayment. It effectively pays your future self.

The beauty of this rule lies in its ease. You simply divide your net income. Then, you manage your spending within those buckets.

Pros and Cons of the 50/30/20 Rule

The 50/30/20 Rule appeals to many due to its simplicity.

Pros: It is easy to understand. This makes it an excellent starting point for beginners. You do not need to track every transaction. Within each category, you have freedom. For example, you decide how to spend your 30% “Wants” money without detailed restrictions. It encourages healthy financial habits without being overly rigid.

Cons: You have less oversight on individual items. It is possible to overspend within a category without realizing it. Furthermore, if you have significant debt, 20% might not be enough. You might need to adjust these percentages to accelerate progress. Also, it works best for those with a stable income.

Zero-Based Budgeting vs 50/30/20 Rule: A Head-to-Head Comparison

Now, let us directly compare Zero-Based Budgeting vs 50/30/20 Rule to see which builds wealth faster. The answer often depends on your psychological approach to money.

Control and Intentionality

Zero-Based Budgeting offers unparalleled control. Every dollar is purposeful. This intentionality means you always direct funds towards your goals. When you actively choose to allocate $500 to investment, it happens. Ideally, this method eliminates “leakage” in your finances.

Conversely, the 50/30/20 Rule provides general guidance. The 20% for savings is crucial. However, it does not specify how that 20% is allocated. Are you focusing on an emergency fund? Or are you aiming for aggressive debt repayment? The rule itself does not dictate this. Therefore, this lack of granular control could mean a slower pace if your 20% is not strategically deployed.

Flexibility and Adaptability

The 50/30/20 Rule shines in terms of flexibility. As long as you stay within the percentages, you can adjust your spending. This makes it adaptable to changing lifestyles. You can handle occasional splurges without overhauling your system.

Zero-Based Budgeting can also adapt. However, it requires more effort. If your income changes, you must re-evaluate. You must reassign every dollar. This meticulousness is beneficial for staying on track. Yet, it demands more mental energy. For many, this constant adjustment feels burdensome.

Which Method Builds Wealth Faster?

This is the critical question in the Zero-Based Budgeting vs 50/30/20 Rule debate. Zero-Based Budgeting generally has the potential to accelerate wealth building significantly faster. Why? Because it forces you to confront every expense. It helps identify and eliminate waste immediately. This freed-up capital can then be channeled directly into high-impact areas.

For someone with substantial debt, a zero-based budget acts as a scalpel. You can cut discretionary spending drastically. For instance, you might allocate 40% of your income to debt repayment instead of the standard 20%. This aggressive approach reduces interest payments rapidly.

On the other hand, the 50/30/20 Rule builds wealth at a consistent pace. It is the “tortoise” in the race. The 20% savings rate is a healthy baseline. However, it might not be enough to achieve aggressive milestones quickly. Nevertheless, its simplicity often leads to greater consistency over years. Consistency is vital for compound interest to work its magic. For data on savings rates and wealth trends, resources like the Federal Reserve Economic Research provide excellent context.

Suitability for Different Financial Stages

Choosing between Zero-Based Budgeting vs 50/30/20 Rule depends on your current financial health.

When to Choose Zero-Based Budgeting

Zero-Based Budgeting is ideal for specific scenarios. If you have significant high-interest debt, choose this. It allows you to attack the principal balance aggressively. Furthermore, if you have a variable income, this method is superior. It ensures you cover necessities during lean months. Also, if you are saving for a massive short-term goal, like a house down payment, the precision of zero-based budgeting is unmatched.

When to Choose the 50/30/20 Rule

The 50/30/20 Rule is perfect for maintenance and steady growth. If you are debt-free (excluding a mortgage), this rule works well. It ensures you enjoy your money today while saving for tomorrow. It is also great for beginners. If the thought of spreadsheets scares you, start here. It builds the muscle of saving without the overwhelm of tracking every penny. It prevents burnout, which is a common reason people stop budgeting.

The Psychological Factor in Wealth Building

Money management is 20% math and 80% behavior. Therefore, understanding your personality is key when analyzing Zero-Based Budgeting vs 50/30/20 Rule.

Do you love data? Do you feel secure when you know where every cent is? Then Zero-Based Budgeting will likely make you wealthier. It gives you a sense of agency. You will find joy in optimizing your categories. You will actively look for ways to reduce the “expenses” category to increase the “savings” category.

However, if you feel restricted by micromanagement, Zero-Based Budgeting might backfire. You might rebel against your own budget. In this case, the 50/30/20 Rule is safer. It allows for “guilt-free” spending within the 30% bucket. This psychological freedom often helps people stick to the plan longer. A “good” plan that you follow is infinitely better than a “perfect” plan that you quit.

Advanced Hybrid Strategies

You do not have to choose strictly between Zero-Based Budgeting vs 50/30/20 Rule. Many successful investors use a hybrid approach. For example, you can use the 50/30/20 ratios to set your macro goals. Then, you can use zero-based principles within the “Wants” category.

Alternatively, use Zero-Based Budgeting for a season. Apply it for six months to kill debt. Once you achieve that milestone, switch to the 50/30/20 Rule. This allows you to relax while maintaining financial health. This flexibility prevents fatigue. It ensures your financial strategy evolves as your life changes.

Tools to Help You Succeed

Regardless of the method, technology can accelerate your progress. For Zero-Based Budgeting, apps like YNAB (You Need A Budget) are fantastic. They are designed specifically for this philosophy. They force you to allocate every dollar. Ideally, they connect to your bank accounts for real-time tracking.

For the 50/30/20 Rule, simpler trackers work well. General finance apps or even a simple automated transfer system are sufficient. Set up an automatic transfer of 20% of your paycheck to a separate savings account immediately. Then, live on the rest. This “pay yourself first” mentality automates the 50/30/20 rule. For investment education to support your 20% bucket, sites like Investopedia offer invaluable resources.

Conclusion: The Verdict on Speed

So, regarding Zero-Based Budgeting vs 50/30/20 Rule, which is faster? For pure speed and aggressive wealth accumulation, Zero-Based Budgeting wins. It minimizes waste. It maximizes allocation to wealth-building assets. It forces you to be hyper-aware of your financial reality. If you are willing to put in the work, it will get you to your destination sooner.

However, the 50/30/20 Rule wins on sustainability for the average person. It builds wealth by ensuring you never stop saving. It protects you from lifestyle creep while allowing you to enjoy life. Ideally, assess your current debt load and your discipline level. Experiment with both. Choose the method that empowers you to take action today. Building wealth is a marathon, not a sprint. The best method is the one that keeps you running.