Introduction

Life is full of surprises, and unfortunately, not all of them are pleasant. A car making a sudden strange noise, a pet needing an urgent visit to the vet, or an unexpected medical bill arriving in the mail—these moments can create a sinking feeling of dread, especially when you’re not financially prepared. This is where an emergency fund comes in. It is the single most important tool for turning a potential financial crisis into a manageable inconvenience. More than just a simple savings account, an emergency fund is the cornerstone of true financial security. It serves as a buffer between you and the chaos of life, protecting you from debt, safeguarding your credit, and reducing the stress that so often harms our health and well-being.

What is an Emergency Fund and Why is it Non-Negotiable?

An emergency fund is a stash of cash set aside specifically for unexpected and essential expenses. It is not a fund for a planned vacation, a down payment on a house, or a new gadget. Its sole purpose is to be there for you when a true emergency strikes. Think of it as your own personal self-insurance policy for life’s smaller, yet still costly, surprises.

This fund acts as a firewall between you and high-interest debt. Without this cash reserve, what is your first move when faced with a $700 car repair bill? For most people, the answer is to reach for a credit card. While convenient, this often marks the beginning of a difficult debt cycle. An emergency fund allows you to handle the situation without resorting to a credit card or seeking other forms of costly last-minute financing. It provides you with options, control, and peace of mind when you need them most, making it a non-negotiable foundation for anyone serious about their personal finance journey.

The True Cost of Not Having an Emergency Fund

To fully appreciate the power of an emergency fund, it’s helpful to visualize the domino effect of not having one. Imagine you are faced with an unexpected $1,000 expense—perhaps a dental emergency or an urgent home repair.

Without an emergency fund, your only choice is likely to put the entire amount on a credit card. If you can’t pay it off at the end of the month, that balance immediately starts to accrue interest. With a typical high interest rate, that $1,000 debt can quickly grow. You end up paying significantly more than the original cost of the emergency. This financial pressure creates stress and anxiety, which can negatively impact your mental and physical health.

Furthermore, this new debt increases your credit utilization ratio—the amount of credit you’re using compared to your total limit. A high utilization ratio can lower your credit score. If the new monthly payment strains your budget and you accidentally miss a payment, the damage to your credit will be even more severe. This single event can set you back for months, making it harder to achieve your other financial goals. An emergency fund prevents this entire negative cascade.

How Much Should You Save? Setting Your Goal

The question of “how much?” can feel intimidating, but the key is to start small and build momentum. Financial experts typically recommend a two-stage approach.

1. The Starter Emergency Fund: Your immediate goal should be to save a starter fund of around $500 to $1,000. This amount is achievable for most people and is enough to cover a wide range of common emergencies, such as a new set of tires, a minor medical co-pay, or an appliance repair. Reaching this first milestone provides an incredible sense of security and motivates you to keep going.

2. The Fully-Funded Emergency Fund: Once you have your starter fund in place, your long-term goal is to save between three to six months’ worth of essential living expenses. To calculate this, add up your non-negotiable monthly costs:

- Housing (rent or mortgage)

- Utilities (electricity, water, internet)

- Food

- Transportation

- Insurance premiums

- Minimum debt payments

Multiplying this total by three to six will give you your target range. This larger fund is designed to support you through a more significant life event, such as a job loss or a serious health issue.

Where to Keep Your Emergency Fund

The money in your emergency fund needs to meet two very important criteria: it must be liquid (meaning you can access it quickly) and it must be safe (meaning its value won’t drop). For this reason, you should never invest your emergency fund in the stock market.

The ideal place for your emergency fund is a high-yield savings account (HYSA). These accounts are typically offered by online banks and have two main advantages:

- They are separate from your regular checking account, which makes you less tempted to dip into the funds for non-emergencies.

- They offer a much better interest rate than a traditional savings account, allowing your money to grow slightly while it sits there.

Strategies for Building Your Fund from Scratch

Saving a large sum of money can seem impossible, but with a consistent strategy, you can get there.

- Automate Your Savings: This is the most effective method. Set up an automatic transfer from your checking account to your high-yield savings account every payday, even if it’s just a small amount to start. This “pay yourself first” approach builds your fund without you having to think about it.

- Dedicate “Found” Money: Any time you receive unexpected money—a tax refund, a work bonus, a cash gift, or money from selling something—deposit it directly into your emergency fund.

- Trim Your Budget Temporarily: Look for one or two non-essential spending categories where you can cut back for a few months and redirect that money to your savings goal.

Remember that your fund works together with your other financial protections. Having good health insurance and auto insurance means your emergency fund only needs to cover your deductible in a major event, not the entire catastrophic cost.

Conclusion

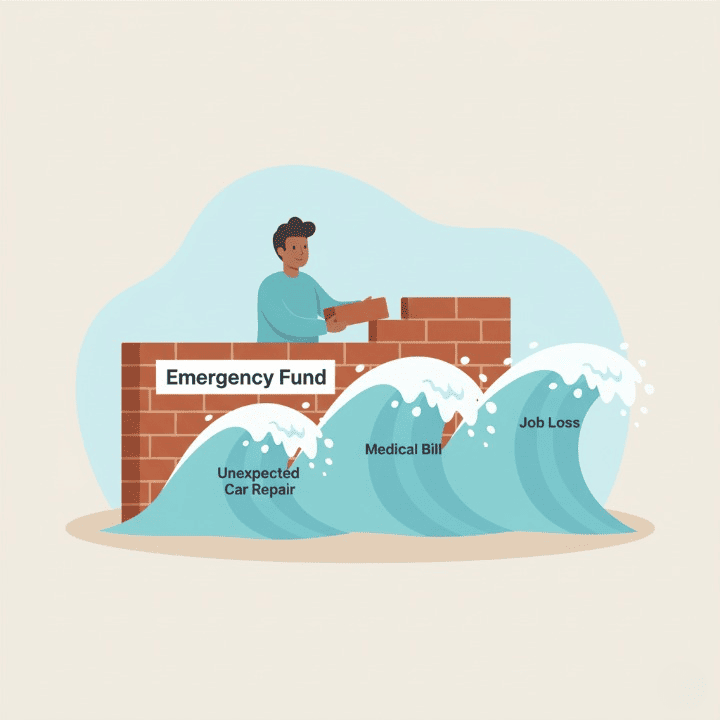

Building an emergency fund is the ultimate act of financial self-care. It is the cornerstone of a solid financial house and the tool that empowers you to handle life’s inevitable surprises with confidence instead of fear. This fund is your shield against high-interest rate credit card debt, your guardian for your hard-earned credit score, and a powerful reliever of financial stress, which directly benefits your overall health. It works in harmony with your formal insurance policies to create a comprehensive safety net. Start small, be consistent, and know that every single dollar you save is another brick in the wall that protects your financial future.