Introduction

Life is full of surprises, right? Some are great, like a surprise promotion or finding a twenty-dollar bill in an old jacket. Others? Not so much. Imagine this: your car gets into a fender bender, you have an unexpected medical emergency, or a pipe bursts in your apartment. Without a safety net, these “surprises” can quickly turn into massive financial headaches, emptying your savings or even landing you in debt.

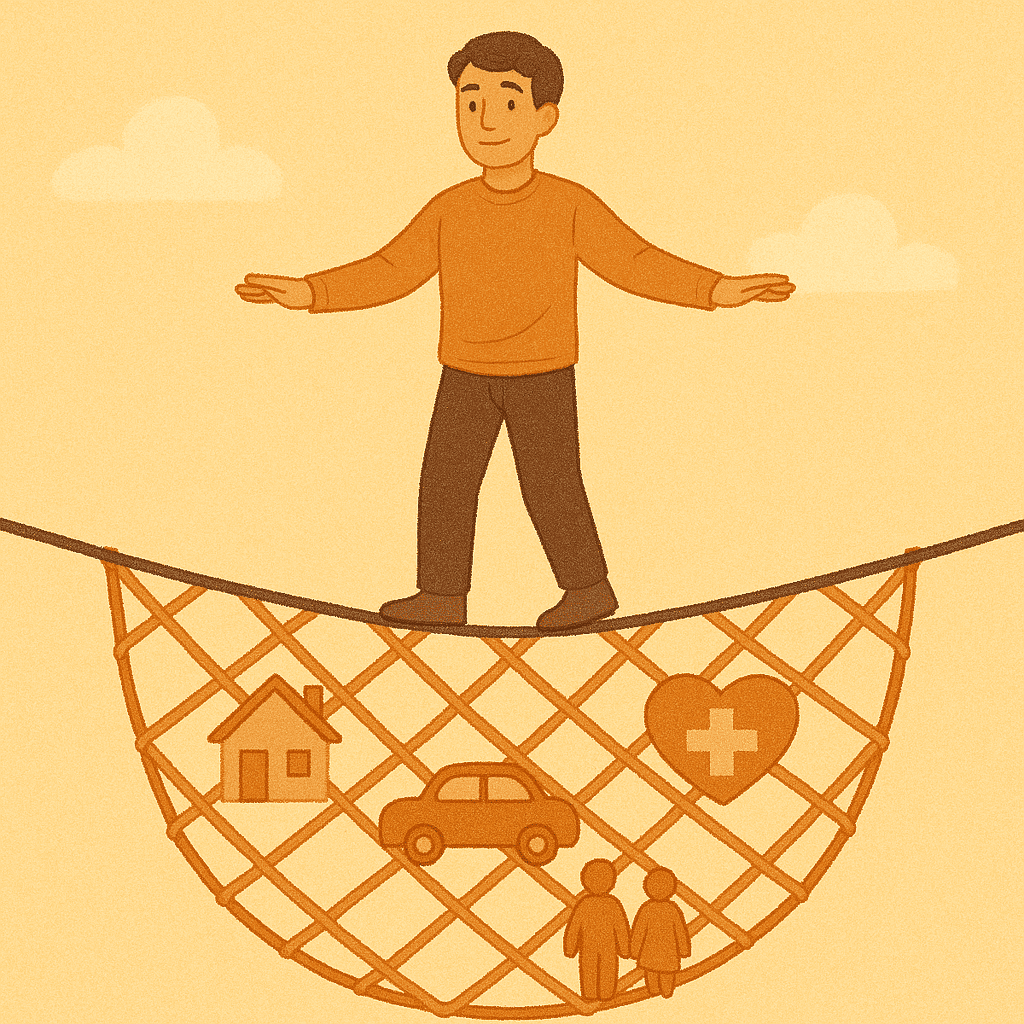

That’s where insurance comes in. For many, insurance feels like a confusing, jargon-filled topic, something you have to buy but don’t quite understand. But here’s the secret: insurance isn’t just another bill. It’s one of the most powerful tools in your personal finance toolkit, designed to protect you from the unexpected and provide invaluable peace of mind. Let’s break it down in plain language.

What is Insurance, Anyway? Your Shared Umbrella

Think of insurance like a shared umbrella. A lot of people (policyholders) chip in a little bit of money regularly (called premiums). This money goes into a big pot. If one person under the “umbrella” experiences a covered event—like their car being damaged or falling ill—they can get money from that big pot to help cover the costs.

Essentially, insurance is a contract where you pay a company a regular amount, and in return, they promise to pay you a larger sum or cover specific costs if certain unfortunate events happen. It’s all about spreading risk. Instead of one person bearing the full financial burden of a disaster, many people contribute to a fund that helps those who need it most. This makes major financial shocks manageable for individuals.

Why Do You Even Need Insurance? Protecting What Matters

You might be thinking, “Why pay for something I hope I never use?” That’s a valid question! The answer lies in financial protection and stability. Without insurance, a single major incident could:

- Wipe out your savings: A serious car accident or a major illness could lead to bills costing tens of thousands, or even hundreds of thousands, of dollars. Your emergency fund might cover a few months of living expenses, but rarely these kinds of catastrophic costs.

- Force you into debt: If you don’t have savings to cover an unexpected event, you might have to take out high-interest loans, pushing you further behind financially.

- Jeopardize your assets: If you’re liable for an accident, your personal assets (like your home or investments) could be at risk.

- Cause immense stress: The emotional toll of a major financial hit, on top of dealing with an unfortunate event, can be overwhelming.

Insurance acts as a buffer, ensuring that your financial journey isn’t derailed by life’s inevitable bumps. It allows you to rebuild and recover without sacrificing your long-term financial goals.

Common Types of Insurance You Should Know About

While there are many specialized types of insurance, a few are fundamental for most people. Understanding these is a great starting point:

1. Health Insurance

This is arguably one of the most critical types of insurance. Medical emergencies and ongoing healthcare costs can be astronomically expensive. Health insurance helps cover things like doctor visits, prescriptions, hospital stays, and preventive care. Even a minor injury or illness can result in significant bills, making health insurance a non-negotiable for protecting your finances and ensuring you can get the care you need.

2. Auto Insurance

If you own a car, you likely know this one well – it’s legally required in most places! Auto insurance protects you financially in case of an accident, theft, or other damage to your vehicle or someone else’s. It can cover repairs, medical expenses for injuries, and liability if you’re at fault in an accident.

3. Homeowners or Renters Insurance

Whether you own your home or rent an apartment, your dwelling and its contents are valuable. Homeowners insurance protects your house and belongings from perils like fire, theft, and natural disasters, and also provides liability coverage if someone is injured on your property. If you rent, renters insurance is your equivalent, covering your personal belongings and liability, often at a very affordable price.

4. Life Insurance

This type of insurance might feel a bit morbid, but it’s crucial if you have people who depend on you financially (like children, a spouse, or even elderly parents). Life insurance provides a financial payout to your beneficiaries if you pass away. This money can help them cover living expenses, pay off debts, or fund future needs, ensuring your loved ones are financially stable even if you’re no longer there.

Key Terms to Understand (No Jargon Overload!)

Don’t let these terms intimidate you; they’re simpler than they sound!

- Premium: This is the regular payment you make to the insurance company to keep your policy active. It could be monthly, quarterly, or annually.

- Deductible: This is the amount of money you have to pay out-of-pocket before your insurance coverage kicks in. For example, if you have a $500 deductible on your car insurance and you have a $2,000 repair bill, you’d pay the first $500, and your insurance would cover the remaining $1,500.

- Coverage: This refers to what your insurance policy actually pays for. Policies have limits on how much they will pay for different types of claims.

- Claim: This is the formal request you make to your insurance company for payment or services when a covered event occurs.

How to Choose the Right Insurance for You (Actionable Tips)

Choosing insurance doesn’t have to be overwhelming. Here are some actionable steps to guide you:

- Assess Your Needs: What do you need to protect? Do you have dependents? Do you own a car or a home? Think about your lifestyle and potential risks. For example, if you’re single with no dependents, life insurance might not be an immediate priority, but health insurance definitely is!

- Shop Around and Compare Quotes: Don’t just go with the first offer you receive. Different companies offer different rates and coverage options. Use online comparison tools or work with an independent insurance agent to get multiple quotes.

- Read the Fine Print (Seriously!): We know it’s boring, but understanding what your policy covers—and, more importantly, what it doesn’t cover—is crucial. Pay attention to exclusions, deductibles, and coverage limits. If you have questions, ask your agent!

- Review Your Policies Regularly: Life changes. You might get married, have children, buy a house, or change jobs. These life events can significantly impact your insurance needs. Make it a habit to review your policies once a year to ensure they still meet your current situation.

Conclusion

Insurance isn’t a luxury; it’s a fundamental part of a healthy financial plan. It protects your hard-earned money and provides a critical safety net against life’s unpredictable moments. While it might seem like an expense, think of it as an investment in your financial security and your peace of mind.

Don’t wait for a crisis to understand your options. Take control today! Start by reviewing any current policies you have or researching the types of insurance you might need. Understanding your options is the first step toward building a resilient financial future. What kind of insurance are you most curious about? Share your thoughts in the comments below!