Maximizing Your Health Savings Account (HSA) is a powerful strategy for astute investors seeking to leverage unparalleled financial advantages. Many people view an HSA merely as a savings vehicle for medical expenses; however, its true potential extends far beyond, offering a unique triple tax benefit that few other investment tools can match. Understanding and utilizing these benefits can significantly impact your long-term financial health and retirement planning. Therefore, a deeper dive into its mechanics reveals why an HSA is often hailed as one of the most advantageous accounts available today.

Understanding the Power of an HSA: The Triple Tax Advantage

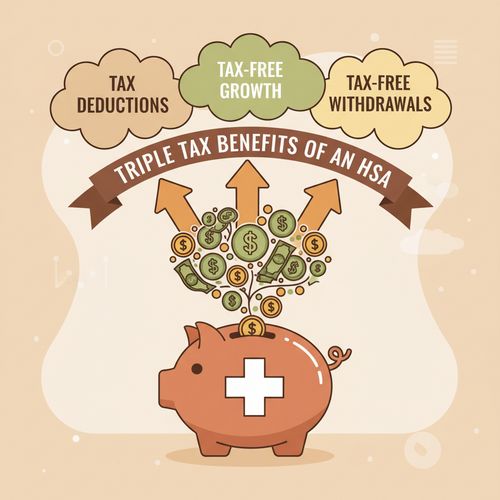

The core appeal of a Health Savings Account lies in its remarkable triple tax benefits. This distinctive feature sets HSAs apart from most other investment and savings accounts. Consequently, grasping these three pillars is crucial for any investor looking to optimize their financial strategy. This strategic advantage offers a unique pathway to accumulate wealth while simultaneously covering healthcare costs.

Tax-Deductible Contributions

Firstly, contributions to your HSA are tax-deductible. This means that any money you contribute reduces your taxable income for the year. For instance, if you contribute $3,000 to your HSA, your taxable income decreases by $3,000. This immediate tax break can lead to substantial savings on your annual tax bill. Many employers offer the convenience of pre-tax payroll deductions, making contributions even more efficient. Opting for this method allows you to contribute directly from your gross pay, which further simplifies your tax filing process and boosts your take-home pay.

Tax-Free Growth

Secondly, the funds within your HSA grow tax-free. This particular benefit is incredibly powerful, especially over the long term. Any interest, dividends, or capital gains generated by the investments held in your HSA are not subject to taxes. This allows your money to compound more aggressively without the drag of annual taxation. Contrast this with a standard brokerage account, where investment gains are typically taxed each year. Furthermore, this tax-free growth accelerates your wealth accumulation, making your HSA a formidable investment tool. You can find more information about tax advantages on official government resources like the IRS website.

Tax-Free Withdrawals for Qualified Medical Expenses

Thirdly, and perhaps most enticingly, withdrawals from your HSA are entirely tax-free, provided they are used for qualified medical expenses. This includes a wide range of services, from doctor visits and prescription medications to dental and vision care. Essentially, you contribute pre-tax dollars, those dollars grow tax-free, and you withdraw them tax-free for healthcare needs. This creates an incredibly efficient cycle for managing healthcare costs both now and in retirement. Understanding what constitutes a qualified medical expense is vital; consult Healthcare.gov for detailed lists. Furthermore, this benefit effectively means that your healthcare costs are paid with dollars that have never been taxed, offering a significant financial advantage.

Eligibility and Contribution Limits: Getting Started with Your HSA

While the benefits of an HSA are clear, not everyone is eligible to open or contribute to one. Specific criteria must be met to take advantage of this powerful financial tool. Moreover, understanding the annual contribution limits is crucial for maximizing your savings without incurring penalties.

Who Qualifies for an HSA?

To be eligible for an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP). This is the foundational requirement. An HDHP is a health insurance plan with higher annual deductibles than traditional plans. However, it often comes with lower monthly premiums. Additionally, you cannot have any other health coverage (with certain exceptions, such as specific dental, vision, or disability coverage). You must also not be enrolled in Medicare. Lastly, you cannot be claimed as a dependent on someone else’s tax return. Meeting these criteria unlocks the door to HSA eligibility, providing access to its unique tax advantages.

Annual Contribution Limits

The IRS sets annual limits on how much you can contribute to your HSA. These limits are updated yearly and vary depending on whether you have individual or family HDHP coverage. For instance, in 2024, the individual contribution limit is $4,150, while the family limit stands at $8,300. It is important to note that these figures include any contributions made by your employer. Moreover, individuals aged 55 and older can make an additional “catch-up” contribution of $1,000 per year. Staying within these limits is paramount to avoid tax penalties. Consequently, carefully tracking your contributions throughout the year is essential.

Beyond Healthcare: HSA as a Retirement Investment Vehicle

While designed for health savings, the HSA’s triple tax benefits make it an exceptional retirement investment vehicle. For many, it surpasses even 401(k)s and IRAs in flexibility and tax efficiency. Therefore, strategically viewing your HSA as a long-term investment account can unlock its full potential. This perspective transforms it from a simple savings tool into a powerful wealth-building asset.

The Power of Investing Your HSA

Many HSA providers allow you to invest funds once your account balance reaches a certain threshold. This is where the “tax-free growth” benefit truly shines. Instead of letting your money sit in a low-interest savings account, you can invest it in a variety of options, including mutual funds, ETFs, and stocks. Over decades, these investments can generate significant returns, all growing tax-free. This compounding effect, unhindered by annual taxes, can lead to a substantial nest egg. Remarkably, this makes your HSA a stealthy but potent retirement account. Investors should consider the long-term implications of this growth.

Strategic Withdrawal Considerations in Retirement

Once you reach age 65, your HSA gains even more flexibility. At this point, you can withdraw funds for any purpose without incurring a 20% penalty, though non-qualified withdrawals will be subject to ordinary income tax. This effectively means your HSA functions much like a traditional IRA or 401(k) in retirement, but with the added bonus of being entirely tax-free if used for qualified medical expenses. Considering healthcare costs typically increase in retirement, an HSA provides a dedicated, tax-advantaged fund for these inevitable expenses. Consequently, it offers peace of mind and financial security. Keeping meticulous records of all qualified medical expenses throughout your working life allows you to reimburse yourself tax-free later in retirement, even if you paid out-of-pocket at the time. This strategy, detailed by financial experts, maximizes the tax-free withdrawal potential, as explored by sources like Investopedia.

Maximizing Your HSA: Advanced Strategies and Best Practices

To truly unlock the full potential of your HSA, employing advanced strategies and adhering to best practices is essential. These approaches go beyond basic contributions, aiming to optimize the account for long-term growth and flexibility. Consequently, a proactive approach to managing your HSA can yield significant financial rewards.

Paying Out-of-Pocket and Reimbursing Later

One of the most powerful HSA strategies is to pay for current medical expenses out-of-pocket, if you can afford to do so, and then save your receipts. You can later reimburse yourself from your HSA for these qualified expenses at any point in the future. This strategy allows your HSA funds to remain invested and continue growing tax-free for a longer period. Imagine accumulating years of receipts for medical costs. You can then withdraw a lump sum tax-free from your HSA years, or even decades, later. This essentially turns your HSA into an emergency fund for future health needs while simultaneously serving as a powerful investment vehicle. Furthermore, this method keeps your money working for you for as long as possible.

Funding Your HSA to the Maximum

Consistently contributing the maximum allowable amount each year is fundamental to maximizing your HSA benefits. This ensures you take full advantage of the tax deductions and the subsequent tax-free growth potential. Many employers offer contributions to employee HSAs as part of their benefits package. Therefore, leveraging any employer contributions effectively boosts your savings without impacting your take-home pay. Prioritizing HSA contributions, perhaps even before other retirement accounts if your employer doesn’t offer a 401(k) match, can be a wise financial move. This proactive approach accelerates your path to financial independence. Notably, this dedication to maximum funding significantly amplifies its long-term impact.

Considering Your Health Needs and Risk Tolerance

When deciding how much to invest within your HSA and what types of investments to choose, consider your current and projected health needs alongside your personal risk tolerance. If you anticipate significant near-term medical expenses, maintaining a portion of your HSA in easily accessible, less volatile investments might be prudent. Conversely, if you are relatively healthy and have other emergency savings, you might opt for more aggressive growth investments. Balancing these factors ensures your HSA serves both your immediate and long-term financial goals. Thus, a personalized approach to investment strategy within your HSA is highly recommended. This thoughtful consideration helps in managing both health and wealth effectively.

Common HSA Pitfalls to Avoid

While an HSA offers incredible advantages, certain missteps can diminish its effectiveness or even lead to penalties. Being aware of these common pitfalls helps you navigate your HSA journey successfully. Avoiding these mistakes ensures you fully capitalize on its benefits. Therefore, understanding potential traps is as important as knowing the benefits.

Misunderstanding Qualified Medical Expenses

A frequent error involves withdrawing funds for non-qualified expenses before age 65. If you do this, those withdrawals become taxable income and are subject to a 20% penalty. This penalty can significantly erode your savings. Always ensure your withdrawals align with the IRS definition of qualified medical expenses to avoid these costly consequences. Consequently, retaining all receipts and documentation for medical expenses is paramount. Consulting an expert or checking the IRS guidelines regularly can prevent costly errors.

Not Investing Your HSA Funds

Perhaps the biggest missed opportunity is simply letting HSA funds sit in a standard savings account. While safe, this approach forfeits the powerful tax-free growth potential. For long-term investors, the investment component is where the true wealth-building power of the HSA lies. Neglecting to invest means you are leaving significant money on the table. Moreover, actively investing these funds allows them to compound over decades. Take the time to research investment options offered by your HSA provider and choose those that align with your financial goals and risk tolerance. Many individuals miss this crucial step, thereby limiting their account’s potential.

Missing Out on Catch-Up Contributions

Individuals aged 55 and older are eligible for an additional $1,000 “catch-up” contribution annually. Overlooking this benefit means missing a valuable opportunity to boost your retirement healthcare savings. If you qualify, make every effort to contribute this extra amount each year. This extra contribution can significantly enhance your HSA balance as you approach retirement. Therefore, actively taking advantage of this provision is a smart financial move. It directly supports your long-term financial health. The additional funds provide a robust cushion against future medical costs.

Conclusion

Maximizing Your Health Savings Account (HSA) stands out as an exceptionally versatile and powerful financial instrument, particularly for those looking to optimize their tax strategy and secure their financial future. Its triple tax benefits—tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses—offer an unparalleled advantage. By understanding eligibility, adhering to contribution limits, and employing strategic investment approaches, you can transform your HSA from a mere health savings account into a robust component of your overall wealth management and retirement planning strategy. Taking a proactive approach to your HSA can significantly enhance your financial well-being, providing a dedicated and efficient way to manage healthcare costs while simultaneously building substantial wealth for the long term. This account truly serves as a cornerstone for a sound financial future. Ensure you are fully leveraging all its potential benefits to achieve your financial goals. Moreover, a well-managed HSA offers flexibility and security as you navigate both immediate health needs and future retirement plans.