Introduction

A credit card can often feel like a double-edged sword. When someone uses it irresponsibly, it can quickly lead to a cycle of debt and financial stress. However, when a person uses it with a clear and responsible strategy, it becomes the single most powerful and accessible tool for building a strong credit history. And in the modern financial world, a good credit score is absolutely essential.

A strong score is your key to unlocking your biggest life goals, from buying a car to owning a home. This guide will provide you with a clear, step-by-step plan. We will not focus on rewards or perks. Instead, we will show you exactly how to use a basic credit card to build an excellent credit score from the ground up. This is a foundational skill for your long-term financial success.

Why Your Credit Score Matters So Much

Before we get into the “how,” let’s briefly revisit “why” this is so important. Your credit score is much more than just a three-digit number. It is a powerful indicator of your financial health and responsibility.

First and foremost, a good credit score makes it possible to get approved for major financing. This includes the mortgage you will need for a home or the auto loan for a car.

Second, a higher score will qualify you for a much lower interest rate on that financing. This simple fact can save you thousands, or even tens of thousands, of dollars over the life of a loan. A good score means borrowing money is cheaper for you.

Furthermore, the influence of your credit extends beyond just loans. Landlords often check your credit when you apply to rent an apartment. Some insurance companies may even use a credit-based score to help determine your premiums for auto insurance. In short, building good credit is a vital part of your overall financial management.

The Two Golden Rules of Building Credit

The entire strategy of building good credit with a credit card simplifies into two non-negotiable rules. If you follow these two rules consistently, you will be on the path to an excellent score.

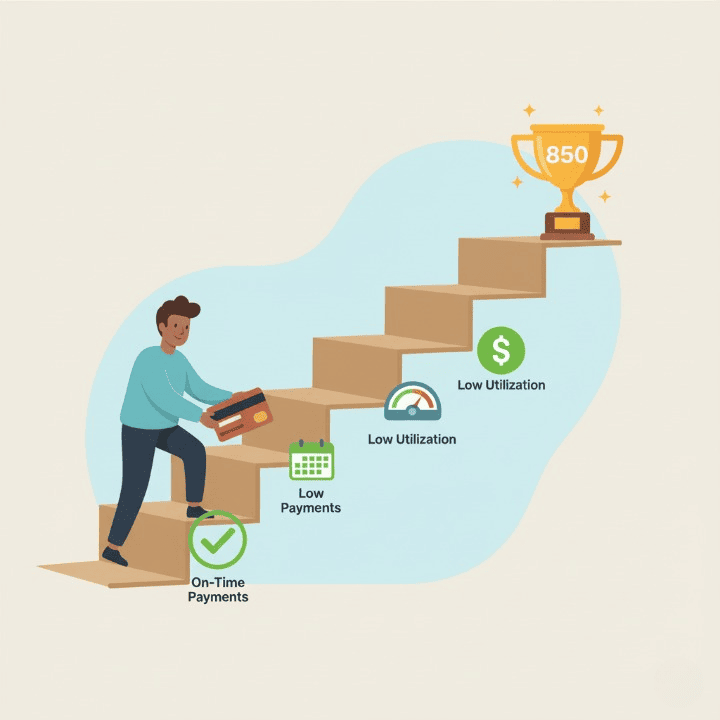

Golden Rule #1: Pay Your Bill On Time, Every Time

This is the most important rule. Your payment history is the single largest factor that makes up your credit score. In fact, it accounts for about 35% of your score in most models. Lenders want to see a long and consistent track record of you paying your bills as agreed.

A single late payment that a creditor reports to the credit bureaus can have a significant negative impact on your score. Unfortunately, it can stay on your credit report for years. Therefore, you must make it your absolute top priority to never miss a payment due date. The best way to ensure this is to set up automatic payments for at least the minimum amount due. This simple action acts as a safety net to protect your payment history.

Golden Rule #2: Keep Your Balances Low

The second most important rule is to keep your balances low in relation to your credit limit. This concept is known as your credit utilization ratio. It accounts for about 30% of your score.

For example, if you have one credit card with a $5,000 limit and you have a $500 balance on it, your utilization ratio is 10%. Financial experts generally recommend that you always keep this ratio below 30%. However, for the best possible score, you should aim to keep it below 10%. A high utilization ratio signals to lenders that you may be over-reliant on debt. They see this behavior as risky.

A Step-by-Step Strategy for Beginners

Now, let’s put these rules into a practical, step-by-step plan for someone who is just starting to build their credit.

Step 1: Get the Right Type of Card. If you have no credit history at all, you might need to start with a specific type of credit card. A “secured” credit card is often the best option. This type of card requires a small cash deposit that acts as your credit limit. Another option could be a student credit card if you are enrolled in college.

Step 2: Use the Card for a Small, Planned Purchase. Once you have your card, you should not use it for your everyday spending. Instead, you can use it for one small, recurring purchase that you already have in your budget. For example, you could use it to pay for a single streaming service subscription. Another option is to use it for your monthly cell phone bill. This action shows that the card is active and being used.

Step 3: Pay the Statement Balance in Full. After you have made your one small purchase for the month, you should wait for your monthly statement to be generated. This is important, as it ensures the activity is reported to the credit bureaus. Then, as soon as you receive the statement, you must pay the entire balance in full before the due date. This single action accomplishes three things at once. You will have an on-time payment. You will have a very low credit utilization ratio. And, you will never pay a single cent of interest.

Step 4: Be Patient and Consistent. Finally, you must be patient. Building a great credit score is a marathon, not a sprint. It takes time to build up a positive history. You should repeat this simple process every single month. After about six months of consistent, positive history, you should start to see a significant improvement in your credit score.

Common Mistakes to Avoid When Building Credit

As you follow this plan, you should also be aware of a few common mistakes that can set you back.

Mistake #1: Closing Your Oldest Credit Account. The length of your credit history makes up 15% of your score. Because of this, you should generally avoid closing your oldest credit card account, even if you get a new one. Keeping it open helps to preserve the average age of your credit history.

Mistake #2: Applying for Too Much Credit at Once. Every time you apply for a new line of credit, it can result in a “hard inquiry” on your report. Too many of these in a short period can temporarily lower your score. Therefore, you should only apply for new credit when you truly need it.

Mistake #3: Carrying a Balance to “Show Activity.” This is a very common and costly myth. You do not need to carry a balance from month to month and pay a high interest rate to build credit. Paying your bill in full every month is the best and most responsible strategy.

Conclusion

In conclusion, a credit card is an exceptional tool. It is one of the best ways to build a positive financial history, but only when it is used with a clear and disciplined strategy.

The plan is simple but powerful. You can use your card for a small, planned purchase each month. You must then pay your bill on time and in full. You should also focus on keeping your overall balances low.

By following these simple rules, you are in complete control of your credit score. You are not just building a number. You are building a powerful asset. This asset will help you unlock your future financial goals. It will also serve as a cornerstone for your long-term financial health.