Executive Summary

- Catastrophe bonds offer an innovative mechanism for transferring specific perils from insurers to capital markets. They represent a critical component of sophisticated risk management frameworks.

- Structuring these complex instruments involves meticulous trigger design, robust actuarial modeling, and compliance with intricate regulatory mandates. This ensures effective risk disintermediation.

- Dynamic reinsurance protocols complement Cat bond strategies. They enable agile portfolio adjustments and real-time risk mitigation in volatile market environments.

The Evolution of Insurance-Linked Securities in Risk Transfer

Traditional reinsurance markets have historically absorbed peak peril exposures. However, their capacity can sometimes be constrained. The emergence of Insurance-Linked Securities (ILS) diversified this risk transfer landscape. ILS provides insurers with direct access to global capital markets. This significantly expands available risk capital.

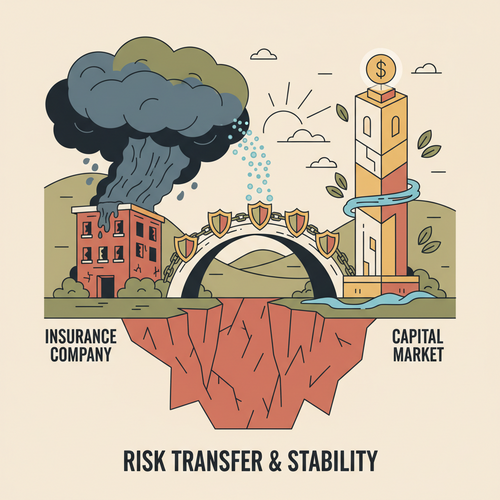

Catastrophe bonds, a prominent form of ILS, allow sponsors to offload specific perils. These include hurricanes, earthquakes, and other natural disasters. Capital markets investors gain exposure to uncorrelated returns. This offers portfolio diversification benefits, distinct from traditional financial assets. Such instruments represent a paradigm shift in managing systemic risk.

Fundamental Principles of Catastrophe Bond Structuring

Catastrophe bond structuring begins with a sponsoring insurer or reinsurer. The sponsor transfers defined risks to a Special Purpose Vehicle (SPV). This SPV is typically domiciled in a financially robust jurisdiction. The SPV then issues bonds to capital market investors. These bonds are collateralized by the premium payments received from the sponsor. Special Purpose Vehicles (SPVs) ensure legal separation of assets.

Investor principal is held in a trust account. This collateral is often invested in highly liquid, low-risk securities. If a predefined catastrophic event occurs, the SPV may retain some or all of the principal. This principal is then paid to the sponsor to cover their losses. If no event occurs, investors receive their principal back at maturity. They also earn attractive coupon payments throughout the bond’s term.

Dissecting Cat Bond Trigger Mechanisms

The efficacy of a catastrophe bond hinges on its trigger mechanism. Each type presents unique characteristics and risk profiles. Parametric triggers are based on objectively measurable physical parameters. Examples include earthquake magnitude or hurricane wind speed at specific locations. These offer speed and transparency but introduce basis risk.

Indemnity triggers are directly tied to the sponsor’s actual incurred losses from a defined event. They minimize basis risk for the sponsor. However, they require extensive loss verification. Industry loss triggers are activated when aggregated industry losses exceed a threshold. These are calculated by independent third-party agencies. Finally, modeled loss triggers rely on outputs from specific catastrophe models. Selecting the appropriate trigger is paramount for effective risk transfer. Each choice impacts pricing and investor appetite.

The Role of Actuarial Science and Risk Modeling

Robust actuarial science forms the bedrock of Cat bond pricing and structuring. Actuaries meticulously assess the probability of loss events. They employ sophisticated stochastic modeling techniques. This determines the Probability of Attachment (PoA) and Expected Loss (EL) for each tranche. Catastrophe modeling firms, such as AIR Worldwide, RMS, and Verisk (formerly EQECAT), provide critical data. Their models simulate millions of potential events. This quantifies potential losses across various perils.

These models integrate vast datasets on geographical exposure, building codes, and historical event characteristics. Underwriters leverage these insights for investor due diligence. They ensure the bond’s risk-adjusted return aligns with market expectations. Precise risk quantification minimizes uncertainty. It supports confident investor participation in the ILS market. This analytical rigor is non-negotiable.

Dynamic Reinsurance Protocol Execution in Practice

Dynamic reinsurance protocols represent an adaptive approach to risk management. Unlike static, annually renewed contracts, these protocols are fluid. They allow insurers to adjust coverage levels and structures in response to real-time market shifts. This agility is crucial in an increasingly volatile global landscape. Integrating Cat bonds with dynamic protocols optimizes capital allocation. It ensures efficient deployment of risk capital.

These protocols leverage advanced data analytics and predictive modeling. This enables rapid decisions on retrocession purchases or bond issuances. Sponsors can fine-tune their exposure management strategies. They can respond to emerging threats or favorable pricing conditions. This proactive stance significantly enhances an insurer’s financial resilience. It moves beyond traditional, rigid frameworks.

“In analyzing recent market shifts, we observe a clear trend toward adaptive risk transfer mechanisms. Dynamic reinsurance, particularly when integrated with bespoke Cat bond tranches, offers unparalleled flexibility in optimizing capital at risk.”

Mitigating Market Volatility and Basis Risk through Protocol Agility

Market volatility poses significant challenges for long-term risk management. Dynamic reinsurance protocols directly address this by fostering agility. They enable timely adjustments to an insurer’s reinsurance program. This can involve scaling up or down coverage based on updated risk assessments. Catastrophe bonds themselves provide a stable multi-year layer of protection. Combining them with dynamic protocols creates a highly responsive framework.

Basis risk, the mismatch between the trigger event and actual losses, remains a key concern. Diversifying Cat bond triggers across parametric, indemnity, and industry loss types can mitigate this. Dynamic protocols further allow sponsors to re-evaluate their trigger portfolio. This happens in light of evolving peril landscapes. Enhanced portfolio optimization reduces unexpected financial exposures. It increases the predictability of risk transfer outcomes.

Regulatory Compliance and Investor Due Diligence

The structured finance nature of Cat bonds necessitates stringent regulatory compliance. Jurisdictions like Ireland, Bermuda, and the Cayman Islands have well-established frameworks. These facilitate SPV formation and bond issuance. Regulatory bodies scrutinize offering documents for transparency and disclosure. Solvency II directives, for example, heavily influence European sponsors’ capital requirements. They impact how Cat bonds are recognized for capital relief.

Rating agencies (S&P, Moody’s, Fitch) play a crucial role. They assign ratings based on the bond’s risk profile and collateral quality. This informs investor due diligence. Investors conduct their own independent analyses. They assess the underlying perils, trigger mechanisms, and creditworthiness of the collateral. Thorough regulatory oversight ensures market integrity. It fosters investor confidence in these complex instruments.

Strategic Integration: Cat Bonds within a Holistic Risk Management Framework

Integrating catastrophe bonds into a broader enterprise risk management (ERM) framework is strategic. It moves beyond merely purchasing capacity. Sponsors leverage ILS to optimize their entire capital structure. This involves a thoughtful balance between traditional reinsurance and capital markets solutions. Tailoring risk transfer solutions to specific, high-severity perils is crucial. It ensures cost-effective protection.

From an operational standpoint, this integration requires robust internal capabilities. These include advanced risk modeling, actuarial expertise, and capital markets acumen. The long-term stability offered by multi-year Cat bonds complements short-term traditional placements. This holistic approach enhances financial resilience. It allows insurers to manage extreme events effectively. The future of risk transfer is undoubtedly integrated and adaptive.

Conclusion

Catastrophe bond structuring remains a sophisticated financial discipline. It necessitates deep expertise in actuarial science and capital markets. Dynamic reinsurance protocols offer an agile complement. They enhance resilience against evolving global perils. Investors gain diversified uncorrelated returns. Sponsors achieve robust balance sheet protection. The convergence of these strategies optimizes risk transfer efficiency.

Are your current risk transfer mechanisms sufficiently agile to navigate emergent catastrophic exposures?