Introduction

Imagine spending years carefully building a house. You lay a strong foundation, construct sturdy walls, and fill it with things you value. Now, imagine leaving that house unprotected from storms, fires, or theft. In personal finance, your savings, investments, and financial goals are that house. Insurance is the essential roof and walls that protect it. Life is inherently unpredictable, and a single unexpected event—a car accident, a sudden illness, or damage to your home—can have devastating financial consequences. This is where insurance plays its most critical role. It is the bedrock of any sound financial plan. This guide will serve as a beginner’s introduction to the world of insurance, explaining how it works and how the right policies protect not only your belongings but also your long-term financial well-being, your credit, and your overall health.

What Is Insurance? The Principle of Shared Risk

At its core, the concept of insurance is quite simple: it is a tool for transferring risk. You pay a small, predictable fee—called a premium—to an insurance company. In exchange for your regular payments, the company agrees to take on the financial risk of a large, unexpected loss. If a covered event occurs, you file a claim, and the company provides a financial payout to help you recover.

Think of it like a large community fund. Hundreds or thousands of people contribute a little bit of money to a central pot. While it’s unlikely that everyone will face an emergency at the same time, when one person does, the money in the pot is available to help them. The insurance company manages this pot, calculates the risks, and ensures the funds are there when needed.

To understand any policy, you need to know a few key terms:

- Premium: The fixed amount you pay (usually monthly or annually) to keep your insurance policy active.

- Deductible: The amount of money you must pay out-of-pocket for a covered loss before your insurance company starts to pay.

- Coverage: This defines what types of risks and losses the policy will pay for.

- Claim: A formal request you make to the insurance company for payment after a covered event.

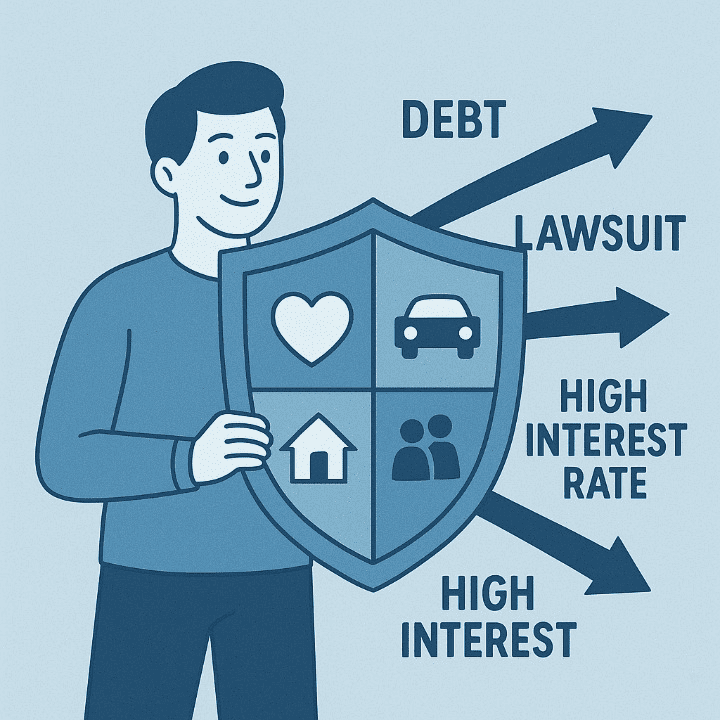

The Four Pillars of Personal Insurance

While there are many types of insurance, most personal financial plans are built on four key pillars. Each one protects a different, vital area of your life.

1. Health Insurance

As we’ve explored before, health insurance is arguably the most important type of insurance for an individual. It is the primary shield for both your physical and financial health. The cost of medical care can be astronomical, and a single serious illness or injury can lead to bills totaling tens or even hundreds of thousands of dollars. Health insurance makes these costs manageable, protecting your savings and preventing medical issues from escalating into a debt crisis.

2. Auto Insurance

For anyone who owns a vehicle, auto insurance is a necessity, and in most places, it is required by law. Its primary function is to protect you from the immense financial liability that can result from a car accident. If you are at fault in an accident that causes injury or property damage, the costs can be enormous. Liability coverage helps pay for those expenses. Other coverages, like collision and comprehensive, help pay for repairs to your own vehicle, whether from an accident, theft, or a natural event like a hail storm.

3. Homeowners or Renters Insurance

Your home is likely your most significant asset, and homeowners insurance protects that investment. It covers damage to the structure of your home and your personal belongings from events like fires, storms, or theft. It also includes liability coverage in case someone is injured on your property. Many renters mistakenly believe they are covered by their landlord’s policy, but that insurance only covers the building itself. Renters insurance is an affordable and essential policy that protects your personal possessions—furniture, electronics, clothing—and provides liability protection.

4. Life Insurance

Life insurance is a topic many people avoid, but it is a critical tool for anyone who has dependents (such as a spouse or children). Its purpose is to provide a financial safety net for your loved ones if you were to pass away. The payout can be used to replace your lost income, pay off a mortgage, cover funeral expenses, or fund a child’s education. For most people, an affordable “term life” policy, which provides coverage for a specific period (e.g., 20 or 30 years), is an excellent way to ensure your family’s financial stability.

The Financial Domino Effect of Being Underinsured

Understanding the importance of insurance becomes clearer when you consider what happens without it. An uninsured loss can trigger a chain reaction of negative financial events.

Let’s imagine a scenario with Maria, who rents an apartment but decided to skip getting renters insurance to save a little money. A fire in her building destroys most of her belongings, causing a $10,000 loss.

- The Immediate Need: Maria has to replace her clothes, furniture, and computer immediately. She drains her small emergency fund, but it’s not enough.

- The Turn to Debt: She is forced to seek financing. She uses her credit card for some purchases and takes out a personal loan for the rest. Both come with a high interest rate.

- The Financial Strain: The new loan and credit card payments put a major strain on her monthly budget. She struggles to keep up.

- The Damaged Credit: After a few months, she misses a payment, which is reported to the credit bureaus. Her credit score drops significantly.

In this example, a single uninsured event led directly to high-interest debt and long-term damage to her credit. This is how insurance acts as a firewall, preventing one bad event from burning down your entire financial house.

How Insurance and Credit Influence Each Other

The relationship between insurance and credit is a two-way street. As we saw with Maria, a lack of insurance can force you into debt that damages your credit score. If a major liability, like a car accident lawsuit, leads to bankruptcy, the impact on your credit can be devastating and last for many years.

Conversely, your credit history can influence how much you pay for insurance. In many regions, insurance companies use a credit-based insurance score when setting premiums for auto and homeowners policies. The data shows that people who manage their credit responsibly tend to file fewer claims. As a result, maintaining a good credit score can often lead to lower insurance premiums, saving you money year after year.

Conclusion

Insurance should not be viewed as just another monthly bill. It is a fundamental and proactive investment in your financial security. It is the shield that stands between you and the unpredictable events of life. By creating a comprehensive safety net with the right combination of policies—health, auto, property, and life—you are doing more than just protecting your possessions. You are safeguarding your savings from being wiped out, protecting your credit score from the damage of unforeseen debt, and providing stability for yourself and your family. Taking the time to understand your needs and put the right coverage in place is one of the most powerful steps you can take toward achieving lasting financial peace of mind.