Introduction

Navigating the complexities of healthcare costs can feel overwhelming. Medical expenses, whether routine check-ups or unexpected emergencies, form a significant part of many household budgets. Thankfully, there are powerful financial tools available to help manage these costs and even provide substantial tax benefits. Two of the most popular options are the Flexible Spending Account (FSA) and the Health Savings Account (HSA).

Understanding the key differences between an FSA vs HSA is crucial for anyone looking to optimize their healthcare spending and boost their overall financial well-being. Both accounts offer distinct advantages. However, their eligibility requirements, features, and long-term implications vary significantly. This guide will break down each option, helping you make an informed decision for your financial future.

What is a Flexible Spending Account (FSA)?

A Flexible Spending Account (FSA) is an employer-sponsored benefit. It allows employees to set aside pre-tax money from their paychecks. This money is then used to pay for qualified out-of-pocket medical and dental expenses. FSAs offer a straightforward way to reduce your taxable income while covering healthcare costs.

How an FSA Works

- Employer-Sponsored: Your employer must offer an FSA plan for you to participate. You cannot open one independently.

- Pre-Tax Contributions: Funds are deducted from your gross pay before taxes are calculated. This reduces your taxable income, saving you money on federal income taxes, and often state and local taxes as well.

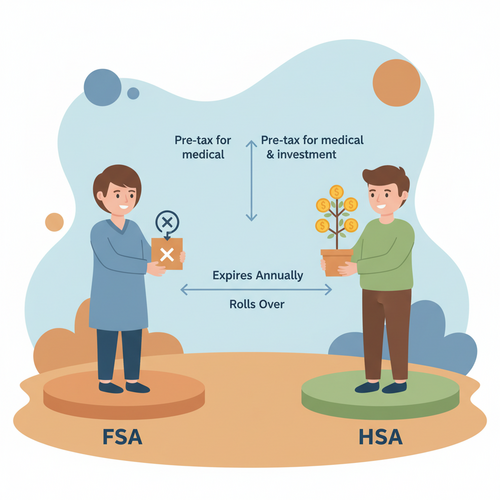

- “Use-It-or-Lose-It” Rule: Historically, FSAs were known for their strict “use-it-or-lose-it” rule. This meant any money not spent by the end of the plan year was forfeited. However, many plans now offer grace periods (typically up to 2.5 months) or allow a limited amount to be carried over to the next year. It is important to check your specific plan’s rules.

- Eligible Expenses: A wide range of medical, dental, and vision expenses are eligible. These include co-pays, deductibles, prescription medications, over-the-counter drugs with a doctor’s note (or without, in some cases after recent changes), and even vision care like glasses and contacts. For a comprehensive list, you can always refer to IRS Publication 502.

FSA Tax Advantages

The primary benefit of an FSA lies in its significant tax savings. These advantages make it a powerful tool for managing healthcare costs:

- Tax-Free Contributions: The money you contribute to an FSA is not subject to federal income tax, Social Security tax, or Medicare tax. This immediately reduces your taxable income.

- Tax-Free Withdrawals: When you use FSA funds for qualified medical expenses, the withdrawals are completely tax-free. You pay no taxes on the money you spend.

This “tax-free in, tax-free out” structure means you effectively pay for your medical expenses with pre-tax dollars, saving a substantial amount compared to using after-tax income.

What is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a tax-advantaged savings account specifically designed for individuals enrolled in a High-Deductible Health Plan (HDHP). Unlike FSAs, HSAs are owned by the individual, offering greater flexibility and long-term potential. They combine the benefits of a savings account with investment opportunities.

How an HSA Works

- Requires a High-Deductible Health Plan (HDHP): Eligibility for an HSA is tied to having an HDHP. An HDHP is a health insurance plan with a higher deductible than traditional plans, but typically lower monthly premiums. This link is non-negotiable for HSA eligibility. You can learn more about HDHPs on Healthcare.gov.

- Individual or Employer Contributions: Both you and your employer can contribute to your HSA. Contributions can be made by you directly or through payroll deductions, often on a pre-tax basis if done via payroll.

- No “Use-It-or-Lose-It” Rule: This is a key differentiator. Funds in an HSA roll over from year to year. They never expire, making it a powerful long-term savings vehicle.

- Investment Potential: Once your HSA reaches a certain balance (often a few thousand dollars), you can typically invest the funds. This allows your money to grow over time, similar to a retirement account. Many providers offer a range of investment options, from mutual funds to ETFs.

HSA Tax Advantages: The Triple Threat

HSAs are often lauded for their “triple tax advantage.” This makes them one of the most tax-efficient accounts available:

- Tax-Deductible Contributions: Contributions you make to an HSA are tax-deductible. This reduces your taxable income for the year you contribute.

- Tax-Free Growth: Any investment earnings within your HSA grow tax-free. You do not pay capital gains taxes or dividend taxes on these earnings as long as they remain in the account.

- Tax-Free Withdrawals: Qualified medical expenses can be paid for with tax-free withdrawals. This means you never pay taxes on the money you contribute, earn, or spend on healthcare.

When you reach age 65, you can withdraw HSA funds for any purpose without penalty. However, withdrawals for non-medical expenses will be taxed as ordinary income, similar to a traditional IRA or 401(k). For qualified medical expenses, withdrawals remain tax-free at any age.

Key Differences: FSA vs. HSA at a Glance

While both FSAs and HSAs help you save on healthcare costs, their fundamental structures and benefits are quite different. Understanding these distinctions is vital for choosing the right option.

Eligibility Requirements

- FSA: You must be employed by a company that offers an FSA as part of its benefits package. There are no specific health plan requirements.

- HSA: You must be enrolled in a High-Deductible Health Plan (HDHP). This is a strict requirement set by the IRS.

Portability and Rollover

- FSA: Generally, an FSA is tied to your employer. If you leave your job, you typically lose access to the funds. While some plans allow a limited rollover amount (e.g., $610 in 2024) or a grace period, the “use-it-or-lose-it” rule largely applies.

- HSA: An HSA is owned by the individual, not the employer. This means it is fully portable. The funds belong to you even if you change jobs or retire. All unused funds roll over from year to year indefinitely.

Investment Potential

- FSA: FSAs are spending accounts; they do not offer investment options. The money sits in a regular account, waiting to be spent.

- HSA: HSAs can be powerful investment tools. After meeting a minimum balance, you can invest your funds in various options. This allows your money to grow tax-free over the long term. Many people use HSAs as a supplemental retirement savings vehicle due to this feature.

Contribution Limits

The IRS sets annual contribution limits for both accounts, which are subject to change each year. It is crucial to stay updated on these figures.

- FSA: For 2024, the contribution limit for an FSA is $3,200 per employee.

- HSA: For 2024, the contribution limit for an individual is $4,150, and for a family plan, it is $8,300. Those aged 55 and older can contribute an additional “catch-up” contribution of $1,000.

Ownership

- FSA: The employer technically owns the FSA account. You have access to the funds as long as you are employed and the plan is active.

- HSA: The individual owns the HSA. This gives you complete control over the account, its funds, and its investment choices.

Choosing the Right Account for You

Deciding between an FSA and an HSA depends heavily on your individual health plan, financial situation, and healthcare needs. There is no one-size-fits-all answer.

When an FSA Might Be Better

An FSA can be an excellent choice under specific circumstances:

- Predictable Medical Expenses: If you know you will have regular, ongoing medical, dental, or vision expenses (e.g., prescriptions, therapy, braces), an FSA allows you to pay for these with pre-tax dollars.

- No HDHP: If your health insurance plan is not an HDHP, an FSA might be your only available option for pre-tax healthcare savings.

- Immediate Out-of-Pocket Costs: You can typically access the full elected FSA amount on the first day of your plan year, even if you haven’t contributed it all yet. This provides immediate funds for expenses.

Remember to carefully estimate your annual healthcare spending to avoid forfeiting funds at the end of the year.

When an HSA Shines

An HSA offers distinct advantages, especially for those looking at long-term financial planning:

- Have an HDHP: If you are already enrolled in an HDHP, an HSA is often the most financially savvy choice due to its triple tax benefits.

- Want Long-Term Savings and Investment Growth: For individuals who can cover their current medical expenses out-of-pocket and want to save for future healthcare costs (even in retirement), the investment growth potential of an HSA is unmatched.

- Desire Portability and Flexibility: The ability to take your HSA with you if you change jobs or retire offers peace of mind and continuous access to your healthcare savings.

- Can Afford Higher Deductible: If you have a solid emergency fund and are comfortable with the higher deductible of an HDHP, the lower premiums combined with HSA benefits can lead to significant overall savings.

Maximizing Your Health Savings: Strategic Tips

Regardless of which account you choose, or if you qualify for both, strategic planning can help you get the most out of your healthcare savings.

- Understand Your Health Plan: Always thoroughly review your health insurance policy. Know your deductible, co-pays, and out-of-pocket maximums. This information is key to estimating your healthcare spending.

- Plan Your Spending: For an FSA, estimate your anticipated medical expenses for the year. Try to be as accurate as possible to avoid the “use-it-or-lose-it” scenario. For an HSA, consider your immediate needs versus long-term savings goals.

- Consider Both if Eligible: In some cases, if you have an HDHP, you might also be eligible for a “Limited-Purpose FSA.” This type of FSA can only be used for dental and vision expenses, allowing you to use it alongside an HSA for comprehensive savings. Always confirm eligibility with your employer.

- Save Receipts: Keep detailed records of all your medical expenses and receipts. This is crucial for verifying qualified expenses, especially for HSA withdrawals in the future.

- Contribute Consistently: Make regular contributions to your chosen account. Even small, consistent contributions can add up significantly over time, especially with the investment growth of an HSA.

Conclusion

Choosing between an FSA vs HSA is a pivotal financial decision that impacts your healthcare costs and overall tax strategy. While both offer valuable tax advantages for medical expenses, their structures cater to different needs and circumstances.

An FSA provides immediate tax relief for predictable annual healthcare costs and is tied to your employer. An HSA, on the other hand, offers a powerful long-term savings and investment vehicle for those with a High-Deductible Health Plan, providing ultimate portability and triple tax benefits.

By carefully evaluating your health insurance plan, anticipated medical expenses, and long-term financial goals, you can select the account that best aligns with your needs. Proactive planning in this area ensures you are well-prepared to manage healthcare costs effectively, securing both your health and your financial future.