Introduction

The financial landscape constantly shifts, influenced by a myriad of factors. Among these, interest rates stand as a formidable force, shaping everything from mortgage payments to investment returns. For investors participating in the peer-to-peer (P2P) lending market, understanding these shifts is absolutely crucial. P2P lending offers an alternative avenue for individuals and small businesses to secure financing, bypassing traditional banks. Lenders, in turn, aim to generate attractive returns on their capital.

However, when central banks opt to raise interest rates, the ripple effect is felt across all sectors. This article explores the multifaceted impact of high interest rates on P2P lending returns. We will delve into how these economic adjustments can create both opportunities and challenges for P2P lenders, ultimately influencing their profitability and risk exposure.

Understanding Peer-to-Peer (P2P) Lending

What is P2P Lending?

Peer-to-peer lending connects individual borrowers with individual lenders directly, often through online platforms. These platforms act as intermediaries, facilitating the loan application, risk assessment, and repayment processes. Borrowers typically seek personal loans, small business financing, or debt consolidation. Lenders, conversely, are investors looking to earn interest by funding these loans.

The P2P model aims to offer more competitive rates than traditional banking for borrowers and potentially higher returns for lenders. This is because P2P platforms often have lower overheads compared to large financial institutions. For example, a borrower might get a personal loan at 8% APR through a P2P platform, while a traditional bank might charge 10% for a similar risk profile.

Key Factors Influencing P2P Returns

Several elements dictate the returns a P2P lender can expect. Firstly, borrower creditworthiness is paramount. Loans to individuals with excellent credit scores typically carry lower interest rates but also lower default risk. Conversely, loans to higher-risk borrowers may offer elevated interest rates to compensate for the increased likelihood of non-payment.

Secondly, the loan terms, including duration and repayment structure, play a significant role. Longer-term loans generally come with higher interest rates. Thirdly, platform fees can eat into a lender’s gross returns. Most platforms charge fees for loan origination, servicing, or collection. Finally, broader economic conditions, such as employment rates and inflation, directly influence borrowers’ ability to repay and the overall demand for credit.

You can find more detailed information on various P2P platforms and their offerings through reputable financial news outlets like Investopedia.

The Mechanics of High Interest Rates

Central Bank Policies and Economic Cycles

Central banks, like the U.S. Federal Reserve, wield significant power over interest rates. They primarily use rate adjustments as a tool to manage economic stability. When inflation rises too rapidly, central banks often increase their benchmark interest rate. This action makes borrowing more expensive across the entire economy. For instance, the cost for banks to borrow from each other increases, which they then pass on to consumers and businesses.

This increased cost of borrowing is designed to slow down economic activity. It discourages consumer spending and business investment, thereby reducing demand and, in theory, curbing inflationary pressures. Consequently, a period of rising rates often signals an effort to cool down an overheating economy.

How High Rates Affect Traditional Lending

The impact of higher interest rates is immediately evident in traditional lending markets. Mortgage rates climb, making homeownership less affordable. Auto loan rates increase, raising the monthly payments for new car buyers. Businesses face higher costs for securing lines of credit or investment loans, which can slow expansion and job creation.

Furthermore, savings accounts and Certificates of Deposit (CDs) offered by traditional banks may start to offer more attractive returns. This makes them more competitive as investment options. For example, a bank CD that offered 0.5% interest might suddenly offer 3% or 4%, drawing capital away from riskier investments.

Understanding these broader economic shifts is essential for any investor. The Federal Reserve’s official website provides comprehensive data and statements on monetary policy decisions.

Direct Impact on P2P Lending Returns

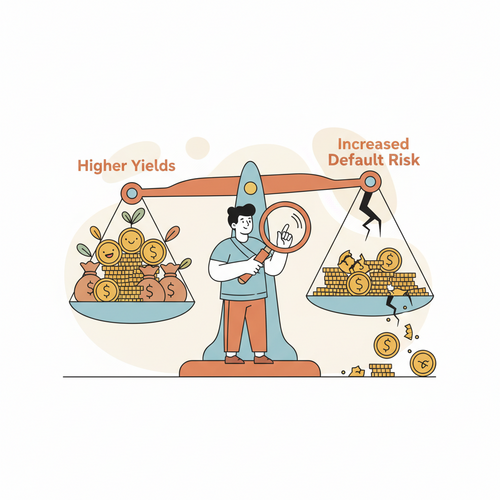

Potential for Higher Yields for Lenders

One of the most immediate and seemingly positive impacts of rising interest rates on P2P lending is the potential for higher gross yields for lenders. As rates increase in traditional markets, P2P platforms must adjust their offerings to remain competitive. They typically raise the interest rates on the loans they facilitate to attract capital from investors.

This means lenders might see new loan opportunities with significantly higher advertised interest rates than before. For example, a loan that previously yielded 7% might now be offered at 9% or 10%. This allows lenders to potentially earn more on their invested capital, assuming all other factors remain constant.

Increased Borrower Default Risk

However, the opportunity for higher yields comes with a significant caveat: increased borrower default risk. When interest rates rise, the cost of borrowing for individuals and businesses also increases. This applies not only to new loans but can also impact existing variable-rate debts. Borrowers might find it more challenging to manage their monthly payments on multiple loans, including their P2P obligations.

An economic slowdown, often a consequence of high interest rates, can further exacerbate this issue. Job losses or reduced income can directly impair a borrower’s ability to repay. Consequently, while the advertised interest rates on P2P loans might increase, the actual net returns for lenders could be diminished by a higher rate of defaults and non-performing loans. Lenders must therefore meticulously evaluate the risk profile of each loan.

Shift in Borrower Demand and Quality

High interest rates also lead to a noticeable shift in borrower demand and the quality of the loan pool available on P2P platforms. When traditional banks increase their lending rates, P2P platforms may become a more attractive alternative for some borrowers. However, this is not always a positive development.

It can mean that lower-risk borrowers, who previously qualified for favorable rates at traditional banks, might now turn to P2P. This could potentially improve the overall quality of the loan pool. Conversely, it might also mean that borrowers who are deemed too risky by traditional lenders – and are therefore willing to accept even higher rates – migrate to P2P platforms. This scenario would increase the average risk profile of P2P loans, even if the interest rates offered seem appealing.

Lenders must be diligent in their due diligence, scrutinizing the credit scores, income stability, and debt-to-income ratios of potential borrowers more carefully in such an environment.

Navigating P2P Lending in a High-Rate Environment

Diversification is Key

In any investment, but especially in P2P lending during periods of volatility, diversification is paramount. Do not put all your capital into a single loan or even a handful of loans. Instead, spread your investments across a large number of individual loans. This strategy helps mitigate the impact of any single default on your overall portfolio returns.

Consider diversifying across different loan types, borrower risk grades, loan durations, and even multiple P2P platforms if possible. For example, you might invest small amounts in 50 different loans instead of a large sum in just five. This approach significantly reduces the concentration risk within your P2P portfolio.

Focus on Borrower Creditworthiness

During times of high interest rates, the importance of borrower creditworthiness becomes even more pronounced. Lenders should prioritize loans to individuals or businesses with strong credit histories and stable income. While these loans may offer slightly lower interest rates than their higher-risk counterparts, their lower default probability makes them more attractive.

- Review credit scores carefully.

- Analyze debt-to-income ratios.

- Consider the borrower’s employment stability.

- Look for loans with collateral if available.

Platforms often provide detailed information on borrower profiles. Taking the time to evaluate this data thoroughly can protect your capital.

Re-evaluating Loan Terms and Maturities

The prevailing interest rate environment should also prompt lenders to re-evaluate loan terms and maturities. In a rising rate environment, shorter-term loans might be preferable. They allow you to re-deploy your capital into new loans at potentially even higher rates sooner. Longer-term loans lock in an interest rate for an extended period, which could become less competitive if rates continue to climb.

Additionally, consider your own liquidity needs. Shorter-term loans generally provide faster access to your capital if circumstances change. Always align your investment strategy with your personal financial goals and risk tolerance. For an insightful perspective on managing personal finance, consult resources like NerdWallet’s personal finance guides.

Staying Informed on Economic Indicators

Finally, staying informed on economic indicators is a critical practice for any P2P investor. Keep an eye on reports regarding inflation rates, unemployment figures, GDP growth, and central bank announcements. These indicators provide valuable insights into the health of the economy and potential future interest rate movements.

- Subscribe to financial news alerts.

- Follow economic analysis from reputable sources.

- Understand the implications of inflation and recession warnings.

Being proactive with your knowledge allows you to anticipate market changes. This enables you to adjust your P2P lending strategy accordingly, potentially mitigating risks and capitalizing on new opportunities.

Conclusion

High interest rates introduce a complex dynamic into the peer-to-peer lending market. On one hand, they present the alluring prospect of higher gross returns for lenders as platforms adjust their rates to remain competitive. This can be a significant draw for investors seeking yield in an otherwise challenging environment.

However, this potential for increased income is inextricably linked with an elevated risk of borrower defaults. As the cost of money rises, borrowers face greater financial strain, increasing the likelihood of missed payments. Therefore, while the headline interest rates may look attractive, a prudent P2P investor must exercise enhanced due diligence. Strategic adjustments, including rigorous diversification, a strong focus on borrower creditworthiness, careful consideration of loan terms, and continuous monitoring of economic trends, are essential. By adopting a well-informed and cautious approach, P2P lenders can better navigate the dual edge of a high-interest-rate environment, striving to optimize returns while effectively managing the inherent risks.