Introduction

In our daily financial lives, we tend to focus on individual numbers: the salary that hits our bank account, the balance on our credit card, or the amount in our savings. While these figures are important, they only tell part of the story. To get a true, holistic picture of your financial standing, you need to look at a single, powerful number: your net worth. Think of your net worth as your personal financial report card or the ultimate scorecard of your financial life. It’s a snapshot in time that clearly shows you what you own versus what you owe. Understanding and tracking this number is one of the most empowering steps you can take. It moves you beyond simply managing your monthly bills and allows you to see your progress, make smarter decisions, and truly gauge your overall financial health.

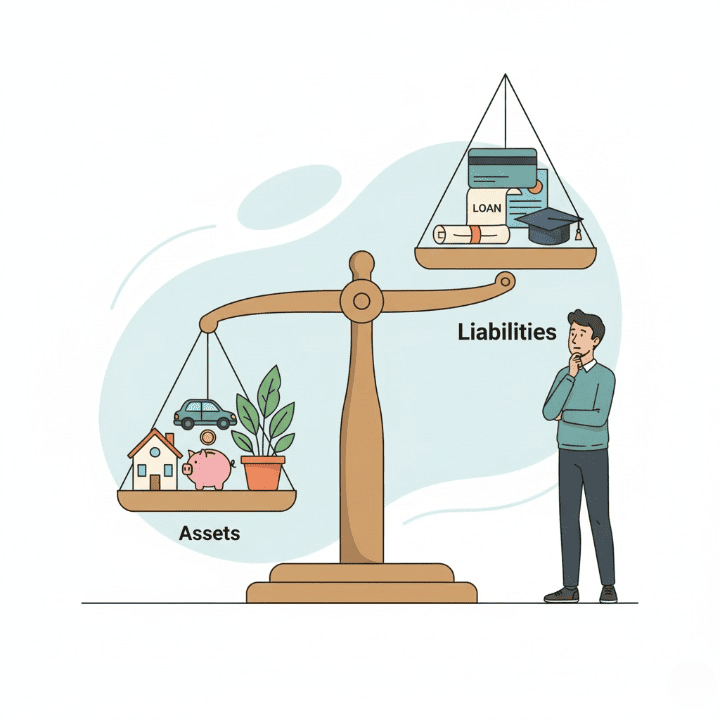

What is Net Worth and Why Does it Matter?

Your net worth is a straightforward calculation. It is the total value of all your assets (everything you own) minus the total value of all your liabilities (everything you owe).

The formula is simple: Assets – Liabilities = Net Worth

This number is crucial because it provides an objective measure of your financial position. A high income is great, but if it’s accompanied by massive debt, your financial situation might be more precarious than you think. Conversely, a person with a modest income who has diligently saved and paid down debt could have a very strong net worth.

Tracking your net worth over time (annually is a good cadence) is where its true power lies. It’s a tangible way to see your progress. When the number is going up, it means your financial decisions are paying off. It’s an incredible source of motivation that shows your hard work is building real, lasting wealth. It can also serve as an early warning system, showing you if your debt is growing faster than your assets.

Tallying Your Assets: What You Own

The first step in calculating your net worth is to make a comprehensive list of all your assets. An asset is anything you own that has monetary value. It’s helpful to group them into a few categories.

- Cash and Cash Equivalents: These are your most liquid assets, meaning they can be accessed quickly.

- Money in your checking and savings accounts.

- Your emergency fund.

- Cash on hand.

- Invested Assets: This is the portion of your wealth that is working to grow over time.

- Retirement accounts (e.g., 401(k), IRA). List the current market value.

- Taxable brokerage accounts with stocks, bonds, or mutual funds.

- The cash value of any whole life insurance policies.

- Physical Assets: These are the tangible items of significant value that you own.

- Real Estate: The current market value of your home (you can get an estimate from real estate websites).

- Vehicles: The current resale value of your car, not what you paid for it.

- Valuables: Any significant collectibles, jewelry, or art that you could realistically sell.

Facing Your Liabilities: What You Owe

The second step is to list all of your liabilities. A liability is any debt or financial obligation you have. This part can be intimidating, but it is an essential step toward financial clarity.

- Secured Debt: This is debt that is tied to a specific asset.

- Mortgage: The remaining balance on your home loan. This is often the largest piece of financing for any household.

- Auto Loans: The outstanding balance on your car financing.

- Unsecured Debt: This debt is not backed by an asset, which is why it often comes with a higher interest rate.

- Credit Card Balances: The total amount you currently owe on all your credit cards. This is a major drain on net worth for many people.

- Personal Loans: Any outstanding personal or signature loans.

- Student Loans: The total remaining balance of your student debt.

- Medical Debt: Any outstanding medical bills.

Mismanaging these liabilities, especially high-interest credit card debt, can quickly erode your net worth and seriously damage your credit score.

The Calculation in Action: A Simple Example

Let’s see how this works with a quick example. Meet Chloe, a 30-year-old graphic designer.

Chloe’s Assets:

- Savings Account: $10,000

- Retirement Account: $25,000

- Car Value: $15,000

- Total Assets: $50,000

Chloe’s Liabilities:

- Student Loan Balance: $20,000

- Car Loan Balance: $8,000

- Credit Card Balance: $2,000

- Total Liabilities: $30,000

Chloe’s Net Worth Calculation: $50,000 (Assets) – $30,000 (Liabilities) = $20,000 (Net Worth)

Chloe’s net worth is positive, which is a great sign. She can now set a goal to increase this number over the next year by paying down her liabilities and adding to her assets.

Strategies to Increase Your Net Worth

There are two fundamental ways to grow your net worth: you can decrease your liabilities or you can increase your assets. The most effective plans do both simultaneously.

Decreasing Liabilities

Focusing on paying down your debt provides a guaranteed “return on investment.” The best place to start is with your highest interest rate debt, which is typically your credit card balances. Every dollar you use to pay off a 20% interest rate debt is like earning a 20% return. As you pay down your loans and credit card balances, you are directly boosting your net worth and improving your credit score.

Increasing Assets

The other side of the equation is to consistently add to your assets. This means regularly contributing to your savings and investment accounts. Even small, automated contributions to a retirement account can grow significantly over time thanks to the power of compounding.

Remember, insurance also plays a crucial protective role. Having proper health, auto, and property insurance acts as a shield for your assets. An unexpected lawsuit or a major house fire could wipe out your assets and destroy your net worth if you are not properly insured.

Conclusion

Calculating your net worth for the first time is a powerful moment of financial clarity. It is not an exercise in judgment, but an act of empowerment. This single number provides the most accurate measure of your true financial health and gives you a baseline from which to grow. By understanding the simple equation of what you own minus what you owe, you can shift your focus from simply managing bills to strategically building wealth. We encourage you to take some time to calculate your own net worth. Track it once a year, and use it as your guide and motivator on the incredible journey of building a secure financial future.