Introduction

When you are shopping for an insurance policy, it is natural to focus on the premium. This is the monthly or annual bill you have to pay. We all want to find the lowest possible premium. However, there is another number in your policy that is just as important for your financial well-being. This number is your deductible.

Your deductible is the amount of money you have to pay out-of-pocket before your insurance coverage starts to pay. Choosing this amount is a critical decision. It directly impacts both your regular budget and your financial exposure in a crisis. This guide will demystify the insurance deductible. We will explain how it works and provide a clear framework to help you choose the right amount for your situation.

What is an Insurance Deductible and How Does it Work?

First, let’s define the term simply. A deductible is a form of cost-sharing. It is an agreement between you and your insurance company. It represents the amount of financial risk that you agree to take on yourself in the event of a claim.

Let’s use a clear, simple example. Imagine you have a $1,000 deductible on your auto insurance policy. If you get into an accident and the repairs to your car cost $4,000, the process is straightforward. You will be responsible for paying the first $1,000 of the repair bill. After you have paid your deductible, your insurance company will then cover the remaining $3,000.

The most important concept to understand is the inverse relationship between your deductible and your premium.

- A high deductible means you are taking on more personal financial risk. To reward you for this, the insurance company will charge you a lower monthly premium.

- A low deductible means the insurance company is taking on more of the risk. To compensate for this, they will charge you a higher monthly premium.

The Core Trade-Off: Lower Premium vs. Higher Out-of-Pocket Cost

The decision of what deductible to choose comes down to a fundamental trade-off. You are balancing your monthly costs against your potential costs in an emergency.

The Case for Choosing a High Deductible

The main benefit of a high deductible is the immediate savings. A higher deductible will result in a lower monthly premium. This frees up more of your cash flow each month. You can then use this extra money in your budget for other important financial goals. For example, you could use it to pay down debt or to increase your savings. This can be a very smart financial move for the right person. However, the risk is that you must be financially prepared to pay that high deductible if you ever need to file a claim.

The Case for Choosing a Low Deductible

On the other hand, the main benefit of a low deductible is greater peace of mind. You know that if an emergency happens, your maximum out-of-pocket cost will be small and predictable. This can reduce financial anxiety. The risk, of course, is that you will have to pay a higher premium every single month for this security. This can put a strain on your regular budget, even if you never file a claim.

The Deciding Factor: Your Emergency Fund

So, how do you make this choice? The answer lies in another key component of your financial life. That component is your emergency fund.

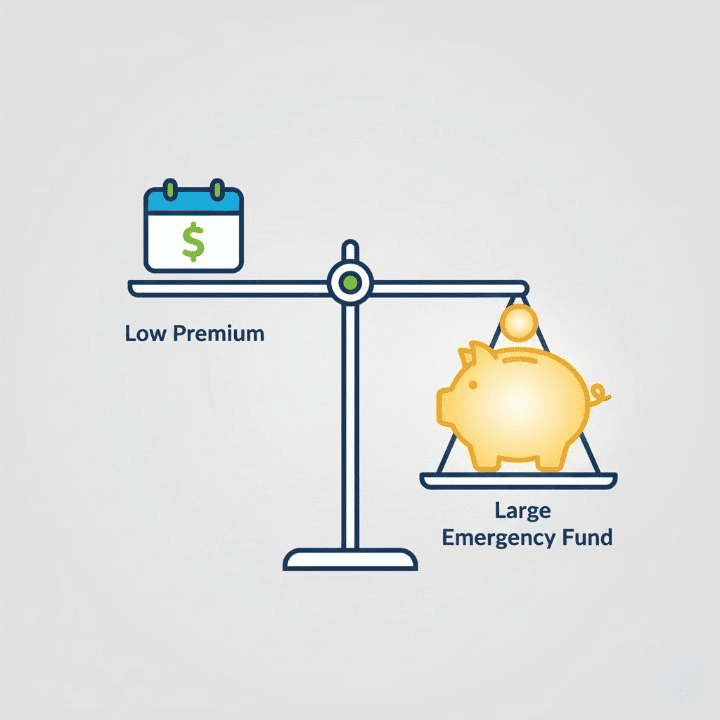

There is a simple golden rule for choosing a deductible. You should never choose a deductible that is higher than the amount of money you have saved in your emergency fund. Your emergency fund is your personal safety net. Your deductible is the amount you will need to pull from that safety net.

If you have a healthy and well-funded emergency fund (typically 3-6 months of living expenses), then choosing a higher deductible can be a very strategic decision. You have the cash on hand to comfortably cover the deductible if a claim arises. In the meantime, you get to enjoy the savings of a lower premium every single month.

However, if you are still in the process of building your emergency fund, a lower deductible might be the safer and more responsible choice. It protects you from a large, unexpected bill that you cannot yet cover with your savings. This is crucial. It prevents you from having to go into debt or use a high interest rate credit card just to pay your deductible. Having to take on new debt after a loss would only make a bad situation worse and could damage your credit.

A Look at Deductibles Across Different Insurance Types

This concept of a deductible applies to many different types of insurance policies, though there can be slight differences.

Auto and Homeowner’s Insurance: These are the most common policies where you will choose a deductible. For auto insurance, you might choose a deductible of $500, $1,000, or more. For homeowner’s insurance, the deductible can sometimes be a flat dollar amount or a percentage of your home’s insured value.

Health Insurance: This is often the most complex. Your health insurance deductible works on an annual basis. This means you must pay a certain amount for covered services each year before your plan starts to pay. After you meet your deductible, you will then typically pay a co-pay or coinsurance for your care. Understanding your deductible is a crucial part of managing your medical financing and your overall health.

Conclusion

In conclusion, choosing your insurance deductible is a strategic financial decision. It is not just a random number on your policy document. It is a balancing act between your monthly costs and your level of emergency preparedness.

The key to making a smart choice is to be honest about your own financial situation. The golden rule is to always align your deductible with the amount of money you have in your emergency fund. This ensures that you can always afford your out-of-pocket responsibility.

By understanding this important trade-off, you can take control of your insurance costs. You can make an informed choice that fits your budget. This protects your savings. Ultimately, it supports your overall and long-term financial health.