Introduction

Where do you see yourself financially in one year? What about in five years, or even ten? For many of us, our financial dreams—buying a home, traveling the world, retiring comfortably—can feel distant and abstract. The gap between where we are today and where we want to be can seem so wide that it’s hard to know where to even begin. The solution is to translate those vague dreams into clear, actionable financial goals. Financial goal-setting is the process of creating a roadmap that guides your decisions and turns your aspirations into reality. As we approach the final quarter of the year, it’s the perfect time to start planning for 2026. This guide will walk you through how to set meaningful goals that can improve your credit, secure your health, and put you on the path to a brighter financial future.

The Power of ‘Why’: Defining Your Financial Goals

Before you can set a goal, you need to understand your motivation. The most effective financial goals are deeply connected to your personal values and what you want out of life. Simply saying “I want to save more money” is not very inspiring. However, saying “I want to save money to have the freedom to travel and the security of a down payment on a home” creates a powerful “why.” This emotional connection is what will keep you motivated when faced with challenges or temptations.

It’s helpful to categorize your goals by their timeline:

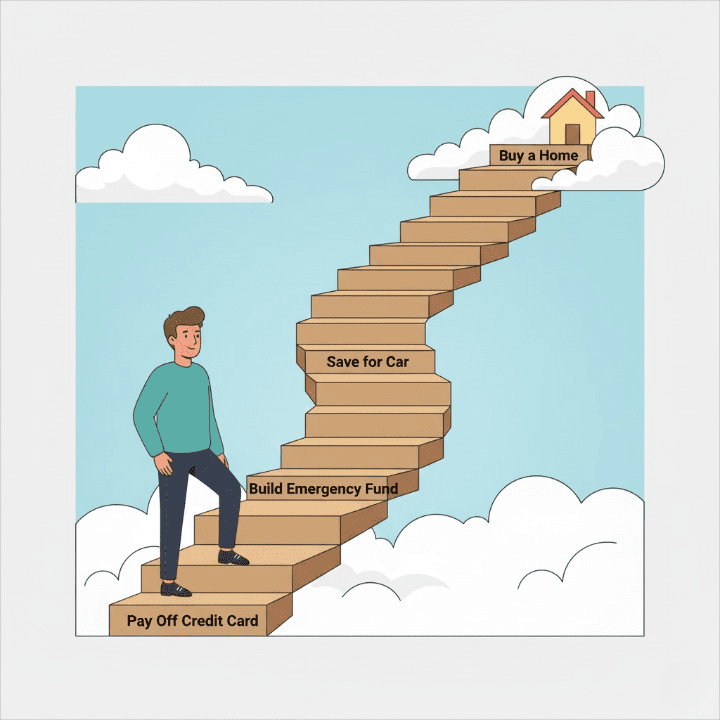

- Short-Term Goals (1-2 years): These are focused, achievable targets that provide quick wins and build momentum. Examples include creating a monthly budget, building a starter emergency fund, or paying off a specific high-interest credit card.

- Mid-Term Goals (3-5 years): These require more sustained effort. Examples include saving for a down payment on a car, paying off a student loan, or saving for a major vacation.

- Long-Term Goals (5+ years): These are the major life milestones that require years of planning. Examples include saving for a down payment on a home, investing for retirement, or saving for a child’s education.

Making Goals Concrete: The SMART Framework

The most effective way to turn a vague desire into an achievable target is to use the SMART framework. This ensures your goals are clear, measurable, and realistic. Let’s use the common goal of paying off a credit card to see how it works.

- S – Specific: Don’t just say, “I want to pay off my credit card.” Instead, be precise: “I will pay off the $3,000 balance on my Visa credit card.”

- M – Measurable: How will you track your progress? In this case, it’s simple: you can measure the balance decreasing from $3,000 to $0.

- A – Achievable: Is your goal realistic given your current income and budget? If you can only afford to put $100 per month toward the debt, paying it off in three months is not achievable. A more realistic plan might be to pay $250 per month.

- R – Relevant: Does this goal align with your “why”? Yes, paying off high-interest debt frees up cash flow for other goals and reduces stress.

- T – Time-bound: Give yourself a deadline. “I will pay off the $3,000 balance on my Visa credit card in 12 months by paying $250 each month.”

Now you have a vague wish transformed into a concrete, actionable plan.

Foundational Goals: Improving Your Credit and Health

Some financial goals act as a foundation for all others. Before you focus on aspirational targets, it’s crucial to ensure your base is secure.

The Goal of Better Credit

Setting a goal like “I want to improve my credit score to over 700” is one of the most powerful financial objectives you can have. Your credit score impacts nearly every other goal you set. A higher credit score unlocks a lower interest rate on any future financing you may need. This means a lower monthly payment and thousands of dollars saved on a mortgage or car loan. Achieving this goal involves creating smaller, supporting goals, such as keeping your credit card balances low and making every single payment on time.

The Goal of Financial Health

Protecting your financial health is another foundational goal. This includes two key components:

- Building an Emergency Fund: As we’ve discussed before, this fund is your safety net.

- Securing Proper Insurance: Having the right health insurance, auto insurance, and other policies is not an expense—it’s protection for your goals. An unexpected medical event or a car accident can derail years of financial progress if you are not properly insured.

The Role of Financing and Interest Rates in Your Goals

Many of our most significant life goals, like buying a home or a car, require financing. In these cases, your financial goal isn’t just to buy the item, but to prepare yourself to borrow money in the smartest way possible. For example, a long-term goal for buying a house is actually a series of smaller goals: improve your credit score, eliminate high-interest debt, and save a 20% down payment.

By achieving these preparatory goals, you put yourself in a position of power. You can approach lenders with a strong financial profile, which allows you to secure financing with a favorable interest rate. A lower rate can reduce your monthly payment by hundreds of dollars and save you tens of thousands over the life of the loan. This demonstrates how foundational goals directly enable you to achieve your larger life aspirations more affordably.

Conclusion

Financial goals are the bridge between your dreams and your reality. They provide direction, motivation, and a clear path forward in what can often feel like a complicated journey. The process starts with understanding your “why” and then transforms those desires into SMART, actionable steps. By focusing first on building a strong foundation—improving your credit, establishing a safety net with savings and insurance, and managing your debt—you create the stability needed to pursue your biggest ambitions. As you look toward the upcoming year, take some time to set one or two meaningful financial goals. This simple act of planning is the first and most important step toward building a more secure, fulfilling, and prosperous future.