Introduction

When we think about building wealth, our focus often goes to strategies like budgeting, saving, and investing. We work hard to set aside money for the future. In doing so, however, we sometimes overlook the most powerful financial engine we have: our ability to earn an income. Your paycheck is the fuel for your entire financial life. For example, it pays for your home, your daily needs, your savings, and your dreams. Have you ever stopped to ask what would happen to your financial plan if that income suddenly disappeared due to a serious health issue or injury? True financial protection involves more than just building a nest egg; as a result, it requires shielding the very source of your wealth. This guide will explore the crucial strategies for protecting your income, showing how tools like insurance and the disciplined use of credit can create a resilient financial life.

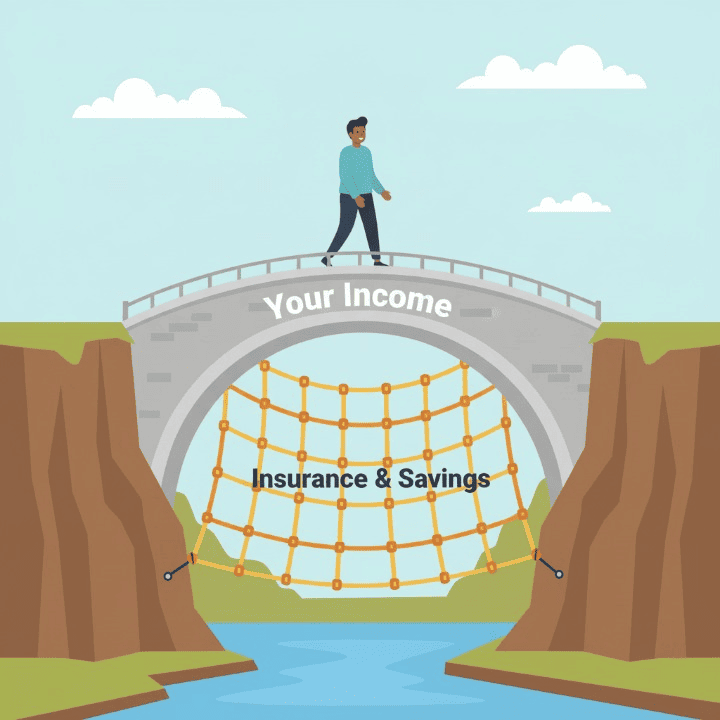

Why Your Income Is Your Most Valuable Asset

It’s easy to think of your home or your car as your most valuable asset, but a simple calculation reveals the truth. Even a modest annual salary, when multiplied over a 40-year career, adds up to a staggering amount. In fact, it often totals well over a million dollars. This future stream of income is the foundation upon which your entire financial structure rests. Without it, paying for your existing financing obligations, like a mortgage or car loan, becomes impossible. Consequently, saving for retirement grinds to a halt and your family’s well-being is put at risk.

Most of us know to protect tangible assets with home and auto insurance. However, protecting the income that pays for everything is a step that people frequently overlook. A robust financial protection plan acknowledges that your ability to work and earn is your greatest asset. Therefore, it takes deliberate steps to insure it against life’s uncertainties.

The Ultimate Safety Net: Understanding Disability Insurance

The single most powerful tool for protecting your income is disability insurance. Many people mistakenly believe that disabilities are rare and only result from freak accidents. The reality, however, is that the vast majority of long-term disabilities come from common illnesses such as cancer, heart disease, back problems, or serious mental health conditions.

Disability insurance is a type of policy that replaces a percentage of your income. It provides this support if you become physically or mentally unable to work due to an illness or injury. There are generally two types:

- Short-Term Disability Insurance: This coverage typically replaces 60-80% of your income for a short period, usually three to six months. Many employers offer this as part of their benefits package. They design it to cover you during the initial phase of a health issue.

- Long-Term Disability Insurance: This policy is for more severe, prolonged conditions. It begins after your short-term benefits run out and can last for several years, or even until you reach retirement age. While some employers offer a group plan, the coverage may be limited. This makes a private policy a crucial consideration for comprehensive protection.

The Domino Effect of an Unprotected Income Loss

To understand the importance of income protection, you can consider the devastating domino effect of a long-term health problem without adequate insurance.

For example, imagine a professional who suffers a serious health condition and cannot work for a year. They have some savings but no long-term disability policy.

- Savings Deplete: Within a few months, their emergency fund is completely gone. They use it up on mortgage payments, utilities, and groceries.

- Turn to Debt: To cover ongoing expenses, they begin to rely on their credit card. The balance quickly grows.

- Interest Accumulates: The high interest rate on the credit card balance causes the debt to swell. This makes a bad situation even worse.

- Payments Are Missed: As the debt deepens, they start missing payments on their car financing and other loans.

- Credit Is Damaged: Creditors report these missed payments to credit bureaus, which in turn causes their credit score to plummet.

In this scenario, a single health crisis has now triggered a full-blown financial crisis. This leads to overwhelming debt and long-term damage to their credit. Disability insurance is the firewall that prevents this from happening.

The Role of Emergency Funds and Credit in a Crisis

A complete financial protection plan involves multiple layers of defense that must work together.

- Your Emergency Fund is Layer One: This is your immediate cash reserve. You should design it to cover your expenses during the “elimination period” of your disability insurance policy. This is the waiting period (often 90 days) before your benefits begin to pay out.

- Your Credit Card is a Last Resort: A credit card can feel like a lifeline in a crisis. However, you should only use it for survival once all other options are exhausted. Using it as a long-term income replacement strategy is unsustainable due to the high interest rate. Furthermore, it can inflict severe damage on your credit.

Proper planning means using your emergency fund to protect your credit. This gives your insurance policy time to activate. Ultimately, this strategic approach prevents you from trading a health crisis for a debt crisis.

Building a Resilient Financial Life

Creating a truly resilient financial life means you must prepare for interruptions. Your income protection strategy should be multi-layered to be effective.

- The Foundation: First, build and maintain a fully funded emergency fund of three to six months’ worth of essential living expenses.

- Employer Benefits: Next, understand the short-term and long-term disability insurance plans your employer offers. You should know the coverage amounts and limitations.

- Fill the Gaps: In addition, if your employer’s coverage is insufficient, you should supplement it with a private long-term disability insurance policy.

- Proactive Health: Finally, prioritize your physical and mental health. A healthy lifestyle is a powerful form of risk management that can reduce your chances of needing to rely on your safety nets in the first place.

Conclusion

True financial protection goes beyond saving for the future; it also involves protecting your ability to save. A combination of a robust emergency fund and comprehensive disability insurance provides the key to weathering major life storms. This strategy protects you from crippling debt, preserves your hard-earned credit, and reduces the immense stress that comes with financial uncertainty. By taking proactive steps today to insure your income, you are securing the foundation of your family’s financial future and well-being.