Introduction

You may have heard a famous quote often attributed to Albert Einstein, calling compound interest the “eighth wonder of the world.” While the quote’s origin is debatable, its sentiment is not. Compound interest is one of the most powerful, yet least understood, forces in personal finance. It is a simple concept with profound consequences, acting as a two-sided coin that can either be your greatest ally in building wealth or your most formidable foe in creating debt. Understanding how this mechanism works is absolutely essential for making smart financial decisions, whether you are saving for the future or considering any form of financing. This guide will demystify compound interest, showing you how it works, how it can help you, and how it can hurt you, especially when dealing with a high interest rate.

What is Compound Interest?

To understand compound interest, it helps to first understand simple interest. Simple interest is calculated only on the original principal amount. For example, if you save $1,000 at a simple interest rate of 5% per year, you would earn $50 every year.

Compound interest, on the other hand, is far more powerful. It is interest calculated on the initial principal and on the accumulated interest from previous periods. It’s “interest on interest.”

Think of it like a snowball rolling down a hill. It starts small, but as it rolls, it picks up more snow. The bigger it gets, the more snow it collects with each rotation, causing it to grow faster and faster. Time is the hill, and the interest rate is the stickiness of the snow. This accelerating growth is the magic—and the danger—of compounding.

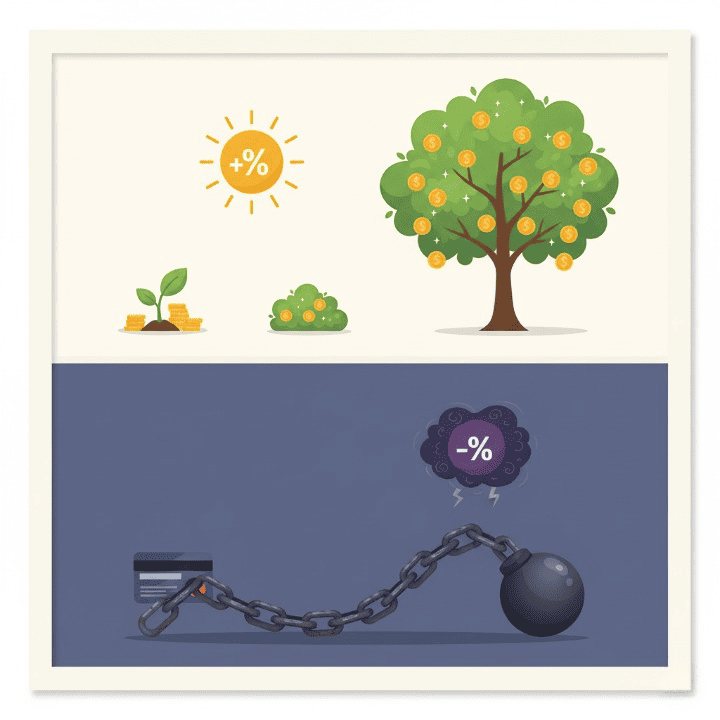

The “Eighth Wonder”: Compound Interest Working For You

When you are saving or investing, compound interest is your best friend. It allows your money to grow exponentially over time, with very little effort on your part. The two key ingredients you need are a consistent rate of return (your interest rate) and, most importantly, time.

Let’s look at a simple example. Imagine you invest $1,000 in an account with a 7% annual interest rate that compounds once a year.

- After Year 1: You earn 7% of $1,000, which is $70. Your new balance is $1,070.

- After Year 2: You earn 7% of your new balance of $1,070, which is $74.90. Your new balance is $1,144.90.

- After Year 3: You earn 7% of $1,144.90, which is $80.14. Your new balance is $1,225.04.

Notice that the amount you earn each year is increasing. While it may not seem like much at first, the effect becomes dramatic over longer periods. After 20 years, without adding another penny, that initial $1,000 would grow to nearly $3,870. This is how small, consistent savings can transform into significant wealth over a lifetime.

The Dark Side: Compound Interest Working Against You

While compounding is a wonderful force for savers, it is a destructive one for borrowers, especially when dealing with high-interest debt. The most common example of negative compounding is the credit card.

Let’s flip the scenario. Imagine you have a $2,000 balance on a credit card with a high 21% annual interest rate. Credit card interest often compounds daily or monthly, making it even more aggressive. If you only make the minimum payments, a large portion of that payment is immediately consumed by the interest charges for that month. Very little goes toward reducing the actual principal.

Because the interest is calculated on a constantly high balance, the debt can feel almost impossible to escape. A $2,000 purchase can end up costing you $3,000, $4,000, or more in the long run if you only make minimum payments. This is the snowball effect in reverse, creating an avalanche of debt that can cause immense stress, damaging both your financial and mental health. This is why paying down high-interest debt should always be a top financial priority.

How This Affects Your Credit and Financing Options

The negative effects of compound interest on debt extend far beyond just the money you owe. When a credit card balance spirals, it can have serious consequences for your overall financial life.

A large, growing balance increases your credit utilization ratio—the amount of debt you have compared to your credit limit. A high utilization ratio is a major red flag to lenders and can significantly lower your credit score. If the debt becomes unmanageable and you start to miss payments, the damage to your credit will be even more severe.

This creates a vicious cycle. A damaged credit score means that any future financing you might need, such as a car loan or a mortgage, will be much harder to obtain. If you are approved, you will be offered a much higher interest rate because you are now considered a riskier borrower. In essence, failing to control compound interest on a small scale (like a credit card) can make all other forms of borrowing more expensive for years to come.

Using Insurance as a Shield Against Negative Compounding

So, how do you stay on the right side of the compounding equation? Beyond disciplined saving and debt repayment, having a proper safety net is crucial. This is where insurance plays a vital role.

Think of insurance (health, auto, home) as a protective shield against the very events that often trigger high-interest debt. An unexpected surgery, a major car accident, or a fire at home can all lead to massive, immediate expenses. Without insurance to cover the bulk of these costs, many people are forced to rely on a credit card or emergency financing, thus starting the negative compounding cycle. Your insurance policy handles the catastrophic cost, leaving you to cover only your deductible, which can ideally be paid from an emergency fund. In this way, insurance is a critical risk management tool that keeps you out of the high-interest debt trap.

Conclusion

Compound interest is a neutral, mathematical force, but its impact on your life is deeply personal. It can be a gentle breeze at your back, pushing you toward your financial goals, or a fierce headwind holding you back. The direction it pushes depends entirely on your actions. By saving and investing early, you give your money the time it needs to grow and harness the positive power of compounding. By aggressively paying down any high-interest rate debt, especially from a credit card or other short-term financing, you escape its destructive grasp. Understanding this single, powerful concept is one of the most important steps you can take in your journey toward financial empowerment and a secure future.