Introduction

We often hear the phrase “health is wealth,” and for good reason. Our physical and mental well-being is the most valuable asset we possess. However, in the modern world, it is impossible to separate our physical health from our financial health. The two are deeply intertwined, each capable of significantly impacting the other. A sudden illness can lead to overwhelming medical bills, while the constant stress of debt can take a toll on our physical well-being. Achieving a true state of wellness requires a holistic approach that includes managing your finances with the same care you give your body. This guide will explore this critical intersection. We will focus on how you can proactively manage healthcare costs and protect your financial future using essential tools like insurance and a smart understanding of credit.

The Undeniable Link Between Health and Wealth

The connection between our finances and our health flows in both directions. On one hand, poor physical health can be incredibly expensive. It can lead to high costs for doctor visits, prescription medications, and hospital stays. It can also result in lost income if you are unable to work. This combination of rising expenses and decreasing income can create immense financial stress.

On the other hand, that financial stress itself is a major health issue. Worrying about how to pay bills, manage a high-interest credit card balance, or deal with a damaged credit score can lead to anxiety, depression, and sleep deprivation. These conditions can, in turn, contribute to physical health problems like high blood pressure and a weakened immune system. Therefore, taking proactive steps to organize your finances is not just a money issue; it’s a crucial part of your overall self-care routine. Investing in your financial health is an investment in your long-term physical and mental well-being.

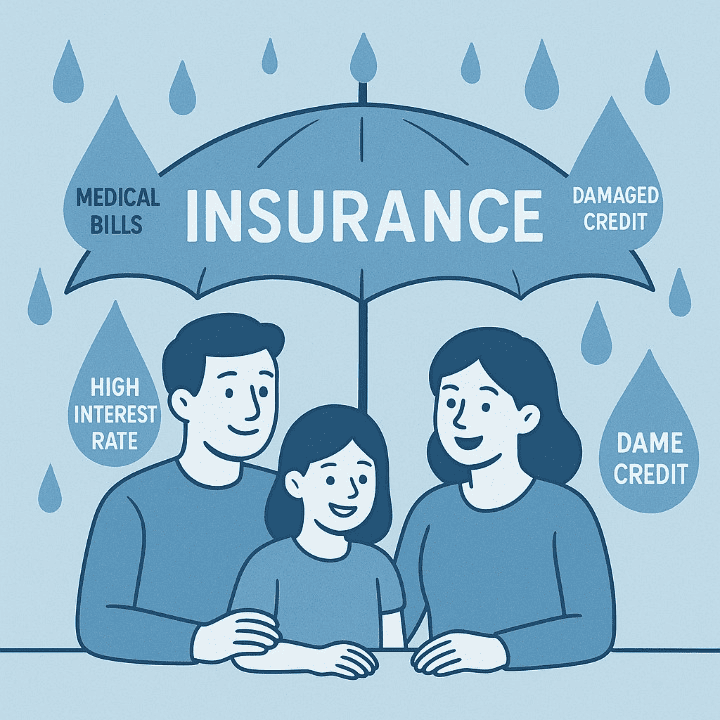

Your First Line of Defense: The Role of Health Insurance

When it comes to protecting your finances from unexpected medical events, health insurance is your single most important tool. It acts as a financial safety net designed to absorb the majority of the cost of catastrophic health events. Without it, a single accident or serious diagnosis could potentially lead to financial ruin for many families.

Understanding how insurance functions from a financial perspective is key. You pay a predictable monthly fee, called a premium, in exchange for protection from unpredictable and potentially massive costs. When you do need medical care, you will likely have to pay a certain amount out-of-pocket—through deductibles, copayments, and coinsurance—but the insurance company covers the rest.

Consider this simple scenario: an unexpected surgery results in a $30,000 hospital bill.

- Without insurance, you would be responsible for the entire $30,000. This would likely require you to drain your savings, sell assets, or take on significant debt.

- With a decent insurance plan, after you meet your deductible and out-of-pocket maximum (perhaps $5,000 in this example), the insurance company would pay the remaining $25,000. While $5,000 is still a major expense, it is far more manageable than the full amount. This is how health insurance provides financial protection and peace of mind.

Navigating Out-of-Pocket Costs: The Credit Card Dilemma

Even with good health insurance, you will still face out-of-pocket costs. These can include your annual deductible, copayments for doctor visits, and the cost of prescription drugs. For many people, the most convenient way to cover these immediate expenses is to use a credit card. While this can be a useful short-term solution, it comes with a significant risk.

The main danger lies in the high interest rate associated with most credit cards. If you charge a $2,000 medical bill to your card and are unable to pay it off in full at the end of the month, that balance will start to accumulate interest. A typical credit card interest rate can be 20% or even higher. Over time, these interest charges can add hundreds or even thousands of dollars to your original bill, turning a manageable medical expense into a long-term debt problem. This can trap you in a cycle of stress that is detrimental to both your financial and physical health.

When Costs Are Too High: Exploring Financing Options

What should you do if you face a medical bill that is too large to pay off quickly, even with a credit card? Before letting it go to collections, it is important to explore alternative financing options that may offer better terms.

Many healthcare providers are willing to work with patients. The first step should always be to call the hospital or clinic’s billing department and ask about payment plans. Often, they can offer a structured plan that allows you to pay off the bill over several months or years with no interest or a very low interest rate. This is almost always a better option than high-interest credit card debt.

If that is not an option, a personal loan from a bank or credit union could be another solution. For those with a good credit score, a personal loan typically offers a fixed interest rate that is significantly lower than a credit card’s variable rate. This makes the payments more predictable and the total cost of borrowing much lower. Securing this type of financing depends heavily on your credit history, which is another reason why maintaining good credit is so vital for your overall financial security.

Protecting Your Future: How Medical Debt Impacts Your Credit

Allowing medical bills to go unpaid can have severe consequences for your financial future. If a bill remains unpaid for several months, the healthcare provider may sell the debt to a collection agency. Once an account goes into collections, it is reported to the major credit bureaus.

A collection account on your credit report is a major negative event that can cause your credit score to drop significantly. This damage can last for up to seven years. A lower credit score makes it more difficult and expensive to get approved for any future financing, from a car loan to a mortgage. This is how a single health crisis can create long-lasting financial challenges. It underscores the importance of being proactive: using insurance as your primary shield and thoughtfully managing any remaining costs to protect your credit.

Conclusion

Your physical health and your financial health are two sides of the same coin of well-being. Nurturing one often means nurturing the other. By taking a proactive approach to your health, you can reduce the likelihood of costly medical issues. By building a strong financial plan, you create a resilient foundation that can withstand life’s unexpected challenges. This involves prioritizing good health insurance, being extremely cautious about using a credit card for medical costs due to the high interest rate, and exploring better financing options when needed. Protecting your credit from the impact of medical debt is essential for your long-term goals. Ultimately, by managing both aspects of your life with care, you build a future that is not only healthier but also more secure.