Introduction

Moving into a new rental apartment is an exciting milestone. It represents independence, a new beginning, and the freedom to create a space that is truly yours. As you settle in, you might feel a sense of security knowing that your landlord has an insurance policy on the building. This leads many renters to a common and dangerous assumption: “My landlord has insurance, so I’m covered, right?” The answer, in short, is no. Your landlord’s policy is designed to protect their investment—the physical building itself. It does nothing to protect your personal belongings or shield you from liability. This is where renter’s insurance comes in. It is an affordable but incredibly powerful financial safety net designed specifically for you, the tenant. This guide will explain what this often-overlooked insurance covers and why it is one of the most important financial decisions a renter can make.

The Big Misconception: Landlord’s Insurance vs. Renter’s Insurance

Understanding the fundamental difference between these two policies is the first step toward appreciating the need for your own coverage. Think of it this way: the landlord insures the “box” you live in, while you need to insure your “life inside the box.”

- Landlord’s Insurance: This policy covers the physical structure of the building—the roof, the walls, the flooring, and built-in appliances. If a fire damages the building, their insurance pays to repair it. It also protects the landlord from liability claims if, for example, a faulty staircase injures someone in a common area. It provides zero coverage for your personal property.

- Renter’s Insurance: This policy protects you. It covers your personal belongings, protects you from personal liability, and can even help with temporary living expenses if your apartment becomes uninhabitable. It is your personal financial shield within the walls of the property you rent.

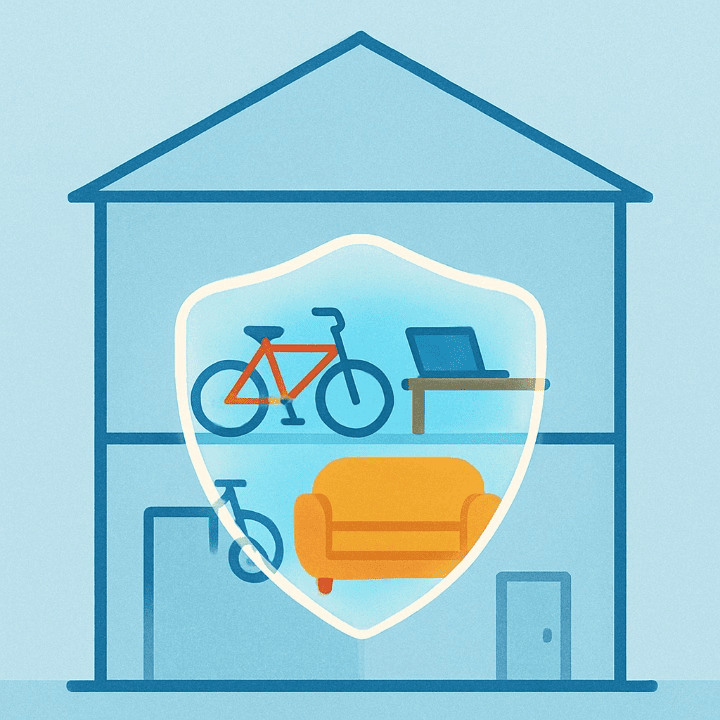

The Three Pillars of Renter’s Insurance Coverage

A standard renter’s insurance policy is built on three essential types of coverage that work together to provide comprehensive protection.

Pillar 1: Personal Property Protection

This is the part of the policy that most people think of first. It covers the cost to repair or replace your personal belongings if they are damaged or destroyed by a covered event, such as a fire, theft, vandalism, or certain types of water damage. This includes everything you own: your furniture, electronics, clothes, kitchenware, and more. When choosing a policy, you will often see two options for this coverage:

- Actual Cash Value (ACV): This pays for the depreciated value of your items. For example, it would pay what your five-year-old laptop is worth today, not what you paid for it.

- Replacement Cost: This pays the full cost to purchase a new, similar item. Although this coverage might make your premium slightly higher, it is almost always the better option as it provides the funds to truly replace what you lost.

Pillar 2: Personal Liability Coverage

This is a critically important, yet often misunderstood, benefit. Personal liability coverage protects you financially if you are found responsible for injuring someone or damaging their property. For example, if a guest slips and falls in your apartment and sues you for their medical bills, this coverage can help pay for those costs and your legal defense. It also covers you if you accidentally cause damage, like if your overflowing bathtub damages the apartment of the neighbor below you. Without this coverage, a single accident could lead to a lawsuit that could financially devastate you, ruining your savings and your credit for years.

Pillar 3: Additional Living Expenses (ALE) / Loss of Use

What would you do if a fire or major pipe burst made your apartment uninhabitable for a month? Where would you live? This is where Additional Living Expenses (ALE) coverage comes in. If you are forced to leave your home due to a covered event, this part of your policy helps pay for the reasonable increase in living costs. This can include expenses like a hotel stay, meals, and laundry services while your apartment is being repaired. It ensures that a disaster doesn’t leave you without a place to stay.

How Much Does It Really Cost? (Hint: Less Than You Think)

Many renters skip this crucial insurance because they assume it is expensive. In reality, renter’s insurance is one of the most affordable types of insurance available. The average cost is often comparable to the price of a couple of coffees or a single streaming service subscription per month. The exact price will depend on factors like your geographic location, the amount of coverage you choose, and your selected deductible (the amount you pay out-of-pocket on a claim). For a small monthly investment, you are buying a massive amount of financial security.

A Practical Scenario: The Kitchen Fire

To see the real-world value, let’s imagine two neighbors, Liam and Sarah, who live in identical apartments in the same building. One evening, a grease fire starts in Liam’s kitchen while he is cooking. The fire is contained quickly, but it causes significant smoke and water damage to both his and Sarah’s apartments, making them both temporarily uninhabitable.

- Liam (Uninsured): Liam loses his laptop, television, and most of his furniture to smoke damage. He has to pay out-of-pocket to replace every single item, forcing him to drain his savings account and accumulate thousands of dollars in credit card debt. Furthermore, he has to pay for a hotel for three weeks while the landlord’s insurance company repairs the apartment. The financial and emotional stress is immense, and the new debt damages his credit score.

- Sarah (Insured): Sarah contacts her insurance company. Her renter’s insurance policy with replacement cost coverage pays for her to buy a new laptop, television, and furniture. Her Additional Living Expenses coverage pays for her hotel stay and meal costs, so she isn’t out-of-pocket for her temporary housing. A single, devastating event becomes a manageable inconvenience because she had the right protection. She avoids debt and her financial health remains intact.

Conclusion

Renting offers flexibility and freedom, but it does not remove the risk of unexpected events. Renter’s insurance is not an optional luxury; it is a fundamental element of financial protection for any modern renter. For a small monthly premium, you are protecting the full value of your personal belongings, shielding yourself from potentially devastating liability lawsuits, and ensuring you will have a roof over your head if disaster strikes. It is the affordable safety net that protects your savings, your credit, and your peace of mind, allowing you to truly enjoy the place you call home.