Introduction

When you are ready to take a significant step in your financial life, such as buying a car, a home, or even getting a credit card, you will encounter one of the most critical terms in any contract: the interest rate. It’s the cost of borrowing money, and it directly impacts your monthly payments and the total amount you will pay over time. But not all interest rates are created equal. They generally come in two main “flavors”: fixed and variable. The choice between these two can have a profound effect on your budget and financial stability for years to come. Understanding the difference is not just for financial experts; it’s essential knowledge for anyone seeking financing. This guide will break down what fixed and variable interest rates are, the pros and cons of each, and how you can decide which path is the right one for you.

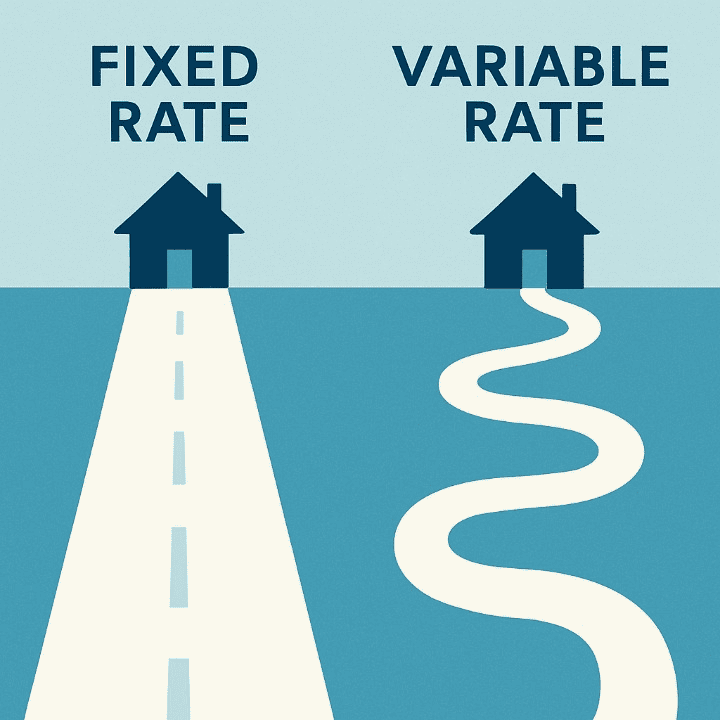

What is a Fixed Interest Rate? The Path of Predictability

A fixed interest rate is exactly what it sounds like: an interest rate that is locked in and does not change for the entire term of the loan. If you secure a personal loan with a 7% fixed interest rate for five years, you will pay 7% for that entire five-year period, regardless of what happens in the broader economy.

Think of it like signing a lease on an apartment with a fixed monthly rent. You have complete certainty about what your payment will be each month. This predictability is the primary appeal of a fixed interest rate.

Pros:

- Stability and Predictability: Your principal and interest payment remains the same every single month. This makes budgeting simple and stress-free.

- Protection from Rising Rates: If market interest rates go up, yours stays the same. You are shielded from economic fluctuations.

- Simplicity: It’s easy to understand and calculate the total cost of your financing over its lifetime.

Cons:

- Potentially Higher Starting Rate: Lenders take on more risk with a fixed rate (because they can’t raise it if their own costs go up), so they might offer a starting rate that is slightly higher than an initial variable rate.

- No Benefit from Falling Rates: If market interest rates fall, you are stuck with your higher, locked-in rate unless you go through the process of refinancing.

Commonly Used For: Mortgages, auto loans, and personal loans, where predictable payments over a long period are highly valued.

What is a Variable Interest Rate? The Path of Flexibility

A variable interest rate, sometimes called a floating or adjustable rate, can change over the life of the financing. It is tied to an underlying benchmark index, such as the prime rate. When this benchmark rate goes up or down due to economic changes, your interest rate goes up or down with it.

You can compare this to the price of gasoline. It can fluctuate weekly or even daily based on market conditions. This means your monthly payment is not set in stone and can change over time.

Pros:

- Lower Initial Rate: Variable rates often start lower than fixed rates, making your initial monthly payments more affordable.

- Potential for Savings: If the benchmark interest rate falls, your rate will also fall, reducing your monthly payments and the total interest you pay.

- Good for Short-Term Financing: If you plan to pay off the loan quickly, you might benefit from the lower initial rate without being exposed to long-term risk.

Cons:

- Lack of Predictability: Your monthly payments can change, making it harder to budget with precision.

- Risk of Rising Payments: If market interest rates rise significantly, your monthly payments could increase dramatically, potentially straining your budget.

- Complexity: Understanding how and when your rate will adjust can be more complicated.

Commonly Used For: Credit cards, home equity lines of credit (HELOCs), and some private student loans.

A Tale of Two Mortgages: How the Choice Impacts a Homeowner

To see the real-world impact, let’s imagine two friends, Emma and Ben. They both buy their first homes at the same time and take out a $300,000 mortgage.

- Emma chooses a 30-year fixed-rate mortgage at 6%. Her principal and interest payment is set at approximately $1,798 per month. She knows that this exact amount will be due every month for the next 30 years. This gives her immense peace of mind and allows her to plan her financial future with certainty.

- Ben opts for a variable-rate mortgage with a lower initial rate of 5%. His starting payment is about $1,610 per month, saving him nearly $200 a month compared to Emma. For the first few years, he feels great about his choice. However, after the initial period, the economy shifts, and market interest rates rise. His rate adjusts upward to 7.5%. His monthly payment now jumps to over $2,098, an increase of almost $500 from his starting payment. This new, higher payment puts a significant strain on his monthly budget.

This scenario perfectly illustrates the core trade-off: Emma paid a little more for stability, while Ben took a risk for a lower initial cost and was eventually impacted by it.

Key Questions to Ask When Choosing Your Financing

There is no single “correct” answer. The right choice depends on your personal circumstances and comfort level with risk. Ask yourself these questions:

- What is my risk tolerance? Can I comfortably handle the stress and budgetary impact if my monthly payment were to increase by 20%, 30%, or more?

- How long is the financing term? For short-term loans, a variable rate can be less risky. For long-term financing like a 30-year mortgage, the stability of a fixed interest rate is often far more appealing.

- What is the economic outlook? While no one can predict the future with certainty, you can research whether economists generally expect interest rates to rise or fall in the coming years.

- Can I afford the worst-case scenario? Variable-rate loans usually have a “rate cap,” which is the maximum interest rate they can reach. Calculate what your monthly payment would be at that maximum rate. If that number would break your budget, a fixed rate is a much safer choice.

Conclusion

The choice between a fixed and a variable interest rate is one of the most important decisions you will make when taking on new financing. It’s a fundamental trade-off between predictability and potential savings. A fixed rate offers the comfort of a stable, unchanging payment, making it ideal for long-term planning and those with a lower tolerance for risk. A variable rate, on the other hand, can offer a lower starting cost with the potential for future savings, but it comes with the inherent risk of rising payments. By carefully considering your personal financial situation, the length of the loan, and your own comfort with risk, you can make an empowered and informed decision that best aligns with your financial goals.