Introduction

If you are just starting your financial journey, you have probably heard this piece of advice: “always choose a credit card with no annual fee.” For the most part, this is sound guidance. Why pay for something when there are so many free alternatives available? This simple logic helps many people avoid unnecessary costs. However, here’s a statement that might surprise you: for some people, paying an annual fee for a credit card can be one of the smartest financial decisions they make. These cards often unlock a world of valuable perks, enhanced rewards, and robust insurance protections that can far outweigh their yearly cost. The key is knowing how to determine if you are one of those people. This guide will provide a clear framework to help you do the math, analyze the benefits, and confidently answer the annual fee question for yourself.

What is an Annual Fee and Why Do Some Cards Have Them?

An annual fee is exactly what it sounds like: a fixed price that a credit card issuer charges you once a year simply for keeping the account open. These fees can range from a modest amount, perhaps under $100, to well over $500 for the most exclusive premium cards.

But why do they exist? In short, these fees fund the premium benefits that come with the card. Think of it as a “pay-to-play” model. Providing perks like airport lounge access, annual travel credits, and comprehensive travel insurance policies is expensive for financial institutions. The annual fee helps cover these costs, allowing them to offer a higher tier of service and value to customers who are willing to pay for it. A no-fee card, in contrast, typically offers more straightforward, lower-cost benefits.

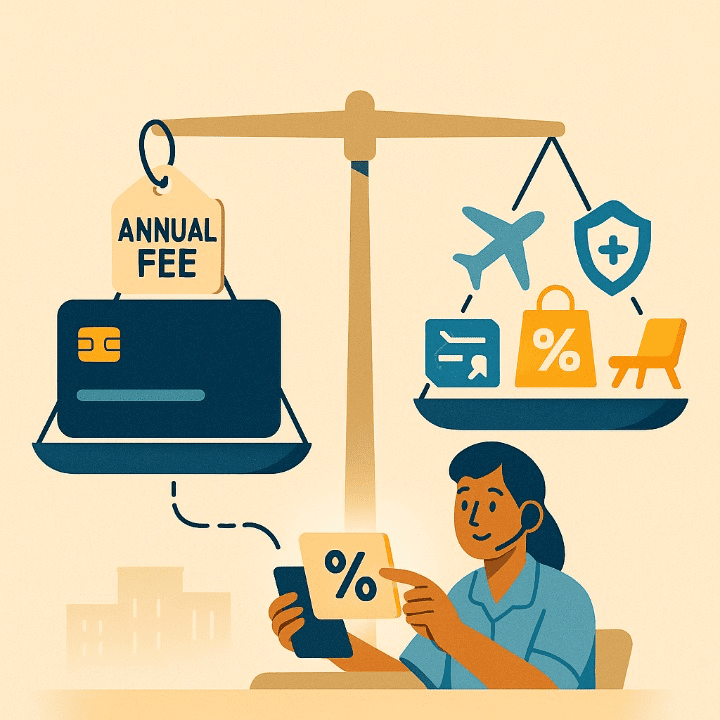

The Other Side of the Coin: Common Perks of Fee-Based Cards

To decide if a fee is worth it, you first need to understand what you’re potentially getting for your money. The benefits offered by premium cards are designed to appeal to specific lifestyles, particularly those of frequent travelers or high spenders.

Enhanced Rewards Structures

While many no-fee cards offer great rewards, fee-based cards often take it to the next level. This could mean a higher cash-back percentage in common spending categories, more valuable points or miles per dollar spent, or a large sign-up bonus that can be worth hundreds of dollars right from the start.

Valuable Travel Credits and Perks

This is a major selling point for premium travel cards. Common benefits include:

- An annual statement credit to cover airline fees or hotel charges.

- Access to a global network of airport lounges.

- A fee credit for programs like TSA PreCheck or Global Entry.

- Free checked bags on a specific airline.

Robust Insurance Protections

This is a crucial, yet often overlooked, benefit. Many premium cards offer a suite of insurance products that could cost a significant amount if purchased separately. This built-in insurance is a key part of their value proposition and can include:

- Trip Cancellation/Interruption Insurance: Reimburses you for prepaid, non-refundable expenses if your trip is cancelled or cut short for a covered reason.

- Primary Auto Rental Collision Damage Waiver: Allows you to decline the rental company’s expensive insurance policy.

- Lost Luggage Reimbursement: Covers the cost of your luggage and its contents if the airline loses it.

- Extended Warranty and Purchase Protection: Extends the manufacturer’s warranty on items you buy and protects new purchases against theft or accidental damage.

The “Is It Worth It?” Calculation: A Simple Framework

Deciding on a fee-based card requires more than just being impressed by the perks; it requires a simple cost-benefit analysis. Here’s how you can do the math for yourself.

- Step 1: Assign a Realistic Dollar Value to the Perks. Go through the list of benefits and assign a monetary value only to the ones you are certain you will use in a year. For example, a $100 airline credit is worth $100 if you’ll use it. However, airport lounge access is worth $0 if you never have time to visit the lounge. Be honest with yourself about your actual habits.

- Step 2: Calculate Your Estimated Rewards Value. Look at the card’s rewards structure and estimate your annual spending in its bonus categories. For example, if a card offers 3% back on dining and you spend $400 a month on restaurants, that’s $144 in rewards per year from that category alone.

- Step 3: Do the Final Math. Add the value of the perks you’ll use to the estimated value of the rewards you’ll earn. Then, subtract the card’s annual fee. (Value of Usable Perks + Value of Earned Rewards) – Annual Fee = Net Value

If the net value is significantly positive, the card is likely a good financial choice for you. If it’s negative or only slightly positive, a no-fee card is probably the better option.

A Practical Scenario: Comparing Two Cardholders

Let’s look at two friends, Mark and Jessica, who are both considering a travel credit card with a $250 annual fee.

- Mark travels for work twice a month. He knows he will use the card’s $150 annual hotel credit. The free checked bag perk will save him at least $240 a year. He also values the peace of mind from the card’s comprehensive travel insurance. For Mark, the tangible benefits ($150 + $240 = $390) already far exceed the $250 fee, even before calculating his rewards points. The card is an excellent deal for him.

- Jessica takes one big vacation a year. She typically packs light, so the free checked bag perk isn’t useful. She also prefers to book budget rentals where the hotel credit doesn’t apply. While the rewards are appealing, she calculates that a no-fee cash-back credit card would still earn her a decent amount without the upfront cost. For Jessica’s lifestyle, the annual fee is not worth it.

This shows that the value of a credit card is not universal; it is entirely personal.

Final Questions to Ask Yourself

Before you apply for a card with an annual fee, ask yourself these final questions:

- Does my regular spending align with the card’s high-reward categories?

- Will I realistically use the premium travel and insurance benefits?

- Can a no-fee card meet my needs sufficiently?

- Most importantly, am I disciplined enough to pay my balance in full every month? If you carry a balance, the interest charges will quickly erase the value of any rewards you earn.

Conclusion

There is no simple “yes” or “no” when it comes to paying a credit card annual fee. A no-fee card is often the smartest and safest choice for many people. However, for individuals whose spending habits and lifestyle align with the offerings of a premium card, paying a fee can be a strategic move that provides substantial value. From enhanced rewards to a safety net of insurance protections, the right fee-based card can be a powerful financial tool. The key is to look past the marketing, do an honest analysis of your own life, and choose the card that truly works for you.