The 50/15/5 Rule offers a clear, actionable framework for beginners aiming to secure their financial future. Consequently, this modern budgeting guideline simplifies the often-intimidating world of personal finance, especially when planning for retirement. Understanding this rule can significantly impact your long-term wealth accumulation. Indeed, it provides a practical path to balance current expenses with future goals. Therefore, adopting this strategy helps individuals build a robust financial foundation.

What is the 50/15/5 Rule?

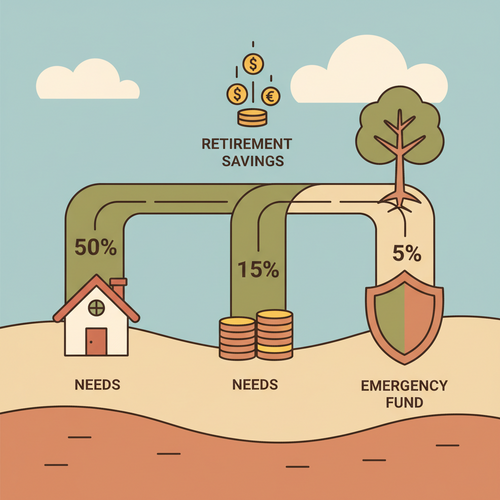

Specifically, the 50/15/5 Rule is a straightforward budgeting method. It dictates how you should allocate your after-tax income. This rule breaks down your monthly earnings into three distinct categories. Firstly, 50% of your income should cover your needs. Secondly, 15% is dedicated to retirement savings. Thirdly, 5% goes towards short-term savings or debt repayment. Consequently, the remaining 30% is for wants. This structure provides a clear blueprint for managing your money effectively. Furthermore, it helps ensure that critical financial goals, like retirement, are prioritized from the outset. Thus, this rule acts as a powerful guide for financial discipline.

50% for Needs: Covering Your Essentials

The largest portion of your income, 50%, is allocated to your needs. This category encompasses all essential expenses necessary for living. For instance, housing costs, including rent or mortgage payments, fall into this group. Utility bills, such as electricity, water, and internet, are also crucial needs. Groceries and essential transportation costs, like gas or public transit, are included. Furthermore, health insurance premiums and minimum loan payments are considered needs. Adhering to this 50% guideline prevents overspending on necessities. Moreover, it ensures you have enough income remaining for savings and discretionary spending. Therefore, careful tracking of these expenses is paramount for success.

Managing your needs effectively often requires careful budgeting. You might consider ways to reduce these core expenses. For example, looking for more affordable housing or reducing energy consumption can free up funds. Moreover, cooking at home more often saves money compared to dining out frequently. In addition, reviewing subscription services and cancelling unused ones helps optimize this category. Consequently, by keeping your needs in check, you create more flexibility in your budget. This disciplined approach directly supports your ability to save for the future. Fidelity provides excellent resources for budgeting advice.

15% for Retirement Savings: Building Your Future Wealth

The 15% allocation for retirement savings is arguably the most critical component of this rule. This percentage represents a dedicated effort to secure your financial independence in later life. Specifically, this money should be invested in retirement accounts. Options include a 401(k) through your employer or an Individual Retirement Account (IRA). Contributions to these accounts benefit from tax advantages. Furthermore, consistent contributions allow your money to grow significantly over time due to compounding interest. Indeed, starting early amplifies the power of compounding. Therefore, making regular deposits into your retirement fund is non-negotiable.

Many employers offer a matching contribution to 401(k) plans. Consequently, contributing enough to receive the full employer match is essentially free money. Never leave this benefit on the table. If a 401(k) is unavailable, an IRA remains an excellent alternative. Moreover, explore both Roth and traditional IRA options to determine which best suits your tax situation. Automating your retirement contributions simplifies the process significantly. Furthermore, setting up automatic transfers ensures you consistently hit your 15% target. Thus, your future self will undoubtedly thank you for this foresight. Charles Schwab offers valuable insights into retirement planning.

5% for Short-Term Savings & Debt: Immediate Financial Security

The final 5% component addresses immediate financial security and high-interest debt. This portion serves a dual purpose. Firstly, it builds an emergency fund. An emergency fund provides a crucial safety net for unexpected expenses. For instance, job loss, medical emergencies, or car repairs can be devastating without readily available cash. Aim for three to six months’ worth of living expenses in an easily accessible, high-yield savings account. Secondly, this 5% can be directed towards high-interest debt. Consequently, credit card debt or personal loans often carry substantial interest rates. Eliminating these debts quickly saves you money in the long run. Therefore, prioritizing this 5% helps reduce financial stress and builds resilience.

Addressing high-interest debt is similar to finding immediate returns on investment. For example, paying off a credit card with 20% interest is like earning a guaranteed 20% return. Moreover, once high-interest debt is eliminated, this 5% can be fully dedicated to bolstering your emergency fund. Subsequently, with a fully funded emergency cushion, you gain immense peace of mind. This financial stability allows you to focus more intently on long-term goals. Indeed, this systematic approach creates a strong buffer against unforeseen circumstances. Bank of America provides information on various savings options.

Why a “Modern Twist” on Retirement Saving?

The 50/15/5 Rule is often described as a “modern twist” because it acknowledges today’s economic realities. Older financial advice frequently suggested saving 20% or even 30% of your income. However, current challenges, such as rising housing costs, student loan debt, and inflation, make those percentages difficult for many. This rule provides a more realistic and attainable starting point. Consequently, it promotes financial progress without demanding immediate, drastic lifestyle changes. Furthermore, its flexibility allows individuals to adjust their strategy as their income and expenses evolve. Thus, it is a practical guide for contemporary financial landscapes.

Unlike rigid, one-size-fits-all approaches, the 50/15/5 Rule offers adaptability. It prioritizes essential needs while still emphasizing crucial retirement savings. For instance, someone burdened with student loan payments might find a 20% savings target overwhelming. This rule, however, breaks down savings into manageable chunks. In addition, it indirectly encourages a mindful approach to “wants” by capping them at 30%. Therefore, it encourages a balanced financial life. Ultimately, it’s about making smart choices that align with your current situation while steadily building for the future. Reuters offers up-to-date economic news impacting personal finance.

Implementing the 50/15/5 Rule: A Step-by-Step Guide

Implementing the 50/15/5 Rule begins with understanding your current financial picture. Firstly, calculate your after-tax income accurately. This figure is your starting point for all allocations. Secondly, meticulously track all your expenses for a month or two. This step helps categorize spending into needs, wants, and savings. Furthermore, identify where your money is actually going. This awareness is crucial for making informed adjustments. Consequently, you will gain a clear insight into your spending habits.

Once you have a clear picture, start adjusting your budget. Identify areas where you can reduce “wants” to free up funds. For instance, dining out less frequently or cutting back on expensive entertainment can help. Furthermore, automate your savings as much as possible. Set up automatic transfers to your retirement accounts and your emergency fund. This automation ensures consistency and removes the temptation to spend those funds. In addition, regularly review your budget. Life circumstances change, and your budget should adapt accordingly. Therefore, consistent review and adjustment are key to long-term success. Bloomberg provides global business and finance news relevant to financial planning.

Benefits of Adopting the 50/15/5 Rule

Adopting the 50/15/5 Rule offers numerous benefits, especially for beginner investors. Primarily, it provides clarity and simplicity. The straightforward percentages make it easy to understand and apply. Furthermore, it instills financial discipline without being overly restrictive. This balance helps avoid burnout often associated with aggressive budgeting. Consequently, you build healthy financial habits over time. Indeed, the rule promotes a balanced financial life, addressing both immediate needs and future aspirations. Thus, it fosters a sense of control over your money.

Moreover, the rule inherently prioritizes retirement saving. By dedicating a specific percentage to your future, you consistently work towards long-term security. In addition, the 5% for short-term savings and debt creates a strong financial buffer. This helps mitigate the impact of unexpected financial shocks. Therefore, you reduce stress and increase your overall financial resilience. Ultimately, this rule empowers you to make conscious financial choices. It moves you from merely reacting to expenses to proactively planning your financial journey. Consequently, it leads to greater peace of mind and financial freedom.

Common Pitfalls and How to Avoid Them

While the 50/15/5 Rule is simple, certain pitfalls can hinder its effectiveness. One common issue is miscategorizing “wants” as “needs.” For example, expensive cable packages or daily gourmet coffees are typically wants, not essential needs. Be brutally honest with yourself when defining these categories. Furthermore, neglecting your emergency fund is another trap. Without a robust emergency fund, any unexpected expense can derail your entire budget. Therefore, consistently prioritize that 5% for short-term savings until your fund is adequately built. Consequently, you will prevent financial crises from becoming disasters.

Another pitfall involves not starting early enough with retirement savings. The power of compounding works best over long periods. Delaying even a few years can significantly reduce your eventual nest egg. Therefore, begin saving that 15% as soon as possible. In addition, failing to review and adjust your budget periodically can lead to outdated allocations. Life changes, and your financial plan should evolve with it. Moreover, don’t get discouraged if you don’t hit the percentages perfectly every month. The goal is progress, not perfection. Indeed, small, consistent steps lead to significant long-term gains. Thus, stay persistent and adaptable in your financial journey.

Conclusion

In conclusion, the 50/15/5 Rule presents a practical and effective framework for modern retirement saving. It successfully balances immediate needs with future financial security. By allocating 50% to needs, 15% to retirement savings, and 5% to short-term savings or debt, you establish a clear path. Furthermore, this rule encourages financial discipline and mindfulness without being overly restrictive. Consequently, it empowers even beginner investors to take control of their financial destiny. Therefore, embrace this modern twist on budgeting to build a secure and prosperous future. Start implementing the 50/15/5 Rule today, and watch your financial confidence grow.