Navigating the complexities of life insurance can be challenging, but understanding the fundamental differences between Term vs. Whole Life Insurance is crucial for sound financial planning. This comprehensive guide aims to demystify these two primary types of life insurance, empowering you to make informed decisions for your future and your loved ones’ security. Consequently, we will explore their structures, benefits, and ideal scenarios, providing clarity in a often-confusing landscape.

Understanding Life Insurance: The Core Purpose

What is Life Insurance?

Life insurance serves as a contract between an individual and an insurance provider. In exchange for regular premium payments, the insurer pledges to pay a lump sum of money, known as a death benefit, to designated beneficiaries upon the insured’s passing. Essentially, it offers financial protection, ensuring that your family or dependents receive crucial financial support when they need it most. This support helps cover immediate expenses and long-term financial stability.

Why is Life Insurance Essential for Financial Planning?

Life insurance plays a pivotal role in a robust financial strategy. Primarily, it safeguards your family from financial hardship should you unexpectedly pass away. The death benefit can replace lost income, pay off debts such as mortgages and car loans, fund children’s education, or even cover daily living expenses. Furthermore, certain types of life insurance can accumulate cash value, which you can leverage during your lifetime. Therefore, it acts as a critical safety net, providing peace of mind and securing your legacy.

Term Life Insurance: Simplicity and Affordability

How Term Life Insurance Works

Term life insurance provides coverage for a specific period, or “term,” typically ranging from 10, 20, or 30 years. You pay a fixed premium throughout this term. If the insured individual passes away within the policy term, the beneficiaries receive the death benefit. However, if the term expires and the insured is still alive, the coverage ceases, and you receive no payout. Generally, you can renew term policies, often at a higher premium, or convert them into a permanent life insurance policy.

Key Features and Benefits of Term Life

- Affordability: Term life policies are significantly less expensive than whole life policies, especially for younger individuals. This makes them accessible to a broader range of budgets.

- Simplicity: Their straightforward nature makes term policies easy to understand. You know precisely what you are getting: pure death benefit protection for a set period.

- Flexibility: You can choose a term length that aligns with specific financial obligations, such as the duration of a mortgage or until your children become financially independent.

- No Cash Value: While this means no savings component, it also means lower premiums. Many people prefer to invest the difference in premiums themselves.

Consequently, term life insurance focuses solely on providing a death benefit without a savings component. This direct approach appeals to many seeking cost-effective protection.

Who Should Consider Term Life Insurance?

Term life insurance is often ideal for individuals with significant financial responsibilities for a defined period. Young families with dependent children, homeowners with outstanding mortgages, or anyone requiring substantial coverage on a limited budget find it particularly appealing. Furthermore, entrepreneurs or those in specific career stages can utilize term policies to cover business debts or secure partnerships for a set timeframe. For many, it represents the most practical and efficient way to protect their loved ones during critical years. Investopedia provides further insights into the pros and cons of term life insurance.

Whole Life Insurance: Lifelong Coverage and Cash Value

The Mechanics of Whole Life Insurance

In contrast to term life, whole life insurance offers coverage for your entire life, as long as premiums are paid. It is a form of permanent life insurance. A distinguishing feature is its cash value component, which grows on a tax-deferred basis over time. This cash value becomes an accessible resource that policyholders can borrow against or withdraw from later in life. Furthermore, whole life policies generally have level premiums, meaning the amount you pay remains constant throughout your life, regardless of age or health changes.

Key Features and Benefits of Whole Life (Cash Value, Dividends)

- Lifelong Coverage: Provides protection for your entire life, guaranteeing a death benefit no matter when you pass away.

- Cash Value Growth: The policy builds cash value over time, which can be accessed through loans or withdrawals. This creates a living benefit that can be used for emergencies, retirement income, or other financial needs.

- Level Premiums: Premiums remain constant, offering predictability in your long-term financial planning. This stability is a significant advantage for budgeting.

- Potential Dividends: Some whole life policies, particularly those from mutual companies, may pay annual dividends. You can use these dividends to reduce premiums, purchase additional coverage, or take them as cash.

- Tax Advantages: The cash value grows tax-deferred, and policy loans are typically tax-free. Moreover, the death benefit is generally income tax-free to beneficiaries. The IRS offers guidance on the taxation of life insurance proceeds.

Ultimately, whole life insurance provides both a death benefit and a savings component, making it a powerful tool for comprehensive financial security.

Who Should Consider Whole Life Insurance?

Whole life insurance suits individuals seeking permanent coverage and a savings component within their insurance policy. It is particularly beneficial for those looking for a guaranteed death benefit, a stable financial asset, and potential estate planning advantages. High-net-worth individuals, business owners planning for succession, or those seeking a conservative, long-term savings vehicle often find whole life appealing. Furthermore, it can be a valuable tool for philanthropic giving or ensuring funds for final expenses, regardless of when they occur.

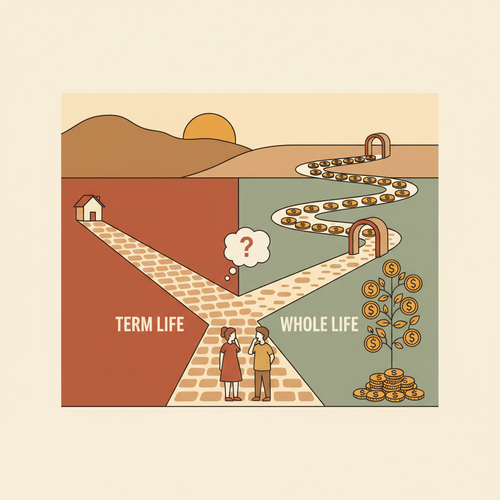

Term vs. Whole Life: A Direct Comparison

Understanding the fundamental differences between term and whole life insurance requires a detailed comparison across several key aspects. Each policy type caters to distinct needs and financial objectives. Therefore, weighing these factors carefully is essential for making an informed decision that aligns with your specific circumstances. We will now delve into the critical differences.

Cost and Premiums

A primary difference lies in the cost. Term life insurance is considerably more affordable than whole life insurance for the same amount of coverage. This is because term policies only provide protection for a limited period and do not build cash value. Consequently, a whole life policy’s premiums are significantly higher due to its lifelong coverage, guaranteed cash value growth, and embedded investment component. This higher premium reflects the added benefits and permanence of the policy. Therefore, budget considerations often drive the initial choice between the two.

Flexibility and Customization

Term life insurance offers flexibility in terms of duration. You can choose a term that precisely matches a specific need, such as a 20-year mortgage. At the end of the term, you have options to renew, convert, or let the policy expire. Whole life, by contrast, offers less flexibility in its core structure since it’s designed for permanence. However, the cash value component provides internal flexibility, allowing you to borrow against it. Policy riders can also customize both types, adding benefits like waiver of premium or accidental death coverage. Ultimately, term policies are simpler to adjust in terms of coverage duration, while whole life offers flexibility through its accumulating cash value.

Investment Component vs. Pure Protection

This represents one of the most significant distinctions. Term life insurance is often called “pure protection” because its sole purpose is to provide a death benefit. It has no savings or investment component. Many financial advisors suggest buying term and investing the difference in premiums into separate investment vehicles like IRAs or 401(k)s. Conversely, whole life insurance includes a savings component that accumulates cash value over time. This cash value grows at a guaranteed rate and acts as an internal investment. While this provides a conservative growth option, its returns are typically lower than those of market-based investments. Thus, your investment philosophy plays a crucial role in deciding which type suits you best. NerdWallet offers a detailed comparison on the investment aspects of these policies.

Tax Implications

Both term and whole life insurance offer significant tax advantages. In both cases, the death benefit paid to beneficiaries is generally income tax-free. However, whole life insurance has additional tax benefits related to its cash value. The cash value grows tax-deferred, meaning you do not pay taxes on the growth until you withdraw the money. Furthermore, loans taken against the cash value are typically tax-free, as they are not considered taxable income. Withdrawals up to the amount paid in premiums are also usually tax-free. These tax efficiencies make whole life an attractive option for certain long-term financial and estate planning strategies.

Making the Right Choice: Factors to Consider

Choosing between term and whole life insurance is a highly personal decision, contingent upon your unique financial situation and long-term objectives. Therefore, a careful evaluation of several key factors is essential before committing to a policy. This thoughtful consideration ensures your insurance aligns perfectly with your life stage and financial strategy. We will explore these critical considerations in detail.

Financial Goals and Budget

Your overall financial goals should guide your insurance choice. Are you primarily focused on providing temporary income replacement for your family? If so, the affordability of term life might be more suitable, allowing you to allocate funds to other investments. However, if your goal includes guaranteed lifelong coverage, a conservative savings vehicle, and estate planning, a whole life policy could be a better fit, assuming your budget can accommodate the higher premiums. Consequently, assess your current financial capacity and future aspirations thoroughly.

Dependency and Life Stages

The presence and age of your dependents heavily influence your insurance needs. Young parents with significant financial obligations, like raising children and paying a mortgage, often require substantial coverage for a defined period, making term life a practical choice. As children become independent and debts are paid off, the need for a large death benefit might diminish. Conversely, individuals who wish to leave a legacy, cover final expenses, or provide for a special needs dependent throughout their entire life might find whole life insurance more appropriate. Your life stage dictates the type and duration of coverage you need.

Risk Tolerance and Investment Philosophy

Consider your personal approach to investing. If you prefer to manage your investments separately and seek potentially higher returns in the market, then term life insurance, combined with an aggressive investment strategy for the premium difference, might align with your risk tolerance. However, if you prefer a guaranteed, conservative growth component within your insurance policy and appreciate the stability of level premiums, whole life insurance offers a lower-risk alternative. It provides a built-in savings mechanism without exposure to market volatility. Ultimately, your comfort with risk and your broader investment views are key determinants.

Conclusion

Both term and whole life insurance policies offer invaluable financial protection, yet they serve distinct purposes for different financial journeys. Term life provides affordable, straightforward coverage for a specific period, making it ideal for temporary, high-need situations. On the other hand, whole life offers lifelong protection, builds cash value, and presents a more permanent solution with potential estate planning benefits. The “best” option ultimately depends on your individual circumstances, including your budget, financial goals, dependents, and investment philosophy. Therefore, meticulously evaluating your personal needs and perhaps consulting with a qualified financial advisor will empower you to select the policy that best secures your financial future and the well-being of your loved ones.